The banks that placed this quarter’s paper have already printed the quarter. The companies whose paper it was have not. Nothing below is hidden; every figure is disclosed to the penny, most of them on cover pages. Read together, they are roughly a billion dollars of friction, collected at settlement, ahead of the first coupon, lifted while the money moved.

Three numbers sit on the cover of SpaceX’s June prospectus: $135.00, $0.90, and $134.10 (1). The first is what the public paid for a share. The last is what SpaceX received. The number in the middle is the underwriting discount, and it never traveled anywhere. No invoice was issued, no wire was sent. The buyers paid $135.00, the seller collected $134.10, and the ninety cents stayed with the banks that ran the sale. Across 555,555,555 shares, ninety cents is $500 million.

That is a croupier’s arithmetic: the take is lifted while the money is in motion, so the money never has to change hands at all. The filings print the mechanics in three stacked rows on page one: price to public, underwriting discounts, proceeds before expenses. The third row is the first row minus the second. Everything in this piece lives in the middle row.

The middle row, six times

Six registered offerings this year printed that row in full, and mostly the same banks ran the books.

NVIDIA sold $25.0 billion of notes in June across seven maturities, 2028 to 2056. The filed discount runs from 0.080% on the two-year notes to 0.400% on the thirty-year notes, and the cover prints each tranche’s discount in dollars; the seven filed rows sum to $47,350,000, or 18.9 basis points of the money moved (2). The representatives were Goldman Sachs, J.P. Morgan, and Morgan Stanley, and Goldman holds the largest allocation in every tranche of the filed table.

Oracle sold $25.0 billion in February: $75.0 million, 30.0 basis points (3). Broadcom sold $4.5 billion in January: $15.25 million, 33.9 basis points (4). Amazon sold $25.0 billion on July 8: a filed total of $56.1 million, 22.4 basis points (5). Alphabet sold $20.0 billion of dollar notes in February for $72.0 million, 36.0 basis points, and £5.5 billion of sterling notes the next day for £22.5 million (6). In June, Alphabet sold $18.0 billion of its own stock; the filed discount was $175.2 million, 97.3 basis points (13).

And SpaceX’s initial public offering raised $75.0 billion at the $500 million on its cover, 66.7 basis points. The option to sell $11.25 billion more carries a filed commission of zero. The same document notes the regulatory ceiling on underwriting compensation: five percent of gross proceeds. The filed rate is two thirds of one percent.

The rows line up like a rate card, and the card orders by the paper more than by the name. NVIDIA paid 18.9 basis points per dollar placed, Amazon 22.4, Oracle 30.0, Broadcom 33.9, Alphabet 36.0 in dollars. Alphabet is among the strongest credits on this page and sits at the bottom of the card; Oracle, which a July piece in this series found at the last notch of investment grade, paid six basis points less. What separates them is not the name. Alphabet’s curve runs decades longer, and the cost of years is the next section.

The card also holds an inversion worth a sentence. The type of deal that is priced as the expensive one came in below the routine one: the largest initial public offering on record cost 66.7 basis points per dollar, while a seasoned issuer’s stock sale the same month cost 97.3. At $75 billion, the filed rate followed the deal’s size rather than its type. That is a reading, not any filing’s sentence; the two rates are both filed.

