The public argument over this company never ends, and the filing shows why. One side reads the balance sheet and the cash flow statement against the income statement’s category; the other reads the income statement and the contracted tab forward. Each is a correct reading of its pages, so neither lands a blow on the other. This piece holds the whole document at once, through the quality of cash, and finds three statements, each prepared correctly, presenting three businesses: an income statement that earns like a rental company, a balance sheet built like an equipment lessor, and a cash flow statement that moves money like a financing operation. The three cross at one sentence in a footnote, which reclassifies $1.3 billion from deferred revenue, money received for service still owed, to customer liabilities, a line the filing names but does not define. The filing, a required, standard, unaudited quarterly update, states the change and gives no cause. We mark the one footnote and carry a resulting forward-looking question on its resolution and timing: whether the next quarter’s financials, the year-end, or the audit will say anything more about it. The filing does not say that any of them will, though the change itself, current by placement, puts its resolution inside the coming year’s balance sheets.

The phrase belongs to the auditor’s report: an opinion on the financial statements “taken as a whole.” It is a fine phrase, and it describes a reading that, as far as we can find, no one is actually required to perform. The opinion runs to conformity with the framework, and the framework governs one statement at a time. What follows is that reading, performed on CoreWeave’s Form 10-Q for the quarter ended March 31, 2026, filed May 8. (1) Our June piece ran the quality-of-cash test down that company’s filings vertically, line by line. This one runs it horizontally, statement against statement. Everything quoted below is from the one document.

