In the first quarter of 2026, CoreWeave’s operations produced $968 million in cash before working capital, and the company spent $7,695 million on equipment. New money covered most of the gap, debt at an average cost of 9.1 percent and an equity placement beside it; the rest came from collections of the year-end billings, customers’ cash in advance, vendor payables, and $810 million off the company’s own cash balance. The arithmetic here charges every machine dollar at the debt rate alone. On the company’s own filed numbers the answer is a range. An amortizing lender, which this stack has never contained, would be repaid in about fourteen years, nine at the strongest corner in the notes. The stack as filed needs about twenty-seven. And the strategy the record shows, surplus reinvested in new machines at these yields, clears in no year at all. The company’s depreciation schedule says the machines last six. Across the constructions, a dollar of machines returns at most 99 cents over its scheduled life, before the cost of any money; it never returns the dollar, and at year six, 44 to 78 cents of it is still owed, while the books carry the machines at zero. Every dollar of debt matures by October 2032, so the money must be raised roughly four and a half times over before even the shortest road is walked, each time at a price the market sets fresh; the June notes, priced at par on June 11, traded at 96.5 within a month. The inputs are CoreWeave’s, from its own filings; where another filer supplies a number, the piece names it. The arithmetic on top of them is ours, shown in full. Two questions survive it, and the company has already answered each of them once: how long the machines last, and how much cash, for how long. The piece ends where the answers point: what are these machines worth in 2032, and what will the money cost until then?

The quarter, in one currency

In the quarter ended March 31, 2026, CoreWeave reported revenue of $2,078 million, up 112 percent from a year earlier, and an operating loss of $144 million. With $1,147 million of depreciation and amortization added back, the quarter produced $1,003 million of EBITDA, a 48 percent margin. Reported operating cash flow was $2,984 million, but $2,016 million of that was working capital: receivables, payables, and deferred revenue moving through the quarter. Cash from operations before working capital was $968 million. Purchases of property and equipment were $7,695 million. Free cash flow was negative $4,711 million. Capital expenditure ran 7.7 times EBITDA. (1)