One line against one quarter

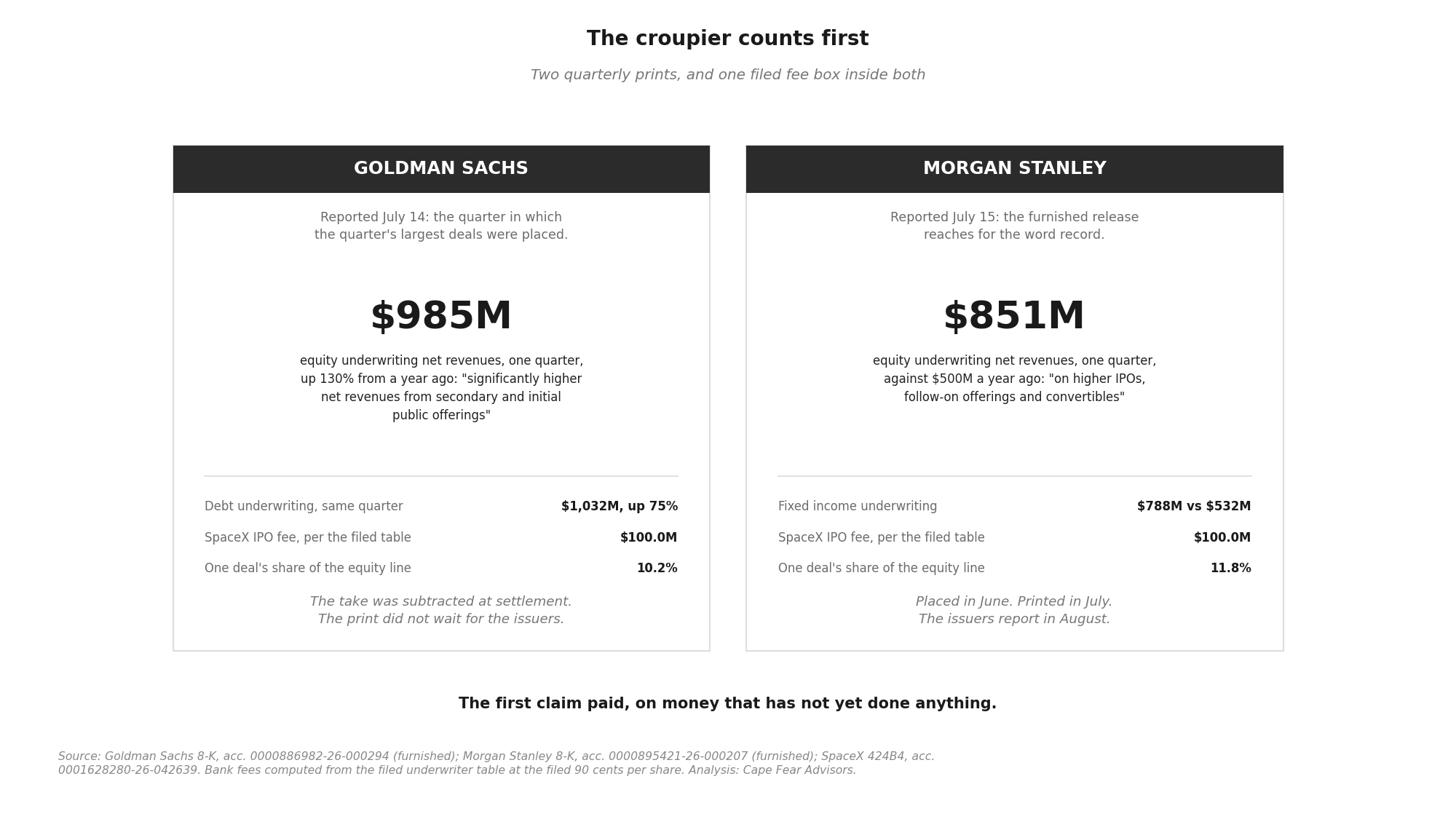

Goldman Sachs reported its second quarter on July 14: revenue 39% higher than a year ago, earnings of $20.98 per share (7). One line inside the report reads equity underwriting, $985 million, up 130% from a year ago. The furnished explanation: “significantly higher net revenues from secondary and initial public offerings.”

The SpaceX cover splits its $500 million by name. Goldman’s 111,111,111 shares, at the filed ninety cents, is $100.0 million. One deal is 10.2% of that line.

Morgan Stanley reported the next morning, and its furnished release reaches for the word record for the firm, for pre-tax income, and for the division that did the placing. Equity underwriting: $851 million against $500 million a year ago, “on higher IPOs, follow-on offerings and convertibles” (8). Its SpaceX allocation matches Goldman’s, so the same $100.0 million is 11.8% of its line. The debt lines moved the same direction: Goldman’s debt underwriting up 75%, Morgan Stanley’s fixed income underwriting up 48%.

The calendar deserves its own care here. Of the tables quoted in this piece, Broadcom’s, Oracle’s, and Alphabet’s February rows belong to the banks’ first quarter; SpaceX’s, NVIDIA’s, and Alphabet’s May and June rows to the second; Amazon’s July row to the third. Every comparison in this section stays inside the second quarter, where the deal and the line share a calendar.

