Oracle’s fiscal 2026 statements are audited, unqualified, and taken here as they stand. Added up, they record two businesses in one column: a franchise of installed software, and a buildout spending $56 billion on capacity still to be delivered. The column produced $32 billion of operating cash. The difference was raised, with $20 billion to spare, at prices the filing lists to the basis point. This piece sorts the year’s cash by what discharges it, sets the furnished description beside the filed record, and stops where the disclosures stop: at a question the rules leave open, whose only answer on the record is furnished.

Nine days ago, against this same annual report, we set a second test beside the quality of earnings and called it the quality of cash: of a number presented as a present fact, how much is cash, and how certain is the cash still to come. (1) We ran it against the largest figure in the filing, the $638 billion backlog, and stopped there. This piece runs it through the rest of the document, through the cash itself.

Oracle’s statements carry an unqualified opinion from Ernst & Young, its auditor since 2002, and internal control over financial reporting was audited and found effective. (2) We take the statements as they stand and depend on them. They consolidate two very different businesses into one column because consolidation is what the standards require of a single company, and customers appear in aggregate because the aggregate is what the rules permit. What is vague in what follows is vague because the rules allow it to be. The same requirements that produce the one column leave its largest question open.

The numbers the company reports

For the fiscal year ended May 31, 2026: total revenues of $67.4 billion, up 17 percent. Net income of $17.1 billion, which includes the $2.7 billion one-time gain on the Ampere sale we read in June. (3) Net cash provided by operating activities of $32.0 billion, up 54 percent. Cash used for capital expenditures of $55.7 billion, up from $21.2 billion a year earlier, an increase the company attributes primarily to the expansion of its data centers, with the statement that “we expect this upward trend to continue during fiscal 2027 and in the following fiscal years.” (4)

Oracle publishes the difference itself. In its own liquidity discussion, in its own table: operating cash of $31,977 million, capital expenditures of $(55,663) million, free cash flow of $(23,686) million, stated in the same table as negative 139 percent of net income, against negative 3 percent the year before. (5) The company files the figure.