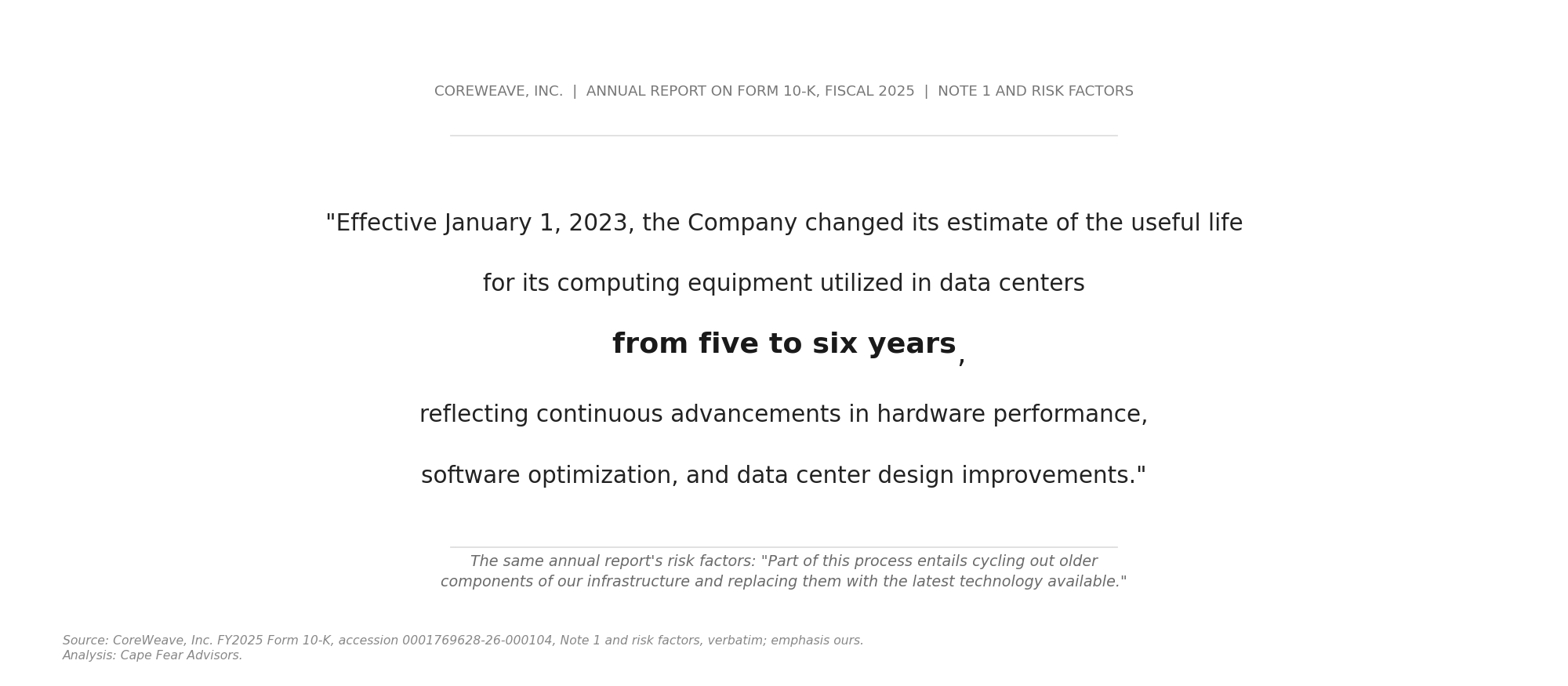

Depreciation is the accounting shadow of cash that already left. Lengthen the schedule and the shadow thins; the cash is unchanged. CoreWeave has pulled that lever once already: effective January 1, 2023, it extended the estimated life of its computing equipment from five years to six, and every quarter since has carried a thinner shadow per dollar of fleet than the old schedule would have cast. (6) The machines did not change when the estimate did, and neither did the cash. $7,695 million left this company in one quarter to buy equipment. The test that matters is whether the asset can return the cash and pay for the money, inside the time the asset exists.

The convergence test

What the money costs: CoreWeave’s interest expense was $427 million in the quarter, plus $97 million of interest capitalized into the asset base rather than expensed. Annualized against average debt of $23,116 million, the cost of the borrowed money is 9.1 percent. That figure is consistent with the stack’s own terms at quarter end: $25,149 million of principal across a dozen instruments, 59 percent of it at effective rates of 10 percent or higher, the highest at 15 percent, and the debt “bears interest at variable rates, the majority of which is unhedged.” On its unsecured name, in June, CoreWeave paid 9.625 percent in dollars and 8.500 percent in euros. (3)

What the assets produce: gross property and equipment stood at $40,933 million at quarter end, of which $9,581 million was construction in progress, not yet in service, earning nothing. The arithmetic excludes it. Annualized EBITDA of $4,012 million against $31,352 million of in-service gross equipment is a cash yield of 12.8 percent. The base is mostly the machines themselves: $26,627 million of it is technology equipment on the six-year schedule, and the rest, data center equipment, leasehold improvements, and software, carries filed lives from three to twelve years; note 5 prices the blend. (4)

