In its most recent quarter, NVIDIA sold $81.6 billion of product at a 75 percent gross margin, collected on receivable paper of about 45 days, before any machine it sold had earned anything for anyone. This piece reads the fourth house the way this series read the first three, by where the filings put the money, and finds a revenue engine where the other houses hold placements. The engine is paid in days, at a price that could not be shopped, because the buyers’ own customers wrote NVIDIA into their contracts, and its income statement runs on the machines being bought rather than the machines working. Two worries travel with this house, and the filings measure both. The first is exposure, the stakes it holds in its own customers; the filings size it line by line, from the $2 billion CoreWeave stake, about three days of quarterly profit, to an equity portfolio near $82 billion with $27 billion more committed, and the piece walks the divisions. The second is the shape of demand, and there the filings hold one trace: between February’s annual report and May’s quarterly report, one word left NVIDIA’s customer taxonomy, and the comparable periods were recast. In June the engine went to the bond market its customers depend on and drew $25 billion, nothing pledged. The inputs are the filers’ own, cited by accession; where a number rests on this series’ earlier arithmetic, the piece links it. NVIDIA reports in late August, within days of CoreWeave’s own print, and the piece ends there: with the five lines that show whether the cash arrives on the terms already filed, and how much of it began as NVIDIA’s own.

The fourth card

Days ago this series read three filings from one quarter and found one asset in three forms. Microsoft held its stake through an equity method that adds the gain to net income and excludes it from the measure the market is asked to watch. Amazon held convertible notes that release the gain through other income as conversions occur. Alphabet held an equity derivative carried at approximately nothing. One asset, three forms, three placements, and the closing line of that piece: the form decides when the gain shows.

