Every piece in this shelf has counted a dollar: the fee on a placement, the proceeds of an offering, the revenue of a machine, the gain on a stake, each a real number, filed, cited by accession, checkable against the page it came from. Counting the dollar is the easy part. The dollars always net: every gain is a charge somewhere, every source a use, and across this table the money nets to zero. What changes is how it nets, and how it nets is what the quality of cash reads. The hard part, and the part the market prices last, is the difference between a dollar a company holds now and value that still has to become cash: the difference between present and future value, and what has to happen to close it.

That difference needs a reconciliation the moment has outgrown. The buildout is widely called the most expensive capital outlay in modern history, and it is financed on a circle: the same names invest in one another, buy from one another, and stand behind one another’s paper, through arrangements that run from ordinary terms to the most elaborate special-purpose vehicles. An income statement cannot see the circle; a cash flow statement sees one company’s half of it. This piece reads with a third reconciliation, CBITDA, which does to the cash flow statement what the cash flow statement does to the income statement: it looks past the page, into the footnotes and into other companies’ filings, where the circle nets to zero. It reads the ecosystem whole, and each player’s role inside it, credit and equity on one ledger.

A season of reading those filings has graded dollars end to end on that axis. Sorted by what must still happen, four kinds appear, from the dollar already done to the dollar that may never arrive. Each has a piece behind it.