The placements closed in June. The banks reported in July. NVIDIA reports the quarter of its raise in late August. SpaceX’s first quarterly report as a public company is expected in mid-August. CoreWeave has not named a date. The banks’ compensation did not need to wait for any of that, because it was subtracted before the proceeds arrived. The first claim paid, on money that has not yet done anything.

What the years cost to place

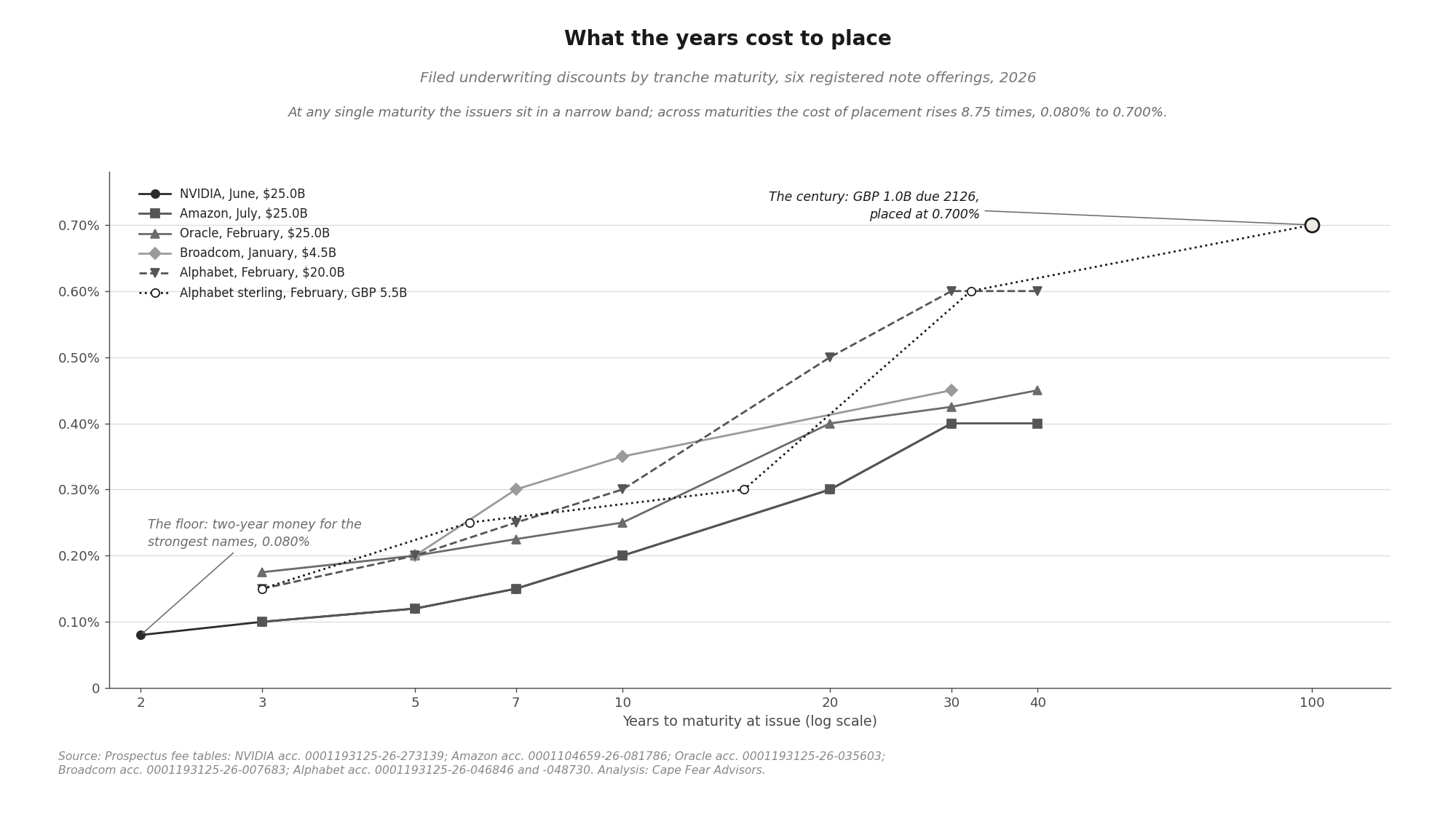

Inside every discount table, one gradient repeats: the longer the money, the more it costs to place. The exhibit above plots every filed tranche discount against its years to maturity, and it carries the prior section’s finding on its face: at any single maturity the issuers sit in a narrow band, while across maturities the cost of placement rises 8.75 times, from 0.080% to 0.700%.