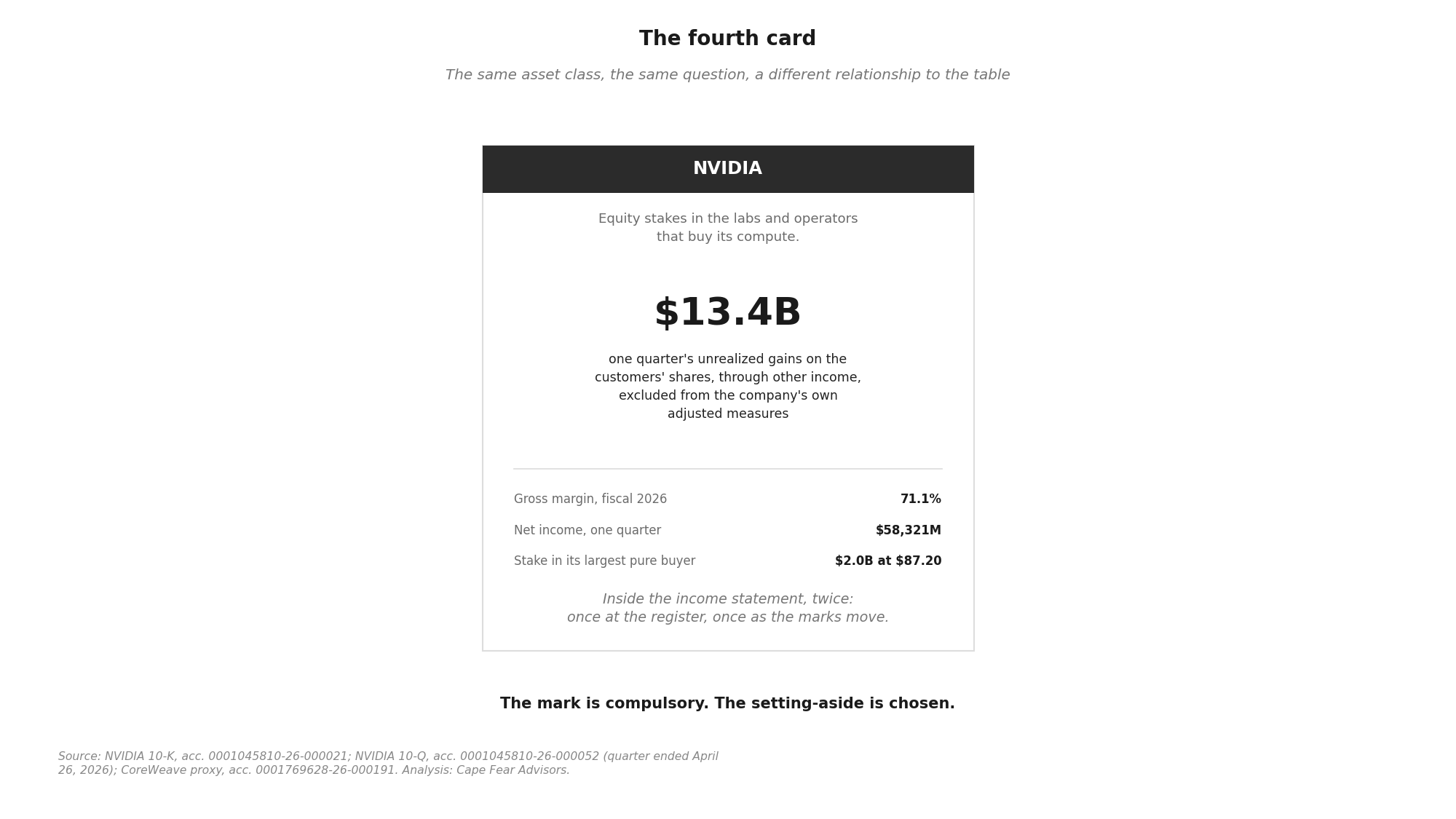

The fourth house completes the set, and its card reads like the others. NVIDIA holds equity stakes in the labs and operators that buy its compute, and in its most recent quarter those stakes produced roughly $13.4 billion of unrealized gains on publicly held positions, flowing through other income into a $58.3 billion quarterly profit. (1) The asset class is the same one the three houses chose. The form is direct equity; the placement is the income statement; the gain shows as the marks move. On those terms NVIDIA is a house like the others, the fourth to be dealt in.

Four houses, four answers, no two alike, and the fourth answer is doubled: NVIDIA is marked by force of listing, its largest pure buyer being public, and its own adjusted measures exclude gains and losses from equity securities. (1) The mark is compulsory. The setting-aside is chosen.

The resemblance ends at the register. The first three houses placed cash into the asset class and wait, each in its chosen box, for the machines to make the placements good. The fourth house also sells the machines. That difference changes the house’s relationship to the table, and the rest of this piece prices it.

The house has four sides

Each side is filed, and three of the four are filed by the counterparty.

The first side is the register itself. CoreWeave’s annual report states the arrangement in one sentence: “as a result of our obligations in our current customer contracts, all of the GPUs used in our infrastructure today are NVIDIA GPUs.” (2) NVIDIA’s position is not CoreWeave’s procurement preference; CoreWeave’s customers wrote it into their contracts. The demand side specified the supplier, which means the one price in this system that cannot be shopped is the price of the machine. What that price contains is also filed: for the fiscal year ended January 25, 2026, NVIDIA reported $215.9 billion of revenue and $153.5 billion of gross profit, a 71 percent gross margin; in the quarter ended April 26, 2026, the margin was 75 percent. (1) Of every dollar that reaches NVIDIA, about 29 cents leaves as cost. The rest is the take, booked at sale and collected on paper the filings size at about 45 days. (6)

The second side is the equity. On January 23, 2026, CoreWeave sold NVIDIA 22,935,780 shares of Class A common stock at $87.20 per share, $2 billion in cash. (3) The transaction reconciles across three documents: the $2 billion announced in the first-quarter press release, the price and share count in the proxy statement and the annual report’s subsequent-events note, and the $1,985 million, net of issuance costs, in the audited cash flow statement. Three documents, one leg, and the $15 million between gross and net is the issuance cost the cash flow statement’s own caption names.