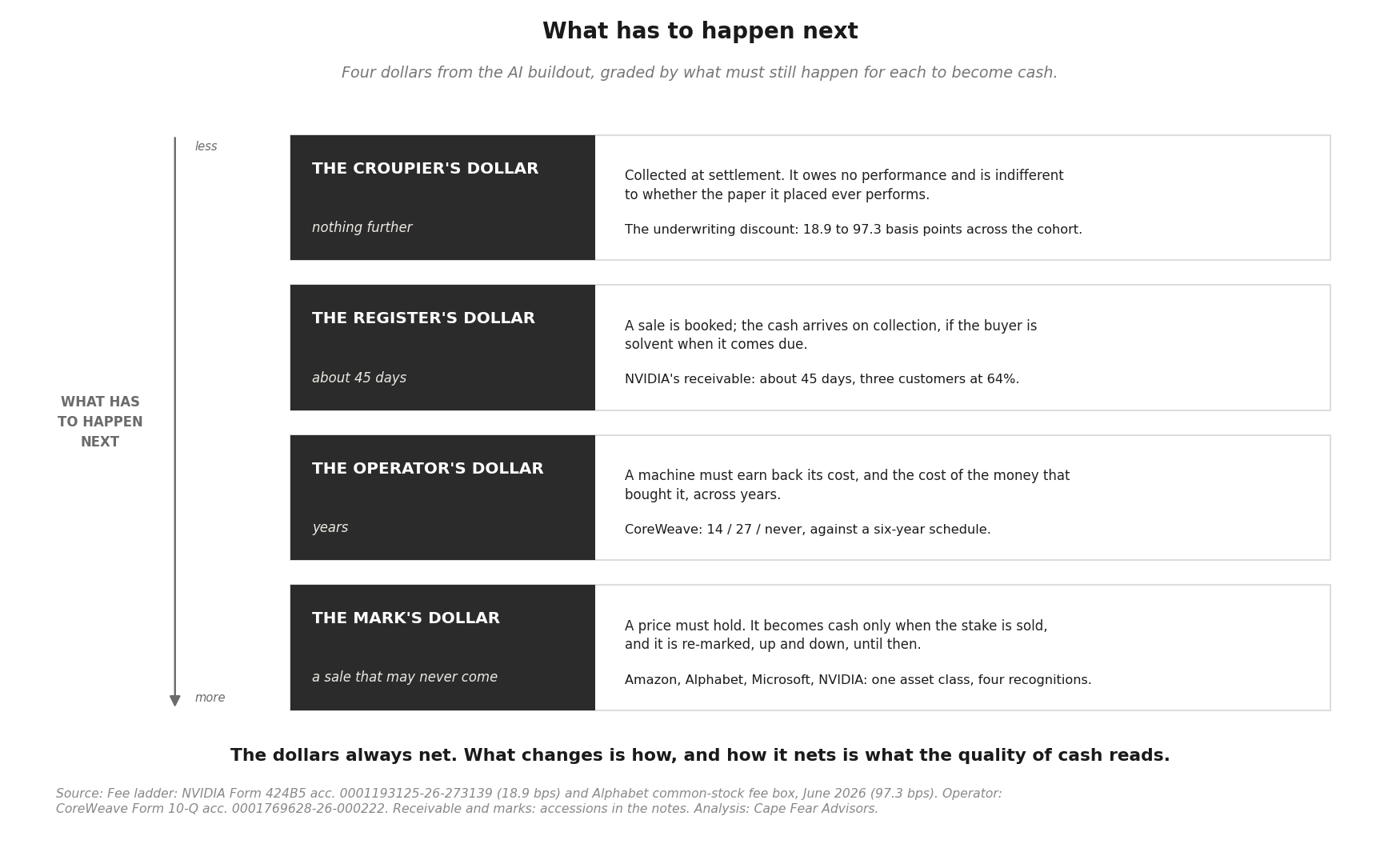

The croupier’s dollar

The house that places the paper is paid first, and paid in a dollar that needs nothing further. The underwriting discount is collected at settlement, not billed; it owes no future performance; and once settled it is indifferent to whether the paper it placed ever performs at all. By the shelf’s measure it is the highest-quality dollar the series has graded, and it always will be. It is why the house runs the casino, and it is earned: the diligence, the distribution, the brand put behind the paper, the balance-sheet risk carried while it is placed. The work is finished by the time the dollar settles, which is what makes it the best dollar at the table. The banks reported this quarter first, as they are paid first, and that harvest is already printed and read. (1)

The filings price it to the basis point wherever the deal is registered. Across one cohort, the same lead banks throughout, the placement cost ran from NVIDIA’s 18.9 basis points on investment-grade notes to Alphabet’s 97.3 on common stock, with the SpaceX IPO at 66.7 and a full tenor ladder in between, the far end of a curve costing as much as five times the near end. FINRA’s rule contemplates a ceiling of five percent; the SpaceX table printed two-thirds of one percent. The gap between what the rule permits and what the table prints is pricing power, and it runs toward the issuer. (1)

Two bounds sit on the grade. It renews only with the flow, falling back toward its own prior-year comparators when the issuance window narrows. And the same houses that step around the paper’s risk for a fee sit on the lender side of the same borrowers, where the exposure the fee avoids still lives; who holds that risk is referenced in the filed exhibits rather than reproduced in them. The fee dollar is pristine; the franchise around it is not unexposed.

The register’s dollar

The next dollar is booked at the counter and waits to be collected. A sale is recognized; the cash arrives later, on the order of forty-five days, if the buyer is solvent when it comes due. What has to happen next is small and ordinary, and it is not nothing: someone has to pay.

The filed instance is NVIDIA’s receivable, as the fourth house set out. Three unnamed customers held sixty-four percent of a $40.7 billion balance; the balance stood at about forty-five days of the quarter’s sales; the allowance against it priced the worry at roughly one basis point. The lines to watch are whether forty-five days lengthens, whether the concentration shifts, whether one basis point moves. The mirror is already filed on a buyer’s ledger, where vendor payables supplied $960 million of CoreWeave’s first-quarter cash: a receivable that lengthens at one register is the same days, booked as a source, at another. (2)

The operator’s dollar

The third dollar has to be earned by a machine, over years, and this is where the distances open. The operator buys equipment on borrowed money and must run it long enough to repay the borrowing and then some. Asked of CoreWeave as arithmetic, how many years of the machine earning at its filed rate would return the machine’s cost and the cost of the money, the answer ran to fourteen with an amortizing lender it never had, twenty-seven as the stack is filed, and never on the strategy the record shows, against equipment the company depreciates on a six-year schedule and a debt stack of $25.1 billion, fifty-nine percent of it at effective rates of ten percent or higher, none of it reaching past 2032. (3)

The croupier’s dollar was done at settlement; the operator’s dollar is a wager that a depreciating machine outearns its financing across a horizon longer than the machine’s own booked life. Everything downstream of it, the marks in the next rung included, rests on whether this dollar shows up.