The three portraits

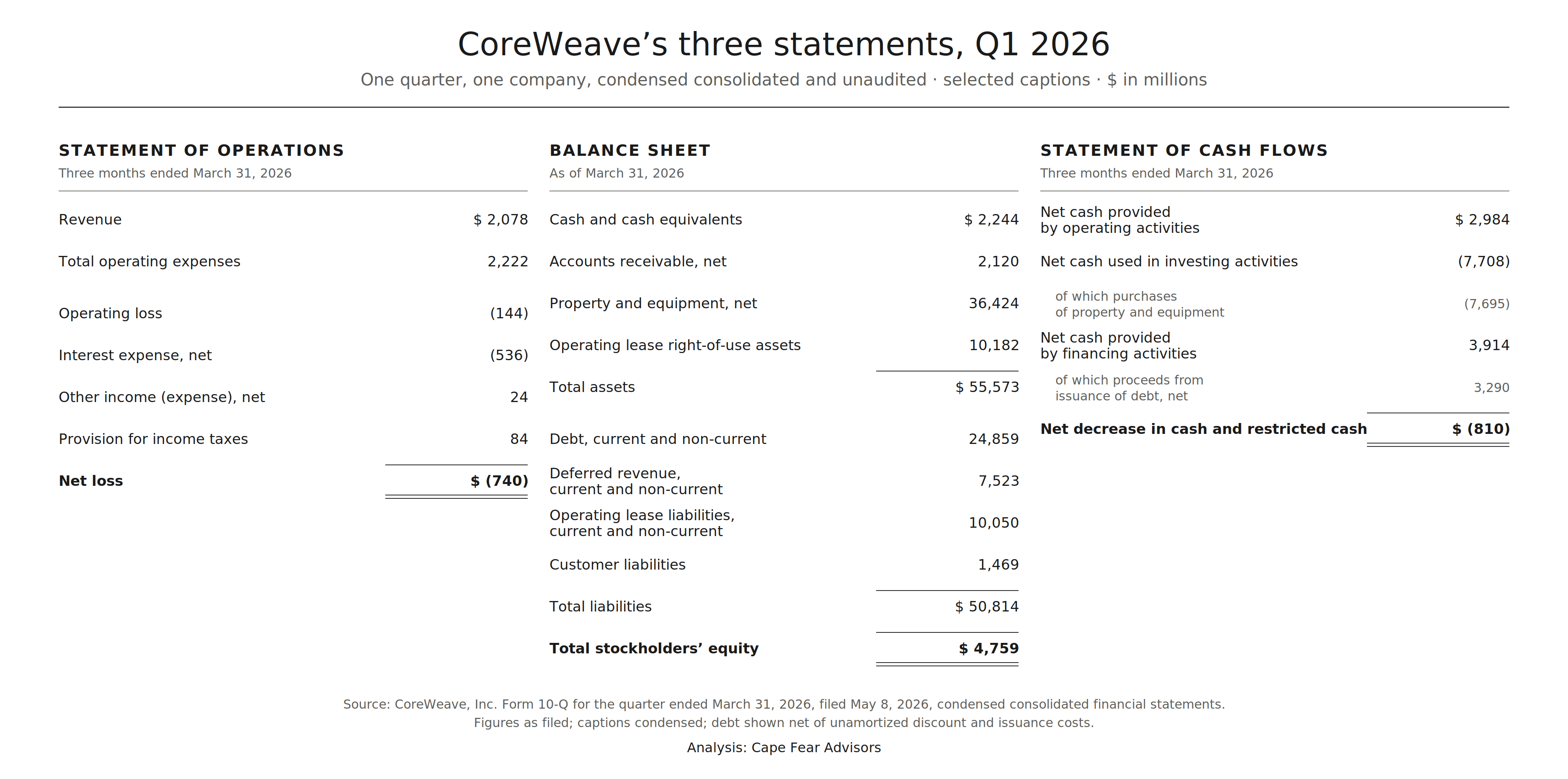

The income statement presents a rental business. Revenue of $2,078 million for the quarter, up from $982 million a year earlier, recognized as service is delivered under the revenue standard, with cost of revenue of $716 million and technology and infrastructure expense of $1,273 million set against it. (2) Depreciation has no line of its own. The quarter’s charge, $1,147 million, appears in the cash flow statement’s reconciliation; on the income statement it is dissolved into the captions, the machines’ wear inside technology and infrastructure, the facilities’ inside cost of revenue. (3) There are no lessor captions: no lease income unwinding, no net investment in leases, no residual accounting. The statement’s theory of the company is a provider of capacity, earning as it serves, period by period. It is prepared exactly as the rules require for that kind of business. Which kind it is, is a presentation judgment the standards commit to management. Management has made it.

The balance sheet presents an equipment lessor. Property and equipment of $36.4 billion net, plus $10.2 billion of right-of-use assets, together 84 percent of total assets of $55.6 billion. (4) The face carries the machines at one number, net. The note beneath splits them: $40.9 billion gross, $4.5 billion already consumed, and $9.6 billion of construction in progress, which neither depreciates nor yet earns, nearly a quarter of the gross. (5) Against the machines: $24.9 billion of debt net of costs, $7.5 billion of deferred customer money, and a footnote tab whose payment expectations run to month eighty-four. (6) Assets that depreciate on schedules; obligations that mature on schedules; customer money that arrived years ahead of the service it purchases. That is the right-hand and left-hand side of a term-financing business, and every line of it is prepared exactly as the rules require.

The cash flow statement presents a financing operation. Operating activities provided $2,984 million, a figure that includes the customer prepayments, against $61 million a year earlier. Investing consumed $7,708 million, of which $7,695 million was purchases of property and equipment. Financing provided $3,914 million, including $3,290 million of new debt. And after all three engines, cash fell $810 million in the quarter. (7) Interest expense, net, ran $536 million, which is 26 percent of revenue, and the quarter’s debt service totaled $1.8 billion: $1.3 billion of principal and $459 million of interest. (8) The statement’s theory of the company is an organism that ingests capital, converts it to equipment, and services the conversion. It is also, of the three, the statement that would not change. Machines are investing, debt is financing, customer receipts are operating, under any name this business carries; the cash flow statement reads identically in every characterization of the company.

Three statements, three businesses, one company. Each portrait is correct. The rules that govern each are statement-local, and nothing anywhere requires the income statement’s theory of the business to agree with the balance sheet’s. The disagreement, if it is one, never appears inside any statement. It lives in the space between them.

The sentence in the footnote

One event this quarter crossed that space, and the filing discloses it in a single sentence:

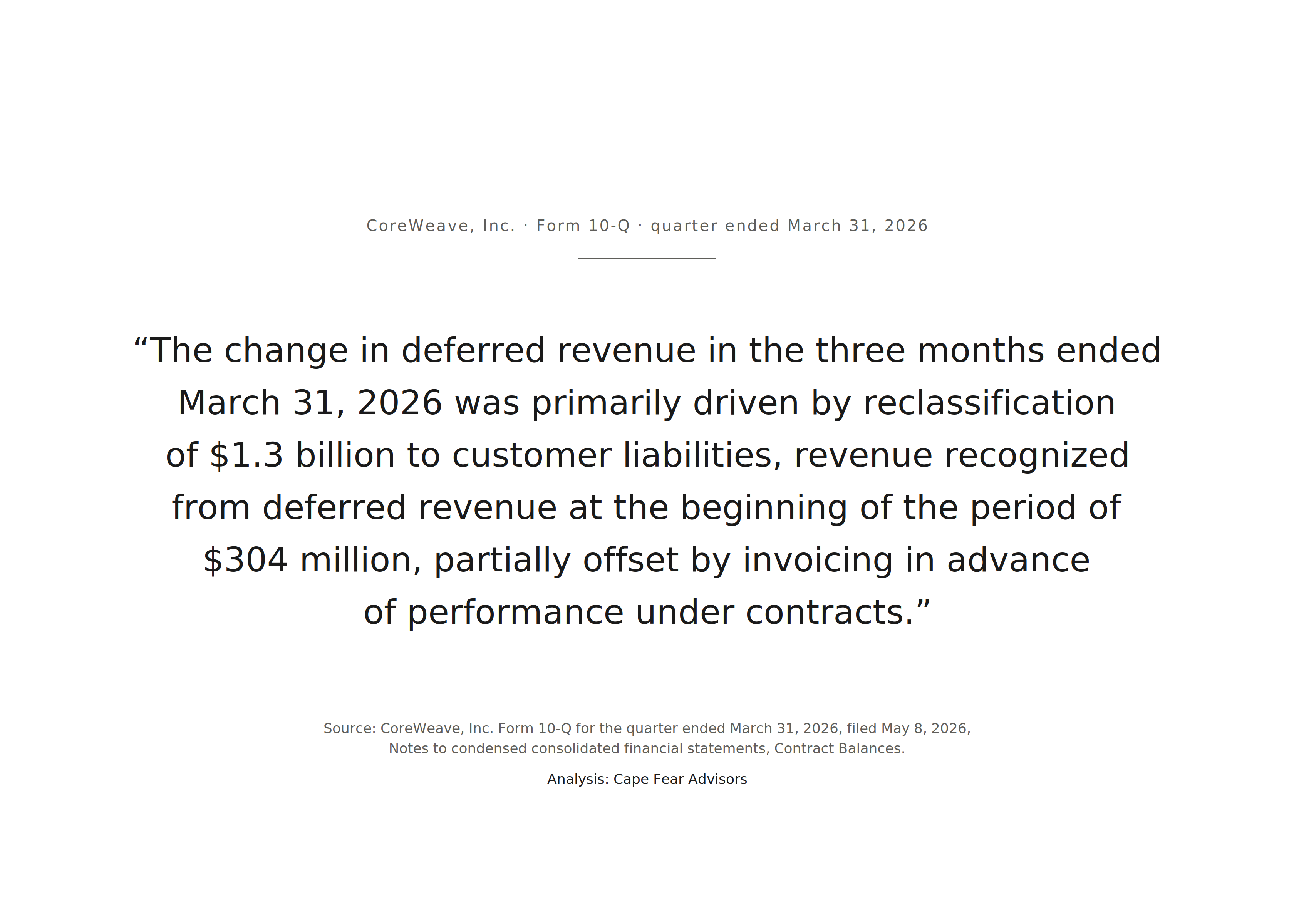

“The change in deferred revenue in the three months ended March 31, 2026 was primarily driven by reclassification of $1.3 billion to customer liabilities, revenue recognized from deferred revenue at the beginning of the period of $304 million, partially offset by invoicing in advance of performance under contracts.” (9)

The two captions are not defined alike. Deferred revenue is money received for performance still owed; it is discharged by serving, and it becomes revenue. Customer liabilities, a line within other current liabilities that stood at $137 million at year-end and $1,469 million at quarter-end, the filing does not define. (10) So the sentence records a change of terminology as much as of amount: in one quarter, $1.3 billion left the caption that resolves into revenue for one the filing names but does not explain, set against $2,244 million of unrestricted cash and $11.1 billion of total liquidity. (11) The classified balance sheet adds tenor. The filing does not map the reclassification between maturity buckets; the columns record the endpoints: deferred revenue beyond twelve months smaller by $1.1 billion over the quarter, deferred revenue within twelve months larger, and the reclassified line current by placement. Wherever the promise sat, the obligation now stands inside the year. (10)

The filing states the mechanics and stops. No cause is given. Two sentences earlier, on the other side of the Contract Balances heading, the filing notes that one customer accounted for 68 percent of accounts receivable at year-end; it does not connect the two, and neither do we. (12) What can be said from the captions alone is this: the entry is correct, and it is correct in the way a term business’s books are correct. A short-cycle rental book contains no relationship that could generate an entry of this kind; a reclassification of this size arises from a long-dated committed arrangement whose accounting basis changed mid-term, and the balance sheet recorded it exactly as such books should. The nature of the change is not filed, and we do not supply one. What changed on the record is the word: money on track to become revenue now sits under a caption the last audited statements left unnamed. The terminology is the event, recorded correctly, in a voice the income statement does not use.

Where does the event register in the cash flow statement? It does not, and the statement is correct not to carry it. Cash flows are indifferent to recognition and presentation decisions; they track cash, and no cash moved. A liability-to-liability change has no line in the body, and the supplemental non-cash schedule records conversions of form, not changes of meaning within a form: its entries this quarter were equipment payables becoming debt, $1,469 million, and, in the prior year, a customer deposit becoming debt. (13) The prepayments themselves remain in operating cash under the character they had on arrival, the only character a cash statement records. But the reclassification happened, and it left its footprint where such footprints belong, one note over, in contract balances. The statement records motion; the notes record meaning; both did their jobs. The meaning lives past the statement, in the notes, because the statement, correctly, will never carry it.