The third side is the order forms. Under a Master Services Agreement dated April 2023, NVIDIA is CoreWeave’s customer: CoreWeave provides “infrastructure and platform services through fulfillment of order forms submitted to us by NVIDIA,” and NVIDIA paid approximately $326.3 million under the agreement in 2025 and $59.6 million in the first quarter of 2026. (3) The seller of the machines rents back their output. The $59.6 million paid in the first quarter is about 3 percent of CoreWeave’s revenue, in a quarter whose operating result was a loss of $144 million; whatever margin the order forms carry, the quarter had no operating profit for them to exceed. (5) NVIDIA sits behind CoreWeave as a holder, across from it as a supplier, and in front of it as a customer, and the exhibit index carries the master agreement for each position.

The fourth side is not a position but a fact about the other three: no single document shows them together. NVIDIA appears nowhere in CoreWeave’s related-party footnote, because the accounting definition of a related party turns on voting influence, and NVIDIA’s stake sits below that line. The same relationships fill more than a page of the proxy statement, because the securities-law definition turns on five percent ownership, and NVIDIA owns more than five percent of its customer. (3) One relationship, two disclosure regimes, visible in one and absent from the other. The reader who checks only the financial statements meets a supplier. The reader who checks the proxy meets the house.

One proportion, filed: NVIDIA accounted for 17 percent of CoreWeave’s total purchases from suppliers in 2025, with the balance of the fleet arriving through intermediaries, and every GPU in the fleet is NVIDIA’s. (3) The direct line item understates the position; the contracts state it in full.

Two sides of one counter

This series has already priced what the machines earn. On CoreWeave’s own filed numbers, a dollar of machines returns between 77 and 99 cents over CoreWeave’s own depreciation schedule, before the cost of any money, across every construction the filings permit. (4) The machine loses on its own schedule at every corner of that grid; the player sat down at 99 cents on the dollar at its most favorable corner, short before the first card was dealt.

NVIDIA’s filed number belongs beside it. The machine that returns at most 99 cents to its owner carried a margin of roughly 71 cents to its seller on the day it was sold. Read together, the two filings describe a system that works: silicon that costs about 29 cents to produce, per dollar of sale price, goes on to generate 77 to 99 cents of operating cash for its owner. They also describe where it goes, and on what clock: nearly all of it reaches NVIDIA on receivable paper of about 45 days, and what remains reaches CoreWeave over six years, spread thinner than the machine’s own price. Days against years is the asymmetry, and both sides of it are filed. The machine costs exactly its price; the money that pays the price costs more. Add the interest on what CoreWeave raised, and the outlay passes the price while the returns stop short of it; the last piece put the roads out at fourteen years, twenty-seven, and never. The surplus and the shortfall are the same number, seen from opposite sides of the counter.

One guard travels with the comparison. NVIDIA’s margin is a company-wide figure; CoreWeave’s equipment dollars flow partly through intermediaries, as the 17 percent direct-purchase figure shows; and no dollar-for-dollar mapping between the two filers is claimed here or available in the filings. The two numbers are poles, each filed by its own filer, and the space between them is where the other participants live. What other buyers pay NVIDIA is not filed, and this piece prices only the pair that files both sides of one relationship. One more filed fact: the participant that knows both the machine’s price and its cost took the order form over owning a fleet. The choice is filed. The reason is not.

A chain follows; it is this piece’s reading, not any filing’s sentence. At filed prices, NVIDIA’s margin and CoreWeave’s shortfall are one number. A machine that returns less than a dollar cannot fund a dollar of its own replacement. So the next machine is bought from the buyers’ raises, and the raises are priced in public. The last piece measured how long the raises must continue; the tape on CoreWeave’s unsecured notes prices what continuing costs, every trading day. Read that way, the durability of NVIDIA’s order book is quoted in its customers’ cost of debt. And the same tape prices the stake: the gain NVIDIA still holds in its customers pays only if the raises keep arriving, so the order book and the equity line wait on the same quoted rate. NVIDIA’s own taxonomy bounds the chain: half of data center revenue is attributed to hyperscalers, who file no per-machine economics, and the chain reaches only the class the recast category no longer separates.