The mark’s dollar

The fourth dollar was never collected and never billed. It is a mark: a change in the value of a stake that the rules compel the holder to recognize once the position is material. The number is not a choice. Mark to market does its work when the standard requires it, and the gain lands on the page. What each filer chooses is where on the page it lands and how much a reader is shown, and four of the largest holders chose differently this year.

Amazon named it. It recognized $12.3 billion of upward adjustment on private-company equity, “primarily from our nonvoting preferred stock in Anthropic,” stated the counterparty and the amount, carried the fair value from $14.8 billion to $32.0 billion across two dates, and put the figure on the front page. (4)

Alphabet reported the largest mark of all and named no one. Its gain on equity securities was $36.9 billion for the quarter, against $9.8 billion a year earlier, folded into a single line the filing attributes to “net unrealized gains on non-marketable equity securities.” No portfolio company is named anywhere in the document. (5)

Microsoft removed it. Its OpenAI interest is carried by the equity method, a different instrument, and its result runs through other income; the company then carries a non-GAAP line, “net (gains) losses from investments in OpenAI,” that strips the impact out, so a nine-month gain of $5.9 billion, most of it a one-time dilution gain from the October 2025 recapitalization, is subtracted back out of adjusted earnings. (6)

NVIDIA recognized $16 billion of it in income, $13.4 billion on publicly held stakes and $2.6 billion on private ones, in a quarter its operations produced $50 billion of cash. The operating income does not depend on the marks. Some of the revenue arrives from companies NVIDIA has itself put money into, and the marks are the upside on those same stakes, which either arrives or does not. On the far side of the same ledger, in the investing section, are two numbers: $17.9 billion of new money into private stakes in a single quarter, and $27 billion of investment commitments still open. Whether that number keeps climbing is a line the next prints draw. (7)

A mark becomes cash only when the stake is sold, or it is held until it is worth nothing, and in between it is re-marked up and down with no cash moving at all. A gain this quarter can be a loss next quarter and not one dollar has changed hands. That is why it belongs below the operating line, and why what a company does with it there is the whole of the judgment.

What is standing in for the cash

Behind that order runs a second one. The croupier’s dollar is cash. The register’s dollar is a sale that becomes cash on collection. The operator’s dollar is cash only if the machine earns it across the years. The mark’s dollar is not cash at all until a sale that may never come. Down the rungs, the reported result leans less on cash and more on something standing in for it.

Turned on a single company’s headline number, CBITDA sets its EBITDA against the cash behind it, in the footnotes and the counterparties’ filings, and the two come apart. EBITDA is read as a proxy for the cash an operation throws off; the distance between the proxy and the cash is the finding.