Believed to be firm

The filing discloses the tab itself two sentences further on. Remaining performance obligations of $98.8 billion, of which 36 percent is expected to be recognized in the first twenty-four months, 39 percent between months twenty-five and forty-eight, and the remainder between months forty-nine and eighty-four. (14) The footnote books year seven. A booking for year seven is not a rental; the disclosure was built for promises with tenor, its rule permitting contracts of a year or less to be omitted entirely, and this figure’s own bands place nearly two-thirds of it beyond the first twenty-four months. (15) And the figure is net of the company’s own estimates: the definition subtracts “potential reductions to the transaction price in the future, such as estimates of future potential credits to customers under availability of service agreements, amounts that may not be recognized as revenue due to delivery delays, and estimates of committed cloud computing capacity that the Company has the right to resell.” (16) The tab is stated after the company’s forecast of its own credits, delays, and resales. Estimates, inside the aggregate, disclosed as such.

Form follows the presentation judgment here too. The tab exists as an RPO because the contracts are presented as services. Presented as leases, the same commitments would appear instead in a lessor’s maturity table: undiscounted payments to be received, year by year for each of the first five years, with a total for the years beyond. (17) The lease form of the disclosure is more granular than the service form’s bands. Whichever presentation is chosen, the chosen one here discloses less about time.

And the categorization answers less than it appears to. The RPO does not evidence the services reading; it presupposes it. It inherits the judgment, so it cannot test it. Nor is the tab on the balance sheet: the funded portion, cash received ahead of performance, is the deferred revenue liability; the remainder of the $98.8 billion is a disclosed aggregate, neither asset nor liability. The polarity of the presentation runs through everything downstream. Presented as services, the future dollars stand mostly outside the statements, and the recognized sliver is performance the company owes. Presented as leases at full depth, the same dollars become an asset, a receivable, and assets carry valuation machinery that disclosures do not: allowances, measured against the credit of named counterparties, tested each period. Under the reading on file, the accounting asks no one to assess the collectibility of the $98.8 billion, because nothing about it is an asset. Disclosures are stated; assets are tested. The one movement on the record this quarter ran in the other direction: the $1.3 billion reclassified to customer liabilities.

The load the tab carries points the same way. A seven-year revenue commitment, load-bearing for financing already in place and for build-out commitments already made, sits on its face at odds with a presentation of a services or rental business.

For more than thirty years, the disclosure rules had a name for this figure: backlog, and the required words were “dollar amount of backlog orders believed to be firm.” The qualifier was carried on the face of the requirement. That requirement was removed in 2020, in favor of principles, two years after the revenue standard installed the successor. (18) The successor’s name is remaining performance obligations, which asserts more and confesses less, and the figure under it is now larger than the balance sheet beneath it. The accounting board reviewed the standard that created it and closed the review, concluding the standard works as intended, and opened no project to revisit it. (19) The last time obligations of this character accumulated in footnotes at national scale, the repair took fourteen years from the study that found them to the standard that surfaced them. (20)

How it goes missing

Every statement is correct under its own rules. Every analyst reads the pieces their work relies on, and reads them correctly. And the profession’s own consistency check runs across periods, not across presentations: the auditing standard titled Evaluating Consistency of Financial Statements asks whether “the comparability of the financial statements between periods has been materially affected by changes in accounting principles or by material adjustments to previously issued financial statements.” (21) This period against last period. Nothing is skipped, and nothing here says otherwise.

What remains is a distinction, not a fault. The statements articulate: net income rolls to equity, cash rolls to cash, every figure that must equal another figure equals it, and an entire industry polices the tying. Whether the statements agree, whether the three share one theory of what the business is, is a different question. The cash flow statement, identical under every characterization of the business, is the fixed point that makes the other two statements’ choices visible as choices; and the duties broad enough to reach the question of agreement, the certification that the filings fairly present and the rule requiring whatever further information is necessary to make the statements not misleading, are tested after the fact. (22) In the meantime, the question sits with whoever holds the statements.

Which returns everything to the critical audit matter and the judgment call, because the record already points there, correctly filed. The presentation of the contracts as services is a judgment the standards commit to management. Management exercised it, and the exercise is not gradable as wrong, because it is a judgment. The auditor of the annual statements then did its own job: it identified that judgment, along with the consolidation accounting for a data-center joint venture, as the audit’s critical matters. (23) The disclosure is addressed to whoever holds the statements; it says: this choice was critical, weigh it. The two matters flagged are not details inside the portraits. They are the portraits’ boundaries, the first deciding which income statement this company has, the second whether an entity stands inside these statements or outside them. Management chose. The auditor flagged the choosing. And the weighing was handed, explicitly, to the one seat at the table with no rulebook: the holder of the whole.