The circuit, priced

The public argument of the moment is what to call a supplier that invests in its customers. The legs are filed, and pricing them is shorter than naming them. The counter transaction is the simple one, cash on the barrel: the machine crosses one way, the cash crosses the other, and the register closes. Every leg below is that transaction stretched, in time or into another form, and the quality of cash is the measure of the stretch.

Out: CoreWeave paid its suppliers for a fleet whose in-service cost stood at $31.4 billion in March, money raised in public at $25.1 billion of principal, 59 percent of it at effective rates of 10 percent or higher, beside the equity placements and the customers’ advances. (5) Back: $2 billion of equity in January, at $87.20, and $386 million of compute rental across five quarters. What returned to CoreWeave’s side is a fraction of what crossed to NVIDIA’s, and the largest returning leg came back not as revenue or rebate but as ownership. The legs interlock in one sentence, every clause filed: the money that bought the machines included NVIDIA’s equity, the revenue that services the machines includes NVIDIA’s rent, and NVIDIA’s income includes both the machines’ price and the marks on CoreWeave’s shares. Past that sentence, the circularity is not the finding. The proportions are, and they rank NVIDIA’s interests without guesswork.

The $2 billion stake amounts to about a quarter of a single quarter’s equipment purchases by CoreWeave and about three days of NVIDIA’s quarterly net income, and it can halve or double quietly inside a sixteen-billion-dollar other-income line. The purchases are the profit: the machines’ being bought, at the margin NVIDIA files, is the income statement. If the machines repay their owners, NVIDIA’s equity compounds. If the machines merely keep being bought, NVIDIA collects again. And the two roads are not independent; NVIDIA holds the dial between them, and this is a reading, not any filing’s sentence, though both of its ends are filed. Each architecture NVIDIA ramps, in its own MD&A’s language, shortens the earning life of the fleets its stake is a claim on. The fleets’ owner files the other end: a risk factor that describes “cycling out older components of our infrastructure and replacing them with the latest technology available.” (2) The faster the machines are replaced, the more often the ante is collected, and the less the residual behind the equity is worth. The ramp is filed every quarter. Which take it favors is arithmetic. The filings describe no outcome in which the fourth house has not already been paid.

The filings describe no outcome in which the fourth house has not already been paid.

The form of the support carries its own information, all of it filed. A price cut would have printed at the register, in the margin, immediately. A loan would have printed as paper with a maturity and a rate, able to sour in public, on schedule. The equity printed as neither: no coupon, no maturity, nothing that ever comes due, an asset marked each quarter at a price anyone can check. A reader may ask what separates support with no clock from a discount with no date. The filings use neither word, and the piece prices the difference at the scale the filings can see: a discount broad enough to matter would have shown in the margin, and the margin held at 75 percent, in the quarter of the placement and in the quarter after it, each figure from filed statements. (9) A discount narrow enough to sit beneath a company-wide margin’s resolution is exactly what the equity’s form makes unnecessary.

The form also prices NVIDIA’s two kinds of dollar against each other. A revenue dollar leaves 65.6 cents of operating income by the quarter’s own statement, on 45-day paper. (1) An investment dollar carries no coupon and no maturity, returns a mark, and NVIDIA’s adjusted measures exclude the marks, sixteen billion dollars of them in the quarter just filed. The exclusion is a statement of relative worth in the filer’s own hand: revenue dollars enter every measure NVIDIA publishes; mark dollars enter only the compulsory ones. The placement spent the currency NVIDIA sets aside to defend the currency it is measured on.

The placement spent the currency NVIDIA sets aside to defend the currency it is measured on.