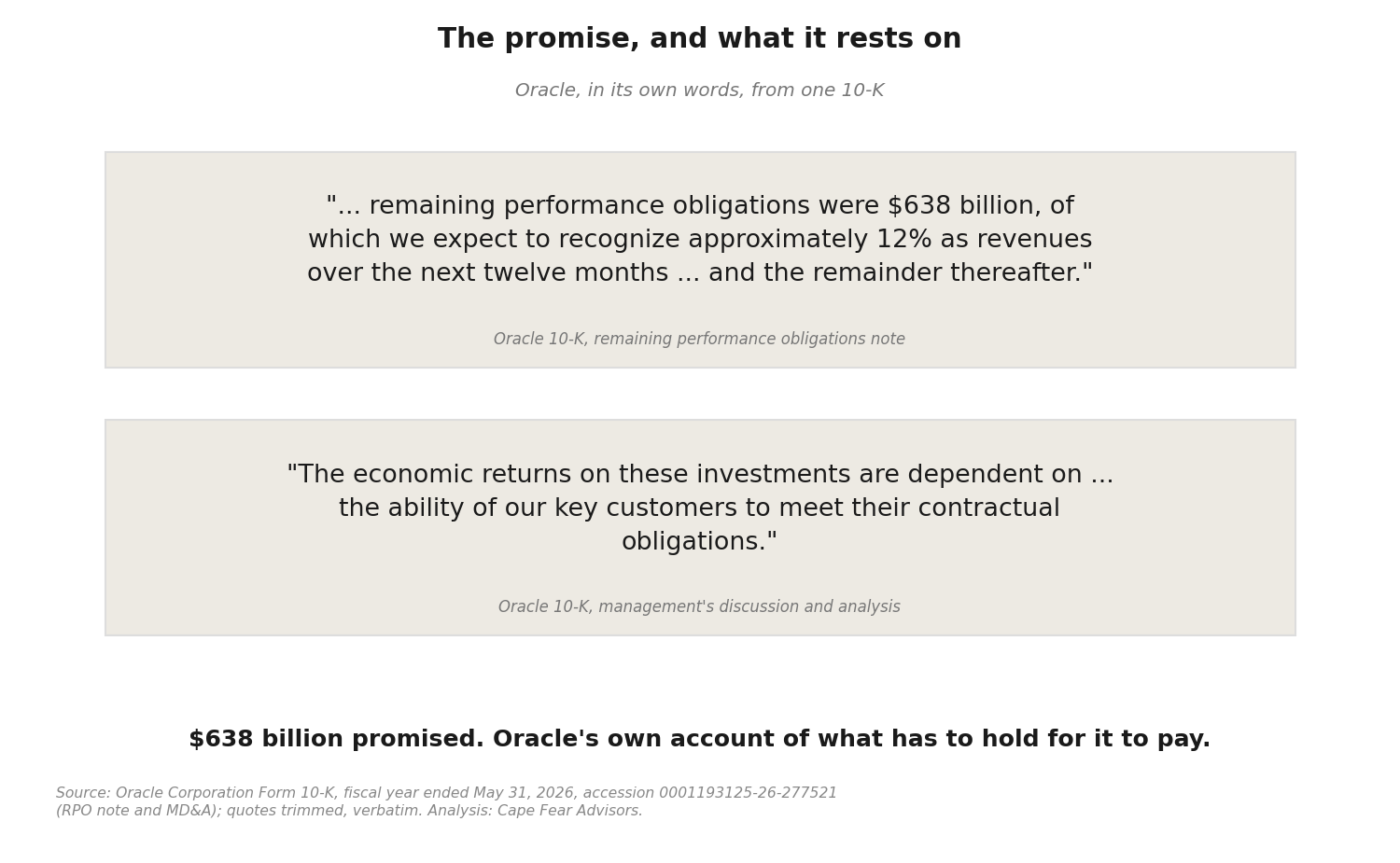

Oracle is the test, a business model in transition, and it prints its own answer. Its headline non-GAAP earnings per share for fiscal 2026 was $7.63; the company states that without the investment gains left inside it the figure is $6.83, so about a tenth of the number is gains rather than operations. Behind the earnings sits a backlog of $638 billion, of which the filing expects twelve percent to become revenue in the next twelve months, and a free cash flow of negative $23.7 billion for the year on $55.7 billion of capital spending. The headline is a promise, and an earnings number that includes the investment gains; the cash ran the other way. None of that reading is ours to prove. Oracle filed each number, the subtraction included; the lens only set them beside one another. (8)

This is not a verdict on Oracle. It is a company netting under extraordinary complexity, and it wrote the uncertainty into the same filing: the returns on its buildout, Oracle says, are “dependent on customer demand and the ability of our key customers to meet their contractual obligations,” and a change in either “may adversely affect operating margins, cash flows” and force a test of “the recoverability of related long-lived assets.” Most of the backlog lands beyond the first year, and the build is funded in the meantime by tens of billions of new debt and equity. The bull reads a contracted backlog no rival can match; the skeptic reads a promise financed ahead of the cash. Oracle wrote both into its 10-K; the next reports answer which governs, not this one. (8)

The reading assumes only what it must, that the filings are accurate and presented fairly in all material respects, and it carries its own inferences in the open, to be tested beside them. What it yields is less a single figure than a set of questions, some direct to the answer and some derivative of it, and much of the work of reading them is still ahead.