NVIDIA’s 2028 notes cost 8 basis points; its 2056 notes cost 40. Amazon runs 10 to 40. Oracle runs 17.5 to 45 on a curve that reaches 2066. Alphabet’s dollar curve runs 15 to 60. At the far end of everything sits a tranche from Alphabet’s February sterling deal: £1.0 billion of 6.125% notes due 2126, one hundred years out, at a filed discount of 0.700% (6). Placing two-year money for the strongest names costs 8 basis points. Placing hundred-year money costs 70. An earlier piece in this series found that the price of the seat is in the tenor. The price of placing the seat is in the tenor too, and it is filed to the decimal.

Where the middle row does not exist

Everything above comes from registered offerings, where the discount prints on the cover. The same months moved at least as much paper through private placements, where it does not, and the difference is the rulebook, not anyone’s choice. A sale under Rule 144A to qualified institutional buyers carries no public fee table, because the rule does not require one; each disclosure below is exactly what the regulations ask of its path.

SpaceX followed its IPO with $25.0 billion of senior notes in late June, sold under Rule 144A to institutional buyers (9). The closing filing names BofA, Citigroup, Goldman Sachs, J.P. Morgan, and Morgan Stanley as representatives of the initial purchasers. What no SpaceX filing contains is their compensation. The names are filed; the fee is not. There is a clock on this: SpaceX agreed to a registered exchange offer that will eventually move the notes into the filed record. The one company in this ledger whose clock has already run is Broadcom, which filed exchange offers in June 2026 for notes it sold privately in September 2021 and April 2022 (10). More than four years, in the one case the record allows a measurement.

CoreWeave’s June notes sit entirely outside the fee record, and its filings follow the same rulebook. The $1.25 billion and €2.0 billion of 9.625% and 8.500% senior notes closed June 18 under Rule 144A, and the filing names no bank in any selling capacity: no initial purchaser, no representative, no registration rights, only the trustee and its agents (11). The highest coupons in this ledger belong to the one placement whose filed record shows neither who sold it nor what the selling cost, and nothing required it to show either. CoreWeave’s secured borrowing reads differently because credit agreements attach as exhibits: MUFG and Morgan Stanley lead both facilities, with Goldman Sachs and JPMorgan Chase among the arrangers (12). The fee letters those agreements reference stay private, as fee letters do. Press coverage says J.P. Morgan led the June notes; the reader can weigh reporting as reporting.

What the record will eventually show has a shape, and it is a netting rather than a name. CoreWeave’s balance sheet already carries the aggregate: total debt principal of $25,149 million at March 31, less $290 million of unamortized discount and issuance costs (11). The August report will grow that line by roughly what the quarter’s raises cost to sell, the June notes and the May facility together, banks and lawyers and printers unseparated, less the quarter’s amortization running the other way. Because the notes carry no registration rights, that aggregate is as much light as the paper’s own terms ever call for; no future filing has to name who placed them.

Two names paid nothing at all, for opposite reasons. Berkshire Hathaway put $10 billion into Alphabet through a private placement disclosed in Alphabet’s own pricing release; a direct sale has no underwriter, so no discount exists (13). Microsoft, the strongest credit in this ledger by the agencies’ published grades, filed no offering documents in 2026. One paid nothing because its buyer needed no intermediary. One paid nothing because it did not borrow.

A billion dollars of friction

None of this is hidden. That deserves saying plainly, because this series usually works where disclosure thins out, and here disclosure is total: every registered discount is printed to the penny, tranche by tranche, on the first page of a public document. What the disclosure describes is friction.