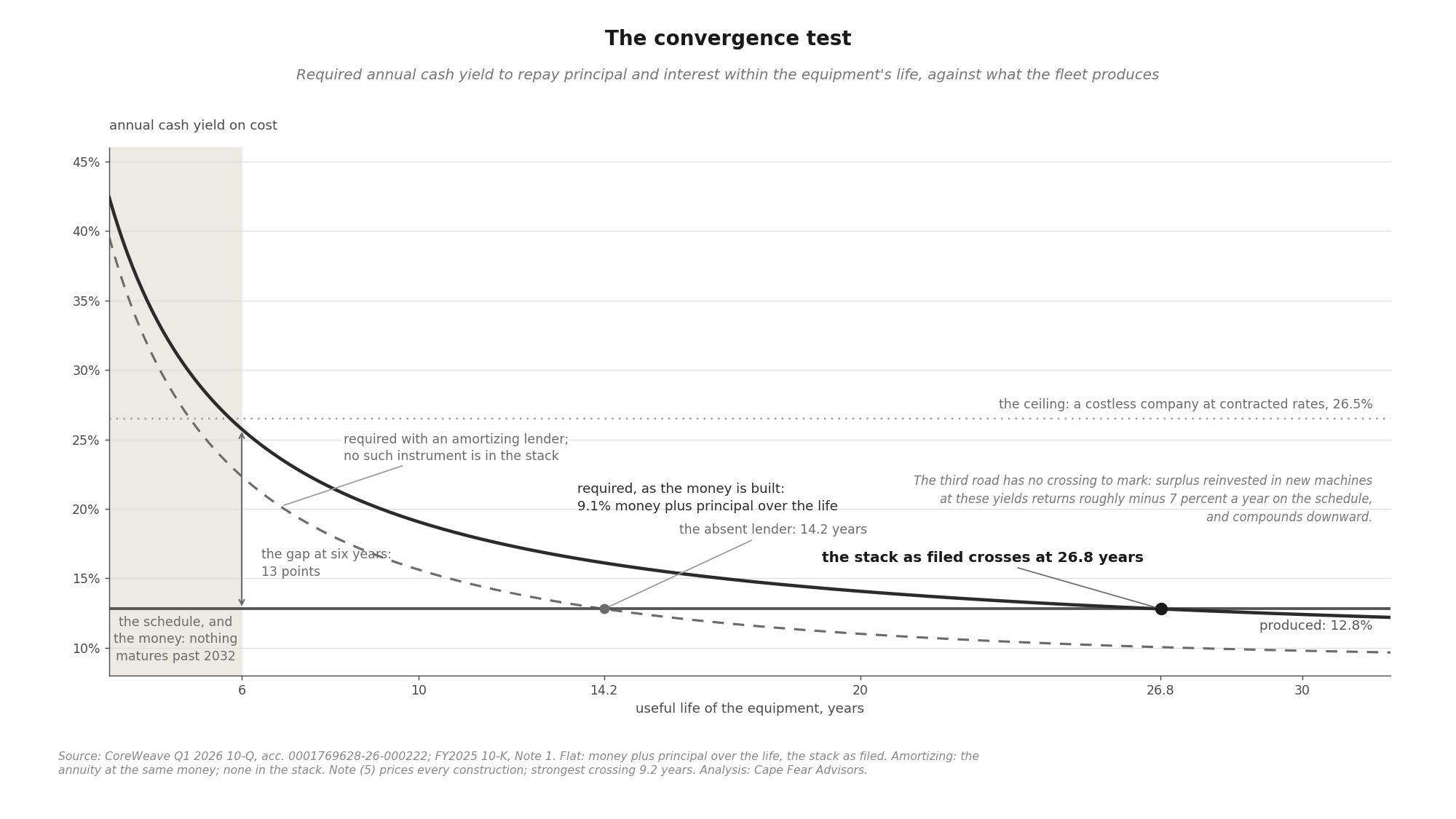

For a depreciating asset to pay its own interest and return its principal within its life, the required annual cash yield is the cost of money plus the principal spread across the years. At 9.1 percent money:

A five-year life requires a 29.1 percent yield. A six-year life, the company’s own schedule, requires 25.7. A ten-year life, 19.1; twenty years, 14.1. The equipment produces 12.8, and the lines cross at roughly twenty-seven years. Twenty-six point eight, on the unrounded figures. (5)

The rate is not the cause. Over its scheduled life, at its current yield, a dollar of machines returns about seventy-seven cents, before the cost of any money. The shortfall is native to the machine; the cost of money only sizes it. The twenty-seven years, and the residual below, are that multiplication plus a rate.

Twenty-seven is the flat arithmetic: interest on the full dollar for the full life, and no credit for the surplus in the meantime. Shorter constructions exist, and the piece prices each of them. An amortizing lender, retiring principal dollar by dollar at the money’s own 9.1 percent, moves the crossing to about fourteen years. With the quarter’s $153 million of stock compensation added back, shares not being cash, it is eleven. On the fleet’s average size across the quarter, every assumption taken at once, the shortest crossing these filings permit is about nine years. (5) Every one of them ends past the six-year schedule, and every one leaves the machine still owing at year six: between 44 and 78 cents of the original dollar, depending on the construction. But the constructions are not equally on file. No amortizing lender appears in this stack. The instruments are bullets, 80 percent of principal due within five years, nothing reaching past 2032, so fourteen is the number for a loan structure CoreWeave has never filed. Under a bullet, the surplus must wait somewhere until the principal falls due, and the filings show where it waits: it was spent, $7,695 million of new machines in the quarter against $968 million of operating cash, every surplus dollar and roughly seven raised beside it. That deployment is itself a rate. At the company’s own schedule, a new machine returns roughly minus 7 percent a year before any financing, minus 3.4 with the stock compensation added back, so the surplus, reinvested the way the record shows, compounds downward, and no year on the calendar clears the fleet. The range is fourteen, twenty-seven, never: the lender the company never had, the stack it has, and the strategy it is executing at these yields. Twenty-seven is the moderate reading. And the flat method’s zero, the assumption that the surplus earns nothing while it waits, is the strongest corner’s own measured rate: there, a reinvested dollar returns 99 cents over its scheduled life, about minus 0.2 percent a year. The bull case’s best arithmetic prices the waiting at zero. One guard travels with all of this. The minus 7 holds at the company’s stated life; if the machines outlive the schedule, the reinvestment rescues itself, and that is the residual question arriving through another door. Every road out runs through year six.

“The range is fourteen, twenty-seven, never: the lender the company never had, the stack it has, and the strategy it is executing at these yields. Twenty-seven is the moderate reading.”

The company’s schedule for the same machines is six years, and six is itself the product of the extension. The company’s words for the change: “reflecting continuous advancements in hardware performance, software optimization, and data center design improvements.” The same annual report’s risk factors describe the fleet’s future differently: “Part of this process entails cycling out older components of our infrastructure and replacing them with the latest technology available.” The pace of advancement lengthens the life of the asset in one note and requires the asset’s replacement in another. Both statements are filed. Neither is incorrect. They are the same fact, entered in two boxes. (6)

The residual, or who has said what the machines are worth

The same arithmetic runs backward. Held to the company’s own six-year schedule, over six years at a 12.8 percent yield, the equipment generates about 77 cents per dollar of cost in cash; the interest on the money consumes about 54 of those cents. For the lender to be made whole at year six, the machines must then be sold, or refinanced against, at roughly seventy-eight cents on the original dollar.

The company’s own depreciation schedule carries them at zero.

The question “what is a six-year-old GPU worth” is, in this record, a filed requirement. The capital structure needs the answer to be seventy-eight cents on the dollar. The books carry zero. The gap between those answers is the value of the fleet, and the tenors on file sit beside one of them. (7)

“The capital structure needs the answer to be seventy-eight cents on the dollar. The books carry zero.”