Most companies keep the mark out of the number they offer as cash, and the refusal is the tell in the other direction. Nebius kept a $780.6 million revaluation gain, the item that made its net income look remarkable, entirely out of its adjusted EBITDA. The four largest holders of these marks report no EBITDA at all; every mark sits below their operating line, and Microsoft subtracts its OpenAI gain out of adjusted earnings besides. CoreWeave’s gap comes from timing and set-aside interest rather than a mark, and the lens reads it the same way. (9)(10)

One definition leaves the mark inside, and no print has yet turned it into a gain. Two builders on the bitcoin side, TeraWulf and Core Scientific, define adjusted EBITDA to add back their warrant marks but not the remeasurement of the bitcoin they hold, so that line sits inside the metric. This quarter it was a small loss and lowered the figure. In a quarter the price rises, the same line becomes an unrealized gain that flows into the metric with nothing removed. The definition is filed; the quarter that turns it into a gain has not printed. (11)

The names here are the ones the market already talks about, and that is the only reason they are here; the examples could have been others. The reconciliation does not depend on the choice. Applied to any filer in the buildout, the reading holds, because it reconciles to the very numbers already being pointed at, and now and then points to one that no one is circling yet.

What the lens asks next

This is a skeptic’s lens, and it should say so: it asks future value to prove itself as cash, and it holds the dollar in hand above the dollar still promised. Turned the other way it is the bull’s lens too, because a bull’s case is won on the same page a skeptic’s doubt is, in whether a promise becomes cash, on time, from a payer still standing. The lens does not settle that argument. It points to where the argument settles, and names the filing that settles it.

The questions it leaves run past the one company shown here. SpaceX’s coming reports answer the distance between the cash a build of that scale requires and the output imputed to it in the valuation. CoreWeave’s next balance sheet answers which way the customer-liabilities caption resolves, toward revenue earned or toward something that services like debt. Microsoft’s disclosures answer how it carries its OpenAI obligations as the one-time gains roll off. OpenAI’s own numbers, if and when they are filed, answer the largest, how it meets the cash obligations it has taken on, and what they are. And Anthropic’s S-1 answers the last, the presentation and materiality judgments it makes on its first public page.

Some of these the market already circles, OpenAI’s obligations most of all. Others sit in a caption or a threshold few are reading yet. The lens does not answer them; it says which carry the weight.

The market quotes each of these companies on one figure and a multiple, and the figure does not carry its own grade. What has to happen next for it to become cash is printed in the filings, one rung and one reconciliation at a time. The grade is in the gap between the headline and the cash, and that gap is what CBITDA reads.

DISCLOSURE, standing: Anthropic is the developer of Claude, which is used in preparing this research. CoreWeave announced a multi-year agreement with Anthropic in April 2026; Amazon and Alphabet, named in this piece, hold large positions in Anthropic; and NVIDIA supplies the infrastructure providers that serve Anthropic. Figures are quoted from the filers without characterization, and the same standard of reading is applied to every filer named.

Figures are verified against the primary filings; documents are cited by accession number. Analysis: Cape Fear Advisors.

Cape Fear Advisors holds no position in any security named in this analysis and has received no compensation from any company discussed.

This analysis also appears on Substack.

Notes

(1) The fee ladder and the FINRA comparison are set out in this series’ croupier work: SpaceX Form 424B4, accession 0001628280-26-042639; NVIDIA Form 424B5, accession 0001193125-26-273139; Alphabet common-stock and note fee boxes as filed (June 2026). Cross-references: “The Price of the Seat” and “The Croupier Counts First”.

(2) NVIDIA receivable and concentration as set out in “NVIDIA, The Fourth House”; the balance is the quarter reported there and is refreshed at the next NVIDIA print. CoreWeave vendor-payables figure: 10-Q, accession 0001769628-26-000222.