The banks’ side of the middle row also deserves stating at full strength, because real work and real exposure sit behind it. In a firm-commitment offering, the underwriters buy the paper themselves: between pricing and settlement they own it, they bear the price risk if the market moves against them, they stabilize the aftermarket, and they carry statutory liability under the Securities Act for the registration statement they sign onto, a liability whose defense is the diligence they perform. The work shows up in the filed record itself: SpaceX’s docket carries seven free writing prospectuses across eight days of early June, including interview transcripts and country-specific materials for the United Kingdom, European, and Japanese legs of the sale (1). Their names print on the cover directly beneath the issuer’s, and the cover is where a failed deal would carry them. The discount pays for the insurance, the distribution, and the name; it is negotiated by the most sophisticated issuers alive; and by the regulator’s own yardstick it is set low, two thirds of one percent on the SpaceX cover against a ceiling of five. The friction in this piece is finely priced, and it is still friction. The premium survives undiminished at the exact end of the table where the insured risk is smallest: eight basis points to hold two-year paper for one of the strongest names on this page, for the few days between pricing and settlement.

The dollar tables quoted here sum to $884.8 million across six deals. Amazon’s July table brings the running figure to $940.9 million. The sterling table adds £22.5 million, and three more currencies of Alphabet notes, two series of Alphabet convertible preferred, and a filed commission of up to 0.5% on a $40 billion at-the-market program are still uncounted. The registered record alone shows roughly a billion dollars in six months, paid by six issuers to a rotating cast of the same five or six banks, for the act of placement.

A basis point reads like dust, and the tables are denominated to feel that way. The restoration is one multiplication: on a $25 billion deal, a basis point is $2.5 million. NVIDIA’s 18.9 quiet basis points are $47.35 million, roughly what it separately budgeted for every other cost of the offering combined, the lawyers and accountants and printers together.

The friction also stays in the paper after the cash is gone. NVIDIA’s cover prints all three columns to the dollar, tranche by tranche; summed, they read $24,964,130,000 paid by the public, $47,350,000 of discounts, $24,916,780,000 of proceeds before expenses, against $25.0 billion of principal to be repaid at maturity (2). The wedge between principal and proceeds is $83.22 million, and the cover splits it: $35.87 million is the market’s pricing of the notes, and $47.35 million is placement. The company will repay, at maturity, money it never received. Every discount in this piece has that shape: out of the system as cash on day one, still in the system as principal for two years, or thirty, or one hundred.

The company will repay, at maturity, money it never received. Every discount in this piece has that shape: out of the system as cash on day one, still in the system as principal for two years, or thirty, or one hundred.

And it stands first in line. Before any of these companies earns back the price of its machines, and before it earns the interest and dividends that are the price of its money, its output must cover the cost of having been handed the money at all. Twenty-seven years of machine life, an earlier piece calculated, to pay for the machines and the money that bought them. The placement was paid before that clock started.

One more grading, in this series’ own currency. The Quality of Cash shelf ranks dollars by what must still happen for them to become real: NVIDIA’s receivable needs about 45 days and a solvent buyer, CoreWeave’s machines need years of earning, a mark needs a price to hold. The middle row’s dollar needs nothing further. It was collected at settlement rather than billed, it owes no future performance, and once settled it is indifferent to whether the paper that produced it performs at all. By the shelf’s measure it may be the highest-quality dollar this series has graded. Two bounds sit on the grade. The dollar renews only with the flow: both banks’ own prior-year comparators show how far the line sits below itself when the window narrows. And the same institutions sit on the lender side of the same names’ borrowing, where the exposure this fee avoids lives on: MUFG and Morgan Stanley are the named arrangers and agents of CoreWeave’s credit agreements, whose lender schedules the filed exhibits reference without reproducing. Even here, who holds the risk is referenced rather than filed. The fee dollar is pristine; the franchise around it is not unexposed.

Reading the next prints

Amazon’s $56.1 million priced on July 8, three days into the banks’ third quarter, so the next prints already hold their first entry. SpaceX’s exchange offer will someday put a registered document around $25 billion of notes, and Broadcom’s more than four years suggest the wait is measured in years. CoreWeave’s issuance-cost netting will grow in August by roughly what the quarter cost to place. Both banks described their backlogs in July as higher.

The billion is disclosed, collected, and closed. The output that must repay it has not been reported by anyone yet. Three claims now stand in line ahead of the first dollar these placements produce: the placing, the money, the machines. The first claim has been paid in full, part of it to parties no filing is required to name. Which filing, and in which August, shows the first dollar arriving?