Market price is market price, and the concession is made in full: a seller prices where the demand side will pay, and this demand side wrote the seller into its contracts. What the filings add to the concession is participation. NVIDIA’s money stands in the financing that met its price, by purchase agreement and by order form, each used once, each filing when used; the terms its receivable carries are where a third instrument would print, and none has. Whether either is used again, or the third appears, is not a forecast this piece makes. It is a line the next filings print on their own.

The rake, and who is paid before the hand

The three houses’ rakes are all paper until events, each waiting in the box its holder chose. In the language of the table those are secondary rakes, a named cut of the winnings, paid if the game ends with winnings to cut. Each depends on the asset class making good. The fourth house rakes the ante. The house prices the seat: the cost of sitting at this table is the machines, the margin is the rake’s take, and the register collects it in days, against players who recover in years, where they recover at all. In January the house placed a stake as well, and the stake is a secondary rake held on the terms the other three hold theirs: a cut that pays at the end, if the end pays. What separates the fourth house’s cut from the others is the sequence the last section priced. The ante was collected first, the stake crossed back to the player afterward, and the stake stands at a fraction of what the ante had already banked. The ante, not the stake, sets this house apart: it is the only take at this table collected whether or not there is ever a pot, and the only one already in the bank. This series has noted once before that the dealers who arranged CoreWeave’s two rated hands keep a ledger of their own; that ledger is still a later piece. This one stops at the house that stands on all four sides and was paid first.

The seat pricing runs in both directions, and June filed the other one. NVIDIA went to the market its customers use: $25 billion of senior unsecured notes, seven tranches reaching 2056, at yields from 4.27 to 5.63 percent, 20 to 65 basis points over Treasuries, with a use of proceeds one line long: general corporate purposes, including the repayment and refinancing of outstanding notes. (10) The notes outstanding total about $8.5 billion, so the named purpose bounds a third of the raise; the filings do not itemize the rest. This series priced that season’s seats when it priced the operator’s. Inside six months, the same $25 billion cost one issuer a covenant on its own future borrowing, cost another a pledged cash floor with a quarterly test, and cost the fourth house nothing pledged at all. Four issuers drew the same number, and the market wrote four different indentures. The fifth participant at this table never drew it and could not: CoreWeave’s entire debt stack, $25.1 billion of principal, sits within a rounding of the number, 59 percent of it at effective rates of 10 percent or higher, none of it reaching past 2032, assembled raise by raise against machines on a six-year schedule. (5) Each of the four drew in one stroke what the fifth owes in total. None of that stack is filed as the seller’s: the proxy’s related-party pages carry equity, order forms, and purchases, with no debt instrument among them. The lenders hold the years, and the seller holds the days and the upside. The fourth house’s row completes the table: a $58 billion quarterly profit beside a $25 billion raise, nothing pledged, from the same market that funds its customers’ next machines.

Reading the register’s print

NVIDIA reports first. Its fiscal quarter closes in late July and, on the cadence of its prior filings, prints in late August, within days of CoreWeave’s own second-quarter report. (7) August grades both sides of the counter, and the two prints answer different halves of the same question.

From CoreWeave, the watch list is inherited from the last piece: the ratio of EBITDA to in-service equipment, the direction the reclassified customer liabilities take, and the rate on any raise that follows. The chain above rereads that rate as NVIDIA’s own line: the durability of the order book, quoted daily in the customers’ cost of debt. One line joins the list from this piece: in the quarter of the placement, NVIDIA’s $1,985 million was the largest of the three lines that closed the gap between CoreWeave’s purchases and its operating cash flow, and whether any next gap closes with NVIDIA’s money again is a line that files itself. (5)

From NVIDIA, the print is read with this series’ oldest instrument, the quality of cash, and five lines carry it.

The receivable. Three unnamed customers hold 64 percent of a $40.7 billion balance; the balance stands at about 45 days of the quarter’s sales, and the $4 million allowance prices the worry at about one basis point. (6) The baselines to watch: whether 45 days lengthens, whether the concentration shifts, whether one basis point moves. The mirror is already filed on a buyer’s ledger, where vendor payables supplied $960 million of CoreWeave’s first-quarter cash; a receivable that lengthens at the register is the same days, booked as a source, somewhere else.