(3) CoreWeave, Inc. Form 10-Q for the quarter ended March 31, 2026, accession 0001769628-26-000222, and “CoreWeave, Twenty-Seven Years” for the convergence arithmetic in full.

(4) Amazon.com, Inc. Form 10-Q, accession 0001018724-26-000014 (quarter ended March 31, 2026): upward adjustment on private-company equity $12,328 million, “primarily from our nonvoting preferred stock in Anthropic”; fair value of the nonvoting preferred approximately $14.8 billion at December 31, 2025 and $32.0 billion at March 31, 2026. A further $4.5 billion reclassification on converted convertible notes brings the two Anthropic lines to about $16.8 billion; total other income, net was $15.6 billion.

(5) Alphabet Inc. Form 10-Q, accession 0001652044-26-000048 (quarter ended March 31, 2026): gain on equity securities, net $36,915 million, against $9,758 million a year earlier; no portfolio company named.

(6) Microsoft Corporation Form 10-Q, accession 0001193125-26-191507 (quarter ended March 31, 2026): OpenAI carried under the equity method; other income (expense), net included a $5.9 billion net gain from OpenAI for the nine months then ended, primarily the dilution gain from the October 2025 recapitalization; non-GAAP measures exclude the OpenAI impact via the line “net (gains) losses from investments in OpenAI.”

(7) NVIDIA Corporation Form 10-Q, accession 0001045810-26-000052 (quarter ended April 26, 2026): net unrealized gains on publicly held equity securities $13.4 billion and on non-marketable equity $2.6 billion, recognized in other income (expense), net; net income $58.3 billion; net cash from operations $50.3 billion; net additions to non-marketable equity $17.9 billion in the quarter; $27 billion of investment commitments outstanding.

(8) Oracle Corporation Form 10-K, accession 0001193125-26-277521 (fiscal year ended May 31, 2026), and Q4 earnings release, Exhibit 99.1 to Form 8-K, accession 0001193125-26-265848: non-GAAP diluted EPS $7.63, which the company states would be $6.83 excluding investment gains; remaining performance obligations $638 billion, of which approximately twelve percent is expected to be recognized as revenue over the next twelve months; net cash from operations $32.0 billion; capital expenditures $55.7 billion; free cash flow negative $23.7 billion. The quoted risk language (“the economic returns on these investments are dependent on customer demand and the ability of our key customers to meet their contractual obligations ...”) is from the management’s discussion and analysis in the same 10-K. Forward funding, from the financing section of the same 10-K: $46,093 million of proceeds from issuances of senior notes, term loans and other borrowings, and $4,954 million of 6.50% Series D Mandatory Convertible Preferred Stock issued in fiscal 2026 (none a year earlier).

(9) CoreWeave Form 10-Q, accession 0001769628-26-000222, and the adjusted-EBITDA reconciliation in the Q1 2026 earnings release, Exhibit 99.1 to Form 8-K, accession 0001769628-26-000220: adjusted EBITDA $1,157 million, which sets aside $536 million of interest expense; net cash from operations $2,984 million, of which $2,016 million is working-capital movement; cash from operations before working capital $968 million; purchases of property and equipment $7,695 million; the $1.3 billion reclassification from deferred revenue to customer liabilities.

(10) Nebius Group Form 6-K, accession 0001104659-26-064092: a $780.6 million revaluation gain excluded from adjusted EBITDA of $129.5 million. Hyperscaler placement of marks below operating income and the absence of any EBITDA metric: Amazon accession 0001018724-26-000014; Alphabet 0001652044-26-000048; Microsoft 0001193125-26-191507; NVIDIA 0001045810-26-000052.

(11) TeraWulf Inc. Form 10-Q, accession 0001083301-26-000092, and Core Scientific, Inc. Form 10-Q, accession 0001628280-26-031396: each adds back warrant or contingent-value-rights marks in its adjusted-EBITDA definition and does not add back the fair-value remeasurement of digital assets, which therefore remains inside the metric; the remeasurement was a small loss in the quarter reported.