Three claims now stand in line ahead of the first dollar these placements produce: the placing, the money, the machines. The first claim has been paid in full, part of it to parties no filing is required to name.

DISCLOSURE, standing: Anthropic is the developer of Claude, which is used in preparing this research. CoreWeave announced a multi-year agreement with Anthropic in April 2026; Amazon and Alphabet, named in this piece, hold large positions in Anthropic; and NVIDIA supplies the infrastructure providers that serve Anthropic. Figures above are quoted from the filers without characterization, and the same standard of reading is applied to every filer named.

Figures are verified against the primary filings; documents are cited by accession number. Analysis: Cape Fear Advisors.

Cape Fear Advisors holds no position in any security named in this analysis and has received no compensation from any company discussed.

This analysis also appears on Substack.

Notes

(1) SpaceX Form 424B4, filed June 12, 2026, accession 0001628280-26-042639. Cover page fee box and underwriting section, including the underwriter table and the over-allotment footnote. Roadshow record: free writing prospectuses of June 4 through June 11, 2026, accessions 0001628280-26-040610, -040874, -041013, -041150, -041365, -041761, and -042466.

(2) NVIDIA prospectus supplement, Form 424B5, June 17, 2026, accession 0001193125-26-273139. Cover fee box prints per-tranche dollar rows for price to public, underwriting discounts, and proceeds before expenses; the sums across the seven filed rows are $24,964,130,000, $47,350,000, and $24,916,780,000. Discount ladder and underwriter table from the underwriting section.

(3) Oracle Form 424B2, accession 0001193125-26-035603. Total computed from filed rates and filed tranche sizes.

(4) Broadcom Form 424B2, January 8, 2026, accession 0001193125-26-007683. Per-tranche discounts and totals as filed.

(5) Amazon Form 424B5, July 8, 2026, accession 0001104659-26-081786. Fee table totals as filed.

(6) Alphabet Forms 424B2, February 11 and February 12, 2026, accessions 0001193125-26-046846 and 0001193125-26-048730. Dollar and sterling fee tables as filed, including the 2126 tranche.

(7) Goldman Sachs Form 8-K, July 14, 2026, accession 0000886982-26-000294. Furnished under Item 2.02. Segment revenue lines and quoted language from the furnished release.

(8) Morgan Stanley Form 8-K, July 15, 2026, accession 0000895421-26-000207. Furnished under Item 2.02. Segment revenue lines and quoted language from the furnished release.

(9) SpaceX Forms 8-K of June 23 and June 26, 2026, accessions 0001628280-26-044955 and 0001628280-26-045763. Tranche schedule, Rule 144A language, and the registration rights agreement naming the initial purchasers’ representatives.

(10) Broadcom Forms 424B3, June 17, 2026, accessions 0001193125-26-274187 and 0001193125-26-274169. Exchange offers for notes issued September 30, 2021 and April 14, 2022.

(11) CoreWeave Form 8-K, June 18, 2026, accession 0001769628-26-000291. The debt-footnote netting: CoreWeave Form 10-Q for the quarter ended March 31, 2026, accession 0001769628-26-000222, total principal of debt $25,149 million less unamortized discount and issuance costs of $290 million.

(12) CoreWeave Forms 8-K, March 31 and May 18, 2026, accessions 0001769628-26-000129 and 0001769628-26-000236, and the credit agreements filed as exhibits thereto.

(13) Alphabet free writing prospectus, June 3, 2026, accession 0001193125-26-254490, and Forms 424B5 of June 2 and June 4, 2026, accessions 0001193125-26-252439, 0001193125-26-257702, 0001193125-26-257690, and 0001193125-26-256375. Common stock fee box as filed; ATM commission cap as filed; the private placement as described in Alphabet’s pricing release.

(14) Pieces in this series relied on above, cited directly: “The Price of the Seat” (July 9, 2026), for the tenor finding and the Oracle rating report it carries; “CoreWeave, Twenty-Seven Years” (July 12, 2026), for the machine-life arithmetic; “NVIDIA, The Fourth House” (July 14, 2026), for the receivable and the treatment of marks; and the Quality of Cash shelf, for the grading framework.