CoreWeave raised money six times in the first half of 2026: a non-recourse GPU facility in March, convertible notes and senior notes in April, a syndicated facility in May, dollar and euro senior notes in June. Every instrument matures by October 2032. The average tenor is about 5.9 years, against a stated equipment life of 6. Nothing in the debt stack reaches past 2032. Six-year money, against a six-year schedule and a twenty-seven-year requirement. (8)

Alphabet borrowed to 2126 this year, Amazon and Oracle to 2066, SpaceX to 2056. CoreWeave, whose machines must run twenty-seven years, has issued nothing that reaches past 2032, at any price the record shows. The refinancing arithmetic follows mechanically. A twenty-seven-year breakeven against a 5.9-year average tenor means the money must be raised roughly four and a half times over before the equipment has paid for itself. Each refinancing is a fresh underwriting at whatever rate the market offers that year, and the June paper, the cleanest read on the unsecured rate, came at 9.625 percent. By the second week of July the same notes, priced at par on June 11, were quoted at 96.50, a 10.42 percent yield. (9)

The price of the promise

The objection is that the customer contracts carry the value, not the machines. CoreWeave’s revenue is contracted years forward, $98.8 billion of remaining performance obligations, with investment-grade counterparties reported behind the largest commitments. On that reading, the equipment is a delivery mechanism, and the promise that matters belongs to the customer.

The income statement answers it, and the income statement is CoreWeave’s. The $98.8 billion lives in a footnote, and a remaining performance obligation is not a receivable. At this company the cash can arrive before the compute does, and some already has, in deposits and in invoicing ahead of performance. Money that arrives early sits as an obligation and discharges only as the machines deliver, and the income statement measures the discharge every ninety days. The most recent measurement is the quarter this piece opened with: revenue at the contracted rates, and 12.8 cents of annual EBITDA per dollar of in-service equipment. The contracts are not a second credit standing beside the machines. They are the machines’ output, sold forward, sometimes paid for early, and earned at the fleet’s pace and the fleet’s margins. The conversion rate is the number the twenty-seven years is built on. The objection holds on the balance sheet and in the footnotes. The income statement runs the contracts through the machines each quarter and prints what they earned.

The market priced the objection twice. Both prints are filed.

In March, CoreWeave closed an $8.5 billion facility through a ring-fenced subsidiary, non-recourse to the parent, secured by GPUs and one customer’s contract. Moody’s rated it A3. Investment grade, higher than SpaceX, higher than Oracle. In May, CoreWeave closed a $3.1 billion facility that carries everything the March facility lacked: the parent’s unconditional guarantee, subsidiary guarantees, a pledge of 100 percent of the borrower’s equity, security over substantially all assets. Its proceeds fund infrastructure dedicated to “two large, non-investment grade customers.” Moody’s rated it Ba2. Speculative grade. Same borrower family, same asset class, same banks, seven weeks apart, five notches. None of the mechanics is unusual; ring-fenced paper rating above its sponsor is what ring-fencing is for, and the two facilities differ in their customers as well as their structures. The direction is the measurement. The May facility carries strictly more of CoreWeave’s own credit support, the parent’s unconditional guarantee, the subsidiary guarantees, the full equity pledge, and it rated five notches lower. Everything the parent added did not close the gap the customers opened. The only thing that lifted the March facility to investment grade was the customer’s contract. And if the customer contract is the credit, then everything that is not the customer contract, CoreWeave’s own promise and CoreWeave’s own machines, is being priced separately, and the price is Ba2 and 2032. (10)

Both facilities were arranged by the same two banks, Morgan Stanley and MUFG, structuring on the investment-grade side in March and leading the speculative-grade syndication in May, paid on each. Five notches apart, one dealer. The role has a name at the table, the croupier, and it keeps its own ledger; this piece only notes who dealt both hands. (11)

Then, at the end of March, a counterparty acted on the inversion, and filed it. Applied Digital, CoreWeave’s landlord at Ellendale, amended its leases so that two data halls moved from CoreWeave the parent to the same ring-fenced subsidiary that borrowed at A3, with the parent demoted to a springing guaranty behind the subsidiary, plus a $50 million letter of credit. The landlord’s own 8-K explains why, in one sentence: the refinanced debt “received an investment grade credit rating of A3. These ratings compare favorably to CoreWeave Parent’s credit rating of BB.” And it draws its own conclusion: the swap is “favorable to the holders of its 9.250% notes due 2030.” The landlord told its own bondholders that replacing CoreWeave’s direct promise with a ring-fenced entity’s promise, keeping CoreWeave only as backup, improved their position. It is how one counterparty now structures around CoreWeave’s name. (12)

The same principle printed in the other direction on July 9, when S&P cut Oracle to BBB minus, the last notch of investment grade. The update’s rationale carries a section headed “OpenAI remains a key credit risk”: S&P estimates OpenAI at “roughly half of the $638 billion in RPO,” and writes that if OpenAI could not pay, Oracle “could be left with massive data center leases that it might be unable to exit or have to re-lease to new tenants under less-favorable terms.” At CoreWeave, a customer’s promise lifted ring-fenced paper five notches above the parent. At Oracle, a customer’s promise dragged an investment-grade parent to the edge of speculative grade, and Oracle’s shares rose 2.7 percent on the day of the cut. The counterparty is the credit, in both directions, priced by the agencies inside four months. And the same update, on the industry rather than the name: “the unit economics of the AI infrastructure business remain opaque.” (16)

The bull case, stated at full strength

The bull case is filed in the same 10-Q. It is three propositions, the same claim made at three dates.