The portfolio. The full position is filed: publicly held equity at $39.1 billion of fair value, non-marketable positions at $42.3 billion after $17.9 billion of net additions in the quarter, $1.0 billion in equity-method funds, and $27 billion more committed for the fiscal year. (9) The whole stands near $82 billion, roughly one and a half quarters of net income; each addition is money moving from NVIDIA back into the system that buys from it, and the cadence of additions is the circuit’s pulse. One mark is computable in advance, to the dollar: 22,935,780 CoreWeave shares, at each quarter’s closing price. The baseline: marks on public positions ran 23 cents of every dollar of net income last quarter, a floor. And the two marks the filer names, $13.4 billion on public positions and $2.6 billion on stakes that have no ticker, sum past the entire $15.9 billion other-income line even at the boundaries of their rounding; everything else in the line netted below zero, and interest sits in its own captions. (1)(9) How much income arrives as marks, and how much at the counter, are two lines the same page separates.

The categories. Between the annual report filed in February and the quarterly report filed in May, one word left NVIDIA’s taxonomy. The indirect-customer sentence is otherwise unchanged: “CSPs, Neocloud builders, AI model makers, enterprises, and public sector entities” became “CSPs, AI Clouds, AI model makers, enterprises, and public sector entities.” The quarterly report adds that revenue by market platform “and the comparable periods have been recast.” (8) A named class of buyer became part of a wider one, retroactively, in a single filing. The dependence on the category is unchanged; the category has been redefined, and what the taxonomy no longer separates, only the customer-concentration disclosures still can.

The margin. Seventy-one for the year, seventy-five for the quarter. The margin is NVIDIA’s price holding: the number the demand side takes as given, and the first place any change in demand would show.

The placements, from CoreWeave’s side: each sale of its equity files its price and its buyer. NVIDIA’s January purchase is the one this piece prices; any next one prints its own comparison, and CoreWeave’s next proxy extends the order-form series.

The fourth house was paid in days, at a margin it files, before the grading of years began. When its print arrives in August, the questions are the series’ oldest ones, asked of the strongest hand at the table: how much of the quarter’s income arrived as cash from customers, how much arrived as marks on the customers’ shares, and how much of the customers’ cash began the quarter as NVIDIA’s own?

DISCLOSURE, standing: Anthropic is the developer of Claude, which is used in preparing this research. CoreWeave announced a multi-year agreement with Anthropic in April 2026; Amazon and Alphabet, named in prior pieces in this series, hold large positions in Anthropic; NVIDIA supplies the infrastructure providers that serve Anthropic. Figures are quoted from the filers without characterization, and the same standard of reading is applied to every filer named.

Figures are verified against the primary filings; documents are cited by accession number. Analysis: Cape Fear Advisors.

Cape Fear Advisors holds no position in any security named in this analysis and has received no compensation from any company discussed.

This analysis also appears on Substack.

Notes

(1) NVIDIA Corporation: Form 10-K for the fiscal year ended January 25, 2026, accession 0001045810-26-000021: revenue $215.9 billion, cost of revenue $62.5 billion, gross profit $153.5 billion (71.1%). Form 10-Q for the quarter ended April 26, 2026, accession 0001045810-26-000052: revenue $81.6 billion, gross profit $61.2 billion (75.0%); unrealized gains on publicly held equity positions of approximately $13.4 billion within $15.9 billion of other income; net income $58.3 billion. The investment portfolio and its placement were read in “NVIDIA, Adding It Up: The Quality of Cash” in this series. Other income (expense), net of $15,929 million and net income of $58,321 million per the Q1 FY2027 results; the CFO commentary attributes the swing to “unrealized gains in publicly-held and non-marketable equity securities,” and the company’s non-GAAP measures “exclude acquisition-related and other costs, other, gains/losses from equity securities, net, certain other income and expense” (Form 8-K furnished May 20, 2026, accession 0001045810-26-000051, press release and CFO commentary; furnished, not filed, and labeled accordingly). The Q1 FY2027 10-Q’s MD&A states operating income at 65.6% of revenue in its percentage-of-revenue table, and its segment discussion attributes the Data Center increase to growth “driven by the ramp of our Blackwell systems.” The income statement reports interest income of $540 million and interest expense of $102 million in their own captions, outside other income (expense), net, of $15,929 million; total other income, net, of $16,367 million sums the three. The two named unrealized-gain figures, $13.4 billion on publicly-held positions and $2,603 million on non-marketable positions, sum to between $15,953 million and $16,052 million at the boundaries of the publicly-held figure’s rounding, above the $15,929 million line at every point of the band; the remainder of the line therefore netted between $(24) million and $(123) million.