The rulebook behind that flag is specific, and it was followed to the letter. A critical audit matter is any matter, drawn from those communicated or required to be communicated to the audit committee, that relates to accounts or disclosures material to the financial statements and involved especially challenging, subjective, or complex auditor judgment. (24) For each one, the auditor must do four things: identify it, describe the principal considerations that led to the determination, describe how it was addressed in the audit, and refer to the relevant accounts or disclosures. The auditor may not use the communication to publish company information that is not already public, so the channel cannot reveal the contracts; it can only point at their disclosed shadow. (25) And the standard prescribes the sentence that must precede every such communication: that communicating these matters “does not alter in any way our opinion on the financial statements, taken as a whole,” and that the auditor is not, by communicating them, providing separate opinions on the matters or on the accounts they relate to. This piece’s title is quoted from that required sentence. The rulebook separates, in one breath, the opinion on the whole from the flag on the matter; the pointing is expressly not an opinion. Identify, explain, describe, refer. Four duties, four performances, to the letter.

So the decision before whoever holds the statements is the same one the auditor flagged, and it is simple to state: is this a services business? The RPO does not answer it; the RPO takes the answer as given. The statements do not answer it; each is correct under either answer, within its own rules. The contracts answer it, privately. What the statements carry is the set of judgments built on that answer, and relying on those judgments, and testing them, is what financial statements are there for.

One more fact about the pointer: it is annual. Critical audit matters exist only in the auditor’s report on the audited annual statements. The quarterly filings between them, including the one this piece reads, are unaudited; they receive a review, inquiries and analytical procedures, which expresses no opinion and carries no critical audit matters. (26) The footprints land quarterly. The pointer updates once a year. For the three quarters between annual reports, whoever holds the statements holds them alone. Stated plainly: the critical audit matters belong to an audited annual presentation; the reclassification belongs to an unaudited quarterly update. They are different classes of document, and the record points forward on its own terms: the next audited annual statements are the venue where matters of this kind may be more fully discussed and disclosed.

Two consistent companies, and a third

Suppose the document were made to agree with itself. There are two ways, and each has a price.

Make it a rental business everywhere, and the balance sheet must follow the income statement: short obligations, minimal prepayment float, no month-eighty-four band, and, above all, no financing of the kind the filing describes. The debt footnote lists non-recourse facilities and vendor financing arrangements tied to equipment additions, and the filing describes what the term lenders hold: the facilities are “collateralized with the assets underlying the contributed contracts and the pledged contractual cash flows.” (27) That is lending against contracts. A contract can be contributed only if it exists, and its cash flows pledged only if they run long enough to repay the draws; a short-cycle rental book has neither to offer. A company financed contract by contract cannot, consistently, be a short-cycle rental operation. The rental reading, applied to all three statements, leaves the company to borrow on some other basis than the contracts, at whatever terms a pool of depreciating machines earns on its own name. The filing’s own liabilities are the evidence that nobody lent to that company.

Make it a lease business everywhere, and the change arrives at two depths. At the shallow depth, operating-lease treatment, the changes are few: the machines stay on the balance sheet, depreciation continues, the cash flow statement does not change a line, and the income statement re-captions, lease income for service revenue, the same dollars under different words, with timing differences where the consideration is variable or usage-based. The visible change is the tab, which dissolves as an RPO and reappears as the maturity table of note (17), disclosing more about time than the bands it replaces. Counted in changed lines, this is the smallest alternative on the table: no line of the cash flow statement, no dollar of the balance sheet, the captions of one statement and the form of one note.

At the full depth, for contracts that transfer substantially all the economics of the machine, dedicated assets, terms consuming most of the equipment’s life, financing components the accounting already admits, the lease is a sale with financing attached: the equipment leaves the balance sheet and a net investment in leases arrives, a receivable, a financial asset, and the credit assessment the tab has never received arrives with it. (28) The customers, at either depth, book right-of-use liabilities on their own balance sheets. At the full depth the income statement becomes a financing spread over residual risk, and the multiple, wherever the market sets it, is thereafter a multiple of the machine and not of the word.

The third company is the one on file: rental on the income statement, lessor on the balance sheet, financier in the cash flows, each per the rules. It is the version in which no one is required to book the debt, assess the credit by name, or re-price anything, because no single statement, read under its own rules, calls for it. It is internally consistent, and it holds. What it leaves unanswered is the question the three raise only together, and that question stays open until something on the record closes it.