First, that the machines are worth more today than the paper says. The revenue side of the argument runs through rent: the fleet earns at contracted rates set when compute was scarce, above what the spot market would pay, and will keep earning them. $9,581 million of construction in progress earns nothing yet and converts into that rent as it enters service. Revenue grew 112 percent year over year; remaining performance obligations are $98.8 billion. On this proposition the six-year schedule is not aggressive but conservative, and the books understate the fleet.

Second, that they will be worth roughly seventy-eight cents on the original dollar at year six. Not more than the schedule’s zero, which is a low bar; seventy-eight cents, which is the bar the arithmetic sets. The first proposition does not imply the second. A machine can out-earn its book today and still be worth little when its successor ships in volume; the same annual report that lengthened the life warns of exactly that cycling.

Third, that the company can keep engaging the capital markets, because the first two propositions mature more slowly than the debt does. A twenty-seven-year breakeven financed on 5.9-year money must be refinanced roughly four and a half times, and each turn reprices at whatever the market then believes about propositions one and two. The current mark is 9.625 percent, unsecured.

Two of the arithmetic’s inputs could improve, the price of money and the operating margin, and the filed numbers price both doors. Cheaper money: the risk-free rate falls to zero from 2032 onward, and CoreWeave rolls everything that matures at the best secured spread it has ever printed, the 2.25 points over the floating benchmark on the March facility. The machines still need roughly thirteen years to return their principal, against a six-year schedule, because the first six years of interest have already been paid at nine. And the spread carries a premise worth noticing: 2.25 points exists, in this record, only on paper secured by an investment-grade customer’s contract. The cheap-money door funds the third proposition with the customer’s credit, the same credit the ratings have already priced.

The margin door has a filed ceiling. Revenue per dollar of in-service equipment, at contracted rates, runs 26.5 cents a year. That is the yield of a costless company, and it clears the six-year requirement by about three months on the flat arithmetic, by about a year with the surplus credited. With selling and administration at zero, the yield is 15.8 percent, crossing at about fifteen years flat, ten credited. What the six-year schedule asks of the margin lever is nearly all of it either way: a margin over cash operating costs between 84 and 97 percent, leaving between 2.9 and 15.7 cents of each revenue dollar for power, rent, and people, against the 40.5 cents those costs take today. (2) The door exists, and it is between 0.8 and 4.2 points wide. All of these are conditional milestones, not forecasts. Each holds the fleet’s current pricing and productivity for the duration, and each is exactly as good as the quarter it is computed from.

Each proposition has a filed gauge. The third grades itself: every raise files its own rate and tenor. The second is graded by the lenders’ tenors already, and by any residual assumption that ever surfaces in a filed structure. And the first has a tell already sitting on the books.

The tell on the first is the fork this publication read in July. In the first quarter, $1.3 billion moved out of deferred revenue, the caption that resolves into revenue, and into a caption called customer liabilities that neither the quarterly nor the annual filing defines. A year earlier, a $230 million customer deposit was recharacterized as debt when the contract acquired a termination right, with a named standard and a stated cause. In that precedent, customer money changed category at the moment the contract’s terms changed. The quality of cash entered this series as a question about money still to come; here it attaches to money already received, the same dollars, revenue-shaped or debt-shaped, with the shape decided after they arrive. If the second quarter’s report shows the $1.3 billion flowing toward revenue as performance occurs, the first proposition is holding. If it hardens further toward something that services like debt, the terms are moving, in the one place the books would show it first. The fork is filed. The next filing picks a tine. (14)

One ratio grades the whole: does EBITDA per dollar of in-service gross equipment rise, quarter over quarter, faster than the useful life of the equipment falls? Both numbers are filed every ninety days. The trend so far runs the wrong way on the broader measure: 12.5 percent to 11.7 to 8.6 to 9.8 on total gross equipment across the four quarters the filings cover, with the fourth quarter derived from the annual report less its nine months. The single upturn arrives in the strongest reported quarter, and the August print says whether it was a turn or a quarter. The in-service measure is the better gauge, and the construction-in-progress conversion is the bull case’s whole first leg. That single line is the hyperscaler argument, reduced to something checkable. (13)

Two questions, answered once

CoreWeave has two questions it must keep answering, and it has answered each once. The first is accounting: matching the stated life of the machines to their actual life. It is a judgment call, and the company has made it once. Effective January 2023, five years became six. Asked once more, and solved for rather than chosen: what would the estimate have to be for the machines to pay for themselves and for the money that bought them? On the current quarter, twenty-seven years. The company’s answer is six. The arithmetic’s is twenty-seven, and never fewer than nine on any construction in the notes. Both are now on the table, and only one of them was ours.