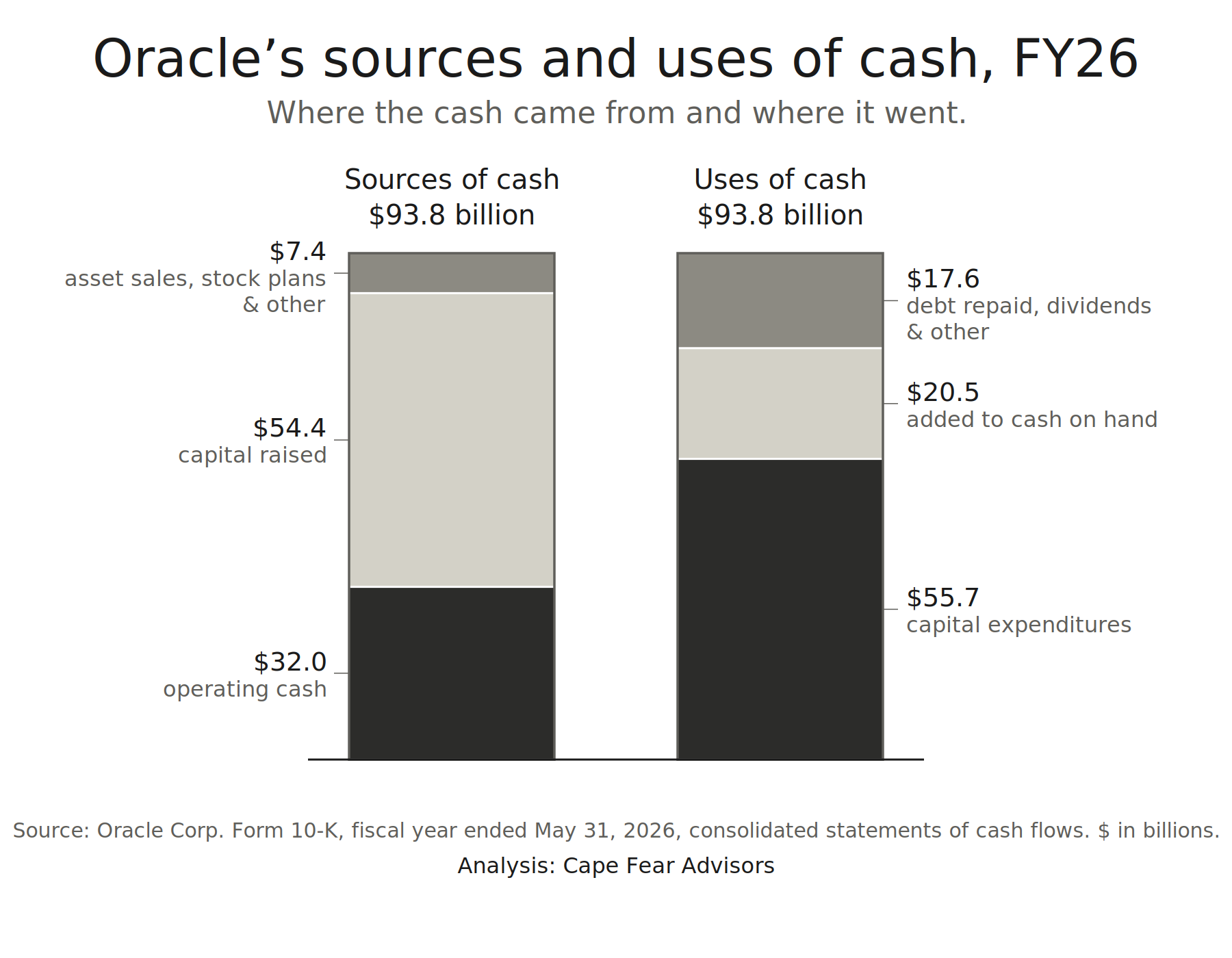

The whole year’s cash, both directions, sorted. Read gross from the statement of cash flows, $93.8 billion came in during fiscal 2026 and $93.8 billion went out, an identity once the addition to cash counts as a use. The sorting is the point. (6) Of the sources: $32.0 billion was operating cash, all of it; $54.4 billion was capital raised; and $7.4 billion came from asset sales, stock plans and other. Of the uses: $55.7 billion was capital expenditures; $17.6 billion was debt repaid, dividends and other; and $20.5 billion was added to cash on hand, which is how a company that produced $32 billion and spent $56 billion on the buildout ends the year with $20 billion more cash than it started with.

Two more figures from the year the income statement carries: restructuring expense of $1.8 billion, against $374 million a year earlier, under a plan sized at up to $2.1 billion whose filed rationale includes “the adoption and integration of AI technologies across certain functions.” (7) And total borrowings of $129.5 billion at year end, up from $92.6 billion. (8)

The annuity and the buildout

The statements present one company, and one column. The disclosures inside it describe two businesses, told apart by the thing this test measures: what discharges the cash. One column, then, with a core: the annuity inside, the buildout rising around it, and no filed line between them.

The first is the older of the two. Software support produced $19.8 billion of revenue in fiscal 2026, $19.5 billion the year before, $19.6 billion the year before that: flat across the three years the filing carries, discharged by the renewal of software already installed and already running. (9) Call it the annuity.

The second is the one the capital is for. Cloud infrastructure revenue grew 77 percent; cloud revenues crossed to 51 percent of the total. Fiscal 2026 is the year the new business became the majority of Oracle by revenue. (10) Its obligations are discharged differently: by delivering capacity the company is still building, in an expansion the filing states will continue, to customers the filings carry in aggregate. (4)

The cash carries no line between them. Even the sentence the MD&A uses to name the source of the money runs the two together: “Our largest source of operating cash flows is cash collections from our customers following the purchase and renewal of their cloud and software support agreements.” (11) Cloud and support, one phrase. The source is named, and the split between the two businesses stays inside it.

The word on the segment line has traveled further than the segment structure. When cloud entered these filings it named an environment; (12) by fiscal 2013 it named a subscription line beside licenses; (13) in fiscal 2026 it carries the majority of revenue and the buildout this piece prices. Each redefinition is filed, the walk deserves its own piece, and it is enough here that the cloud of the current filing is not the cloud of 2013.

The filing also states where today’s dividing lines sit, and why. Oracle reports three businesses: cloud and software, hardware, and services. The annuity and the buildout both live inside the first, so even the filing’s own three-way division stops short of the line this piece is reading for. Its segment disclosures, in the filing’s words, “align to how our chief operating decision makers (CODMs), which are our Chief Executive Officers and Chief Technology Officer, view our operating results and allocate resources.” (14) The segment standard follows management’s own lens: the filing divides where management divides, and carries together what management runs together. The one column is itself a disclosure. Oracle manages the annuity and the buildout as a single business, and files that fact.

The segment note prices the second company’s arrival inside the first. Direct expenses of the combined cloud-and-software segment ran $8.8 billion, then $10.8 billion, then $16.9 billion, up 56 percent in fiscal 2026 against revenue growth of 19 percent, and the segment’s margin moved from 64 to 63 to 59 percent. The margin nets one more line: the segment’s own sales and marketing, $7.2 billion, which fell 3 percent in the year delivery costs rose 56. The buildout is arriving in the cost of delivering, not in the cost of selling. (15) The disaggregation stops where management’s lens stops. Everything this piece measures from here, the blended margin, the aggregated customers, the unallocated capacity, is the rules working as written.

The promise, and who owes it

The naming pattern we read in June holds: the accounting compels a name on an investment and permits an aggregate on a customer, and the filing follows the accounting. (16) Underneath it sits an anchor of Oracle’s own filing, and a search we ran.

On June 30, 2025, Oracle filed a Form 8-K carrying remarks its chief executive would deliver that day: the company had signed multiple large cloud services agreements, “including one that is expected to contribute more than $30 billion in annual revenue starting in FY28.” (17) The filing stated the size and left the name to the aggregate. A year of filings later, the annual report attributes the $500 billion increase in remaining performance obligations to “certain significant cloud contracts that were entered into during the period,” and discloses, accurately, under the test the rules prescribe, which measures revenue and measures the past, that no customer accounted for 10 percent or more of total revenues in fiscal 2026, 2025, or 2024. (18) The past is diversified. The promise is $638 billion, and the promise carries no names.

We went looking for the tie, and here is the record as we found it. The parties themselves have spoken, in their own names: Oracle and OpenAI have jointly announced data-center capacity partnerships under the Stargate program, statements on the record from both sides, carrying the relationship and stopping there. (19) The reporting goes further: a widely carried figure attributes roughly $300 billion of the backlog to that counterparty. We searched for that figure, or any allocation of the backlog to any named customer, in Oracle’s filings and in both parties’ own communications, and it appears in neither; when the question was put to Oracle’s executives directly, after the reports circulated, no further detail entered the record. (20) The size is filed