The question

The contracts know which business this is. Whether the provider can substitute the machines, whether the customer directs their use: these are facts, held by two parties who both know the answer, in documents the public does not read. Assume the contracts are well made and do exactly what they were written to do; whatever tensions exist between the statements’ postures are resolved there, privately. Nothing in this piece requires otherwise. The filing is not required to say, and it does not.

Nothing on the record says the income statement’s presentation is the way to hold the business; the record says only that management chooses to hold it this way, and that the choice was critical. Both of those statements are correct. Neither is an answer. And the presentation is correct in a further sense: the standards commit the judgment to management, and the exercise of a committed judgment is its correctness. What stays open is not whether the presentation is correct but how it is to be read. This piece does not supply the reading either, because it cannot: the presentation may be exactly right in substance as well as in form, the contracts may be genuinely and substantively services, and each statement’s portrait may be the correct rendering of a business that is simply hard to draw. We note what the documents themselves put on the table: that the lenders’ facilities and the income statement’s caption rest on different answers to the same question, and that the three statements, held together, put that question to anyone willing to hold them. That is all, and it is enough.

The register solved this problem before the industry existed, which is why it keeps returning to these pieces. At the drawer, the word and the cash were one event: the sale, the record, and the bell, simultaneous, in public. Modern statements distribute that event across classifications, correctly, and so the classifications are where the listening happens now. Words are not the decoration of these documents; they are the definitions a change must pass through to become visible. The reclassification is noted here, and it merits notice, because it is exactly that: a word changing on the record.

This piece reaches no conclusion, because the reading it performs does not produce one. It produces a requirement: a comprehensive reading of this company needs everything, three statements, the notes beneath them, the annual report and its critical matters, the credit documents behind the debt table, held at once, because the meaning is distributed across them and resides in no single place. And it produces a baseline. The next quarterly update re-measures the balances quoted here: the customer-liabilities line and how it resolves, the deferred revenue that fell $0.7 billion in the quarter while debt rose $3.5 billion, the bands of the tab. (29) The next annual report renews the audited presentation and its critical matters, and that comparison, audit against audit, this reading against the next, is where more may become visible. Nothing here concludes. The nearer question, what the reclassified line is, resolves inside the coming year, as the balance discharges, or is explained, or moves again; any of those is an answer. The larger question, whether this is a services business, keeps the audit’s timetable, not the quarter’s. The tab still stands at $98.8 billion; the record, held whole, has now been read once, so the next reading has something to be held against, and we will be reading for both.

Notes

(1) CoreWeave, Inc., Form 10-Q for the quarterly period ended March 31, 2026, filed May 8, 2026 (unaudited condensed consolidated financial statements). All quotations and figures in this piece are from this filing unless otherwise noted.

(2) Condensed consolidated statements of operations: revenue of $2,078 million (three months ended March 31, 2026) versus $982 million (2025); cost of revenue $716 million; technology and infrastructure $1,273 million; operating loss $(144) million; net loss $(740) million.

(3) Condensed consolidated statements of cash flows, reconciliation of net loss to operating cash: depreciation and amortization of $1,147 million (three months ended March 31, 2026) versus $443 million (2025). MD&A: technology and infrastructure expense “consists of costs associated with our infrastructure, such as depreciation and amortization related to our servers, switches, networking equipment and internally developed software”; cost of revenue includes “depreciation of power installation and distribution systems.” The statements of operations carry no separate depreciation caption; each expense caption absorbs its allocable share, and the allocation between captions is not quantified in the filing.

(4) Condensed consolidated balance sheets: property and equipment, net, $36,424 million; operating lease right-of-use assets $10,182 million; total assets $55,573 million. The two asset captions sum to 84 percent of total assets.

(5) Property and equipment note: technology equipment $26,627 million; software $827 million; data center equipment and leasehold improvements $3,878 million; furniture, fixtures, and other assets $20 million; construction in progress $9,581 million; total property and equipment $40,933 million; less accumulated depreciation and amortization $(4,509) million; net $36,424 million. Construction in progress is 23 percent of gross property and equipment. The note states depreciation and amortization on property and equipment of $1.1 billion for the quarter, and $97 million of interest capitalized.

(6) Total debt, net of unamortized discount and issuance costs, $24,859 million (principal $25,149 million); deferred revenue, current and non-current, $7.5 billion at March 31, 2026.

(7) Condensed consolidated statements of cash flows: net cash provided by operating activities $2,984 million (versus $61 million); net cash used in investing activities $(7,708) million; net cash provided by financing activities $3,914 million, including proceeds from issuance of debt, net, $3,290 million; net decrease in cash, cash equivalents, and restricted cash $(810) million.