(2) CoreWeave, Inc. FY2025 Form 10-K, accession 0001769628-26-000104: “as a result of our obligations in our current customer contracts, all of the GPUs used in our infrastructure today are NVIDIA GPUs,” and “our current customers have contractually specified our use of NVIDIA GPUs.” From the same filing’s risk factors: “Part of this process entails cycling out older components of our infrastructure and replacing them with the latest technology available,” as quoted in “CoreWeave, Twenty-Seven Years” in this series.

(3) CoreWeave, Inc. Definitive Proxy Statement, filed April 22, 2026, accession 0001769628-26-000191, “NVIDIA Related Party Transactions”: the Master Services Agreement dated April 2023 and the order-form language verbatim; payments from NVIDIA of approximately $326.3 million (fiscal 2025) and $59.6 million (three months ended March 31, 2026); NVIDIA at 17% of total purchases from suppliers for fiscal 2025; the Securities Purchase Agreement of January 23, 2026, 22,935,780 Class A shares at $87.20 per share, $2 billion aggregate. The subsequent-events confirmation is the FY2025 10-K, Note 16. The net figure is the Q1 2026 Form 10-Q, accession 0001769628-26-000222, financing activities: common stock private placement, net of issuance costs, $1,985 million. NVIDIA is absent from the financial-statement related-party note (ASC 850 turns on voting influence and principal ownership) and present in the proxy (Item 404 turns on 5% beneficial ownership); the difference is definitional, and both documents are cited here.

(4) “CoreWeave, Twenty-Seven Years” (July 12, 2026) in this series, note 5: the full grid of constructions from the Q1 2026 Form 10-Q, accession 0001769628-26-000222, and the FY2025 Form 10-K. Six-year pre-financing return per dollar of machines: 77 cents as reported, 89 with stock compensation added back, 99 at the most favorable corner.

(5) Same sources: in-service gross equipment $31,352 million at March 31, 2026; total principal $25,149 million with 59% at effective rates of 10% or higher; revenue $2,078 million and operating loss $(144) million for the quarter ended March 31, 2026; financing detail per that piece’s notes 1 and 3. The first-quarter funding gap: purchases of property and equipment $7,695 million against operating cash flow of $2,984 million, a gap of $4,711 million, closed to within the statement’s smaller items by net new debt of $1,955 million, an $810 million draw on the company’s own cash, and the private placement, $1,985 million net, the largest of the three; gross property and equipment grew from $33,941 million to $40,933 million in the quarter. The placement carries no coupon and no maturity; the debt’s rates are the principal figures above.

(6) NVIDIA Form 10-Q for the quarter ended April 26, 2026, accession 0001045810-26-000052: accounts receivable $40.7 billion; three customers representing 64% of the balance; allowance for doubtful accounts $4 million; as read in “NVIDIA, Adding It Up: The Quality of Cash.” The receivable stands at approximately 45 days of quarterly sales: $40.7 billion against $81.6 billion of revenue in a 91-day quarter. The $4 million allowance is approximately one basis point of the balance.