The second is cash: how much, and for how long. That answer is on file: six raises in the first half of 2026 averaging 5.9 years at issue, a debt stack in which nothing reaches past 2032, and 59 percent of quarter-end principal priced at 10 percent or higher. Everything in this piece resolves if that financing carries the company to actual cash profitability, to quarters where operations fund the machines and the machines earn the contracts. Then the maturities are met from operations, the refinancings shrink instead of repeating, and the residual question never needs a sale to answer it. The quarter’s $7,695 million of equipment purchases sets the scale of the meantime: at that filed pace, a year of building adds roughly $30 billion of machines on the same terms, at 9 percent money against a six-year clock.

What are these machines worth in 2032? The schedule has answered. The tenors have answered. The agencies have answered twice, five notches apart, depending on whose promise stood behind the same silicon. A counterparty has begun structuring around the answer. The only answer not yet on file belongs to the equipment itself, and it reports every ninety days, in one ratio, starting with the print expected in August. (15)

Cape Fear Advisors holds no position in any company named above and has no commercial relationship with any filer cited. This is structural observation, not investment advice.

DISCLOSURE, standing: Anthropic is the developer of Claude, which is used in preparing this research. CoreWeave announced a multi-year agreement with Anthropic in April 2026, and Amazon and Alphabet, named in prior pieces in this series, hold large positions in Anthropic. Figures above are quoted from the filers without characterization, and the same standard of reading is applied to every filer named.

Figures are verified against the primary filings; documents are cited by accession number. Analysis: Cape Fear Advisors.

This piece was originally published on Substack on July 12, 2026.

Notes

(1) CoreWeave, Inc. Form 10-Q for the quarter ended March 31, 2026, accession 0001769628-26-000222 (CIK 1769628): income statement; cash flow statement (operating cash flow $2,984M, of which the working-capital swing is $2,016M: receivables +$1,042M, payables +$960M, deferred revenue +$575M, other -$561M); purchases of property and equipment including software, $7,695M. EBITDA computed as operating loss $(144)M plus depreciation and amortization $1,147M. The receivables line reverses a year-end balance: accounts receivable stood at $1,659M at September 30, 2025, $3,169M at December 31, and $2,120M at March 31; the quarter collected what the fourth quarter had billed. The deferred-revenue line is cash motion only: the caption’s balance fell from $8,185M to $7,523M, driven, per the filing’s own walk, by the $1.3 billion reclassification to customer liabilities (note 14) and $304M of revenue recognized from the opening balance, partially offset by invoicing in advance of performance; the cash flow statement’s +$575M is the net cash the caption took in during the quarter. Financing activities, same statement: proceeds from issuance of debt, net, $3,290M; repayments of debt $1,335M; common stock issued in a private placement, net of issuance costs, $1,985M. Cash, cash equivalents, and restricted cash fell $810M in the quarter, and the working-capital swing above includes $960M of payables.

(2) Same 10-Q. Cost of revenue $716M against revenue $2,078M; the filing’s own definition places rent, utilities including power, and data-center personnel in cost of revenue, and server and equipment depreciation in technology and infrastructure expense.

(3) Same 10-Q, Note 10: interest expense $427M; interest capitalized $97M; total principal $25,149M across the facilities and notes as listed, with effective rates as disclosed; the unhedged variable-rate language verbatim. June unsecured notes: Form 8-K filed June 18, 2026, accession 0001769628-26-000291: $1,250M of 9.625% senior notes and EUR 2,000M of 8.500% senior notes, both maturing July 15, 2032, senior unsecured. Note 10’s own schedule bridges the figures: contractual interest expense of $483M, plus $41M of amortization of debt discounts and issuance costs and accretion of redemption premiums, less $97M capitalized, equals the $427M expensed. The piece’s 9.1% therefore prices interest incurred plus the amortized cost of raising the money, $483M plus $41M, annualized, over average debt. On contractual interest alone the rate is 8.4% and the flat crossing moves to about 22.5 years; the discounts and fees the $41M amortizes were cash at issuance, so the piece carries them in the cost. The income statement’s interest expense, net, $536M, is the broader caption: per the filing it is “reflected net of capitalized interest,” and interest income is reported separately, in other income. The $109M between it and Note 10’s $427M is financing cost beyond the debt schedule, which the filings do not itemize. Cash interest paid in the quarter was $364M; it differs from interest incurred by coupon timing and the capitalized share. The figures differ by caption, not by contradiction.

(4) Same 10-Q: property and equipment, gross, $40,933M; construction in progress $9,581M; the in-service base is the difference. Annualized EBITDA is the quarter’s $1,003M times four.