(8) Interest expense, net, $(536) million (versus $(264) million). MD&A, liquidity: “our cash flows dedicated for debt service requirements totaled $1.8 billion, which includes principal payments of $1.3 billion and interest payments of $459 million, inclusive of $95 million related to capitalized interest.” The property and equipment note separately reports $97 million of interest capitalized during the quarter; the two figures measure payment and capitalization respectively, and are the filing’s own.

(9) Notes to condensed consolidated financial statements, Contract Balances, quoted in full as it appears.

(10) Other current liabilities note: customer liabilities of $1,469 million at March 31, 2026 and $137 million at December 31, 2025. The filing does not further define the caption or state the cause of the reclassification. The caption does not appear in the Company’s Form 10-K for fiscal year 2025 (filed March 2, 2026); at December 31, 2025 the $137 million the quarterly filing labels customer liabilities was carried within that annual report’s undifferentiated other current liabilities of $162 million. The Form 10-Q introduces the line, and neither filing defines it. Balance sheet: deferred revenue, current, of $2,130 million at March 31, 2026 and $1,709 million at December 31, 2025; deferred revenue, non-current, of $5,393 million and $6,476 million at the same dates. The bucket movements, $1,083 million down beyond twelve months and $421 million up within, net to the $0.7 billion decline in total deferred revenue.

(11) Cash and cash equivalents of $2,244 million at March 31, 2026, excluding restricted cash. MD&A reports total liquidity of $11.1 billion, of which $8.8 billion is availability under the revolving credit facility and delayed draw term loan agreements; the filing describes borrowings under the term facilities as used primarily to finance the acquisition and installation of computing infrastructure, and remaining revolver capacity was $686 million.

(12) Concentration disclosure: Customer A at 68 percent and Customer D at 11 percent of accounts receivable, net, as of December 31, 2025; as of March 31, 2026, Customers A, B, and C at 39, 17, and 22 percent. The concentration sentence closes the passage directly above the Contract Balances section, two sentences before the reclassification sentence; the adjacency is a fact of the document’s layout, no connection is stated in the filing, and none is asserted here.

(13) Supplemental disclosures of cash flow information, non-cash investing and financing activities: “Reclassification of liabilities related to property and equipment additions to debt upon execution of OEM financing arrangements, $1,469 million” (three months ended March 31, 2026); “Reclassification of customer deposit to debt, $230 million” (three months ended March 31, 2025). The $1,469 million figure coincides numerically with the customer-liabilities balance in note (10); they are different items. Three separate $1.3 billion figures likewise appear in this filing (the reclassification to customer liabilities; the outstanding balance of the DDTL 4.0 facility; the quarter’s principal payments) and are unrelated.

(14) Contract balances note: $98.8 billion of unsatisfied remaining performance obligations, with the timing bands as quoted.

(15) ASC 606-10-50-14 permits omission of the disclosure for contracts with an original expected duration of one year or less; the expedient is elective, and the filing does not state whether it is applied. The two-thirds figure is the complement of the 36 percent band at note (14).

(16) Contract balances note, definition of RPO, quoted verbatim.

(17) ASC 842-30-50 requires a lessor to disclose a maturity analysis of lease payments to be received, showing undiscounted cash flows on an annual basis for a minimum of each of the first five years and a total for the years thereafter. The RPO bands are as quoted at note (14).

(18) Regulation S-K Item 101(c), as in effect for more than thirty years, required disclosure of “dollar amount of backlog orders believed to be firm”; the SEC’s modernization of Items 101, 103, and 105 (adopted August 26, 2020, effective November 9, 2020) replaced the prescribed list with a principles-based approach under which backlog is disclosed if material.

(19) FASB, Post-Implementation Review Report: Topic 606—Revenue from Contracts with Customers, presented to the Financial Accounting Foundation Board of Trustees in November 2024: the report concludes the standard meets its intended purpose, observing that Topic 606 “provides understandable and operational guidance that can be applied as intended”; the IASB’s parallel review of IFRS 15, published September 30, 2024, concluded the requirements are “working as intended,” with remaining application questions deferred to a future agenda consultation.

(20) SEC staff, Report and Recommendations Pursuant to Section 401(c) of the Sarbanes-Oxley Act of 2002 On Arrangements with Off-Balance Sheet Implications, Special Purpose Entities, and Transparency of Filings by Issuers (June 15, 2005), estimating by extrapolation that there “may be approximately $1.25 trillion in non-cancelable future cash obligations committed under operating leases that are not recognized on issuer balance sheets, but are instead disclosed in the notes to the financial statements,” and recommending “that the accounting guidance for leases be reconsidered”; ASU 2016-02 (Topic 842) was issued February 2016 and effective for public companies in 2019, fourteen years after the study. The report is by the Commission staff, which notes the Commission expressed no view on its findings.