(7) NVIDIA’s fiscal second quarter ends in late July; the prior-year second quarter was reported in late August, per the Form 8-K furnishing those results. CoreWeave’s second-quarter timing runs on its own prior cadence, per note 15 of “CoreWeave, Twenty-Seven Years” (July 12, 2026). Neither company had announced a reporting date as of this writing; both cadences are the filed record of prior years.

(8) The taxonomy comparison, verbatim: Form 10-K, accession 0001045810-26-000021: “indirect customers include CSPs, Neocloud builders, AI model makers, enterprises, and public sector entities.” Form 10-Q, accession 0001045810-26-000052: “indirect customers include CSPs, AI Clouds, AI model makers, enterprises, and public sector entities”; same filing: revenue by market platform “and the comparable periods have been recast,” and the hyperscaler and diversification sentences as quoted.

(9) NVIDIA Form 10-Q, accession 0001045810-26-000052, fair value and non-marketable securities notes: publicly-held equity securities at fair value of $39.1 billion at April 26, 2026 ($21.0 billion reported in marketable equity securities, $8.9 billion in other assets under lock-up through December 2027, and $9.2 billion of Level 2 warrants and preferred stock convertible to common stock in public companies), of which $27.4 billion is subject to short-term lock-up restrictions; non-marketable equity securities carried at $42.3 billion, on the filing’s own walk: balance at beginning of period $22,251 million, plus net additions of $17,899 million, plus unrealized gains of $2,603 million (recognized, per the filing’s footnote, in other income (expense), net), less reclassifications of $389 million (primarily to marketable securities following public market trading), less impairments and unrealized losses of $28 million, equals $42,336 million; equity-method investments of $1.0 billion in infrastructure funds, with maximum loss exposure including committed amounts of $2.3 billion; total investment commitments of $27 billion, subject to certain contingencies, expected to be made through the remainder of fiscal year 2027; net unrealized gains on publicly-held equity securities held at period end of $13.4 billion for the quarter. The $82 billion total is the sum of the publicly-held fair value, the non-marketable carrying value, and the equity-method balance; it excludes the $27 billion of commitments. The margin held across the placement, quarter against quarter: fiscal 2026 revenue of $215,938 million and gross profit of $153,463 million (Form 10-K, accession 0001045810-26-000021) less nine-month revenue of $147,811 million and gross profit of $102,370 million (Form 10-Q for the quarter ended October 26, 2025, accession 0001045810-25-000230) give fourth-quarter revenue of $68,127 million and gross profit of $51,093 million, a 75.0% margin for the quarter ended January 25, 2026, the quarter containing the January 23 placement; the quarter ended April 26, 2026 filed 75.0%.

(10) NVIDIA senior unsecured notes, June 2026: pricing term sheet (free writing prospectus) filed June 15, 2026, accession 0001193125-26-271326, and prospectus supplement, accession 0001193125-26-273139, registration statement 333-287619: $25,000,000,000 across seven tranches ($3.5 billion of 4.250% notes due 2028; $3.5 billion of 4.350% notes due 2029; $4.0 billion of 4.500% notes due 2031; $3.5 billion of 4.750% notes due 2033; $4.0 billion of 4.950% notes due 2036; $3.0 billion of 5.550% notes due 2046; $3.5 billion of 5.625% notes due 2056); yields to maturity 4.273% to 5.628%; spreads of 20 to 65 basis points over benchmark Treasuries; net proceeds before expenses $24,916,780,000; settled June 18, 2026 (closing Form 8-K, accession 0001193125-26-275783). Use of proceeds, per the prospectus supplement: “general corporate purposes, including the repayment and refinancing of outstanding notes.” Long-term debt outstanding at April 26, 2026: $8,470 million (Form 10-Q, accession 0001045810-26-000052). The cohort comparison is “The Price of the Seat” (this series): Oracle’s $25 billion (February 2026) carried a covenant limiting further issuance; SpaceX’s $25 billion (June 2026) carried a pledged minimum cash position and a quarterly leverage covenant; Amazon’s $25 billion priced July 8, 2026; the operator’s unsecured notes bear 9.625% due July 2032.