(5) Required-yield arithmetic, flat method: cost of money 9.1% plus 100 divided by the life in years; breakeven life equals 100 divided by the spread between produced yield (12.8%) and cost of money, roughly 26.8 years. The flat method charges interest on the full original dollar for the full life and credits the surplus with no return in the meantime; it is the arithmetic of the stack as filed, bullet maturities with nothing retired along the way. Charging every machine dollar at the debt rate is itself a choice among the sources. Equity carries no filed coupon, and the nearest filed price of unsecured CoreWeave risk is the June notes’ 10.47% trading yield (note 9); customer money, the one time the filings priced it, priced as debt: the $230 million Magnetar deposit bore $19 million of interest expense in a single quarter (FY2025 10-K; note 14). The sinking-fund alternative credits each year’s surplus against principal at the same 9.1%: the six-year requirement falls from 25.7% to 22.3%, and the breakeven from 26.8 years to about 14.2; no amortizing instrument appears in the stack (note 8). The produced yield bears every operating cost on the income statement, including the quarter’s $153M of stock-based compensation (cash flow statement); added back, as the company’s own adjusted measure does, the yield is 14.7% ($1,156M per quarter, within a million of the company’s reported $1,157M Adjusted EBITDA), for breakevens of 17.6 years flat and 11.0 credited. The denominator is quarter-end in-service equipment; averaging the quarter’s endpoints ($24,565M at December 31, being total gross of $33,941M less $9,376M of construction in progress per the FY2025 10-K property note, and $31,352M at March 31) gives $27,959M, a 14.4% yield, and breakevens of 18.9 and 11.5. The add-back and the average base together: 16.5%, and 13.4 years flat, 9.2 credited, the shortest crossing these filings permit. A third construction follows the cash flow statement: surplus reinvested in new equipment at fleet economics, an unlevered return at the stated life of roughly minus 7% as reported, minus 3.4% with stock compensation added back; at a negative reinvestment rate there is no breakeven year. Over the six-year schedule the fleet returns, per dollar of cost and before financing, about 77 cents as reported, 89 with stock compensation added back, and 99 at the strongest corner; every corner is short of the dollar. The corners meet: the strongest corner’s 99 cents over six years is an internal rate of return of roughly minus 0.2%, so the flat method’s zero on the waiting surplus is the strongest corner’s own measured rate. Unpaid principal at year six runs from 78 cents, as the piece computes it, to 44 at that corner. The base is not uniformly six-year property: of the $31,352M at March 31, technology equipment, $26,627M, carries the six-year life; software, $827M, three to six years; data center equipment and leasehold improvements, $3,878M, twelve; furniture, $20M, three to five (Q1 10-Q property note; FY2025 10-K Note 1). At each component’s own filed life, longest lives granted, the six-year requirement of 25.7% becomes a blended 24.7%, an equivalent uniform life of about 6.4 years, and the gap at the schedule narrows from 13 points to about 12; the 26.8-year crossing is unchanged, because it uses no schedule. The crossing is the least stable number in the piece: near the current spread, each added point of produced yield removes roughly five to six years, and 13.8% instead of 12.8 moves the flat crossing from 27 years to 21. The six-year multiplication is the most stable. The computation excludes construction in progress from the asset base, annualizes the strongest reported quarter, and ignores taxes. Door arithmetic, flat method throughout: cheaper money holds 9.1% through 2032 and 2.25% thereafter (the March facility’s floating spread over a zero benchmark; note 10). The margin ceiling is annualized revenue, $8,312 million, over in-service gross equipment, $31,352 million: 26.5%. Selling and administration free adds their $233 million per quarter back to EBITDA: 15.8%. The margin allowance at a six-year life is the ceiling less the requirement: 0.8 points of yield flat (2.9 cents per revenue dollar) or 4.2 credited (15.7 cents), against cash operating costs other than selling and administration of $842 million per quarter, 40.5 cents per revenue dollar. All inputs from the same 10-Q except the December 31 property detail, from the 10-K.

(6) CoreWeave FY2025 Form 10-K, accession 0001769628-26-000104, Note 1: useful lives (technology equipment six years; software three to six; data center equipment and leasehold improvements the shorter of lease term or up to twelve years), and verbatim: “Effective January 1, 2023, the Company changed its estimate of the useful life for its computing equipment utilized in data centers from five to six years, reflecting continuous advancements in hardware performance, software optimization, and data center design improvements.” The risk factor quoted appears in the same annual report.

(7) Residual arithmetic: over six years the asset yields 12.8% times six, about 77% of cost; interest at 9.1% times six consumes about 54 points; the shortfall to return principal in full is roughly 100 minus the 3.7-point annual spread times six years, about 77.6% of original cost, required as residual value at year six. The depreciation schedule runs the equipment to zero over the same six years.

(8) The 2026 instruments and maturities, all filed: DDTL 4.0, matures March 2032 (8-K March 31, 2026, accession 0001769628-26-000129); April convertible notes due October 1, 2032 and 9.75% senior notes due 2031 (10-Q Note 16); DDTL 5.0, matures November 15, 2031 (8-K May 18, 2026, accession 0001769628-26-000236); June dollar and euro notes due July 15, 2032 (8-K June 18, 2026). Average tenor at issue approximately 5.9 years. Maturity ladder per the FY2025 10-K: 80% of principal within five years, nothing past 2032.

(9) The comparison tenors are filed by the respective issuers and were set out in “The Price of the Seat” (July 9, 2026) in this series. The trading level of the June notes is market data, not a filing, per LCD (John Atkins, PitchBook/LCD, July 9, 2026): “CoreWeave’s par-priced June 11 offering of 9.625% six-year senior notes slumped to 96.50 (10.42%).” The last reported trade before publication, July 10, 2026, was at 96.28, a 10.47% yield, per FINRA TRACE (CUSIP 21873SAK4). Oracle’s share move on the day of its downgrade is per press coverage of the S&P action (Investing.com, July 9, 2026).

(10) DDTL 4.0: 8-K accession 0001769628-26-000129, Exhibit 99.1: “first investment-grade rated GPU-backed financing”; A3 (Moody’s) / A (low) (DBRS); non-recourse; “secured by substantially all assets of CoreWeave Compute Acquisition Co. VIII, LLC” and an associated customer contract; floating tranche SOFR + 2.25%. DDTL 5.0: 8-K accession 0001769628-26-000236, Exhibit 99.1: Ba2 / BB+; “unconditionally guaranteed by the Parent pursuant to a parent guarantee and pledge agreement” and by subsidiaries, secured by substantially all assets and a 100% equity pledge; proceeds supporting “customer contracts with two large, non-investment grade customers”; SOFR + 4.50%. Remaining performance obligations $98.8B per the Q1 2026 10-Q. That the March facility’s customer is investment grade is inference, labeled as such, from the rating and from the May facility’s stated contrast.

(11) Both exhibits name the arrangers: MUFG and Morgan Stanley as co-structuring agents and joint bookrunners (with Goldman Sachs) in March; Morgan Stanley and Mitsubishi UFJ Financial Group as joint lead arrangers and bookrunners in May.

(12) Applied Digital Corporation Form 8-K/A, accession 0001493152-26-014498, filed April 1, 2026 (event March 30), Item 1.01, and Form 10-Q accession 0001144879-26-000030, Note 18: the ELN-02 lease amendment suspending two of four data halls and the simultaneous re-lease of the same halls to CoreWeave Compute Acquisition Co. VIII, LLC on substantially the same terms, conterminous; the assignment of the ELN-03 lease to the same subsidiary with the parent released; the Unconditional Springing Guaranties of Payment and Performance; the $50,000,000 letter of credit; and the quoted sentences on ratings and on the transactions being favorable to the holders of the 9.250% notes due 2030. Note that “BB” is Applied Digital’s characterization of the parent rating on the Fitch scale; Moody’s rates the parent family Ba2.

(13) Same 10-Q and prior filings: EBITDA against total gross property and equipment, annualized: 12.5% (Q2 2025, $578.7M EBITDA on $18,585M of quarter-end gross), 11.7% (Q3 2025, $682.3M on $23,234M), 8.6% (Q4 2025), 9.8% (Q1 2026, $1,003M on $40,933M); directional only, with the construction-in-progress share rising across the period. The fourth quarter is not separately filed and is derived from the FY2025 10-K less the nine months ended September 30, 2025: operating income of $(46)M less $44M gives $(90)M for the quarter; depreciation and amortization of $2,454M less $1,633M gives $821M; EBITDA of $731M, annualized against $33,941M of total gross equipment at December 31.

(14) The $1.3 billion reclassification from deferred revenue to customer liabilities, its gross-versus-net presentation, and the undefined caption were set out in “CoreWeave, Taken as a Whole” (July 4, 2026) in this series; the underlying disclosure is the Q1 2026 10-Q, Contract Balances. The $230 million recharacterization is the FY2025 10-K: the MagAI Capacity Agreement amendment, the refundable deposit “now consider[ed]… in-substance debt (the ‘Magnetar Loan’) under ASC 470, Sale of Future Revenue,” with no services provided as of December 31, 2025.

(15) CoreWeave has not announced its second-quarter reporting date as of this writing. First-quarter results were reported May 7, 2026 (Form 8-K, accession 0001769628-26-000220); on that cadence the second quarter’s report is expected in August. The annualized building pace is the quarter’s $7,695 million of purchases of property and equipment, times four.

(16) S&P Global Ratings, Research Update: “Oracle Corp. Downgraded To ‘BBB-/A-3’ From ‘BBB/A-2’ On Rising Business Risk And Weaker Cash Flow; Outlook Stable,” July 9, 2026 (primary contact Andrew Chang). Verbatim: “OpenAI remains a key credit risk. We estimate that OpenAI makes up roughly half of the $638 billion in RPO… If OpenAI were unable to pay Oracle, we believe Oracle could be left with massive data center leases that it might be unable to exit or have to re-lease to new tenants under less-favorable terms.” And: “Our base case assumes that Oracle’s FOCF deficit will peak in fiscal 2027 and turn positive by 2029 as profitability ramps, but in our view, the unit economics of the AI infrastructure business remain opaque.” A rating action commentary is the agency’s published opinion, cited as such.