(21) PCAOB AS 2820, Evaluating Consistency of Financial Statements, paragraph .02, quoted verbatim.

(22) Exchange Act Rules 13a-14 and 15d-14 (certifications that the report does not contain untrue statements or omissions and that the financial statements “fairly present in all material respects the financial condition, results of operations and cash flows”); Regulation S-X Rule 4-01(a) (financial statements must include “such further material information as may be necessary to make the required statements, in the light of the circumstances under which they were made, not misleading”). Certification language conformed to Exhibits 31.1 and 31.2 as filed with the Form 10-Q.

(23) Deloitte & Touche LLP, Report of Independent Registered Public Accounting Firm, CoreWeave, Inc. Form 10-K for the fiscal year ended December 31, 2025 (filed March 2, 2026), discussed in our June 13 piece. Two critical audit matters. The first, Revenue Recognition, names among the significant judgments for certain customer contracts “the determination of whether the contracts with customers are accounted for as a revenue contract for cloud-based services or a lease contract for cloud computing equipment, and the identification and treatment of contract terms that may impact the timing and amount of revenue recognized.” The second, Consolidation Accounting for a Variable Interest Entity, concerns whether the company is the primary beneficiary of, and so must consolidate, a joint venture with a third-party infrastructure developer formed to acquire and develop a multi-phase data center campus. A critical audit matter identifies decisions whose making involved especially challenging, subjective, or complex judgment and commends them to the attention of whoever holds the statements; it is not a ranking of business risk, and it is not a criticism.

(24) PCAOB AS 3101, The Auditor’s Report on an Audit of Financial Statements When the Auditor Expresses an Unqualified Opinion, Appendix A (definition of critical audit matter) and paragraphs .11 through .14 (determination, communication, and documentation requirements); the four communication elements are as enumerated in the standard.

(25) AS 3101.15 (prescribed language preceding critical audit matters, quoted in part); Note 2 to paragraph .14 (the auditor is not expected to provide information about the company that has not been made publicly available by the company, unless necessary to describe the principal considerations or how the matter was addressed).

(26) The condensed consolidated financial statements in the Form 10-Q are unaudited. Interim financial information of SEC registrants is reviewed by the independent auditor (PCAOB AS 4105, Reviews of Interim Financial Information; Regulation S-X Rule 10-01(d)); a review consists principally of inquiries and analytical procedures, and expresses no opinion. Critical audit matters are communicated only in the auditor’s report on the audited annual financial statements.

(27) Debt note: the DDTL 4.0 facility is described in the filing as “a non-recourse delayed draw term loan facility,” with an outstanding balance of $1.3 billion at March 31, 2026; OEM financing arrangements per note (13). MD&A, liquidity: the delayed draw term loan facilities “are collateralized with the assets underlying the contributed contracts and the pledged contractual cash flows, generally from investment grade counterparties.” The underlying credit agreements and their collateral and covenant terms are filed as exhibits and are the subject of continuing review.

(28) Under the lease reading, lessor classification (sales-type, direct financing, or operating) would be determined contract by contract under ASC 842; a net investment in leases is a financial asset within the scope of the credit-loss standard (ASC 326). The invariance of the cash flow statement asserted earlier rests on ASC 842-30-45-5, under which a lessor classifies cash receipts from leases within operating activities “regardless of whether the lease is classified as a sales-type, direct financing, or operating lease” (rationale at BC335 of ASU 2016-02: leasing is the lessor’s revenue-generating activity); the lone exception, depository and lending lessors within the scope of ASC 942, does not apply to the company. Machine purchases remain investing and debt remains financing under every reading, and the commencement recognition of a net investment is non-cash. No restatement is asserted or implied; the paragraph describes the disclosure architecture each consistent reading would produce.

(29) Deferred revenue of $8.2 billion at December 31, 2025 and $7.5 billion at March 31, 2026; total debt principal of $21,615 million and $25,149 million at the same dates; scheduled principal payments of $6,066 million for the remainder of 2026 and $5,652 million for 2027.

The quality of cash, applied horizontally to CoreWeave’s Form 10-Q for the quarter ended March 31, 2026. Source: CoreWeave, Inc. Form 10-Q, filed May 8, 2026; Deloitte & Touche LLP, Report of Independent Registered Public Accounting Firm in CoreWeave, Inc.’s Form 10-K (fiscal year ended December 31, 2025). Figures verified against the primary filings. Analysis: Cape Fear Advisors.

Greg Collins serves as CEO of C3 Metrics, a marketing measurement and analytics firm, and maintains an advisory practice at Cape Fear Advisors focused on structural analysis and strategy.

The author holds no position in the securities discussed.

This article is also available on Substack.

Start a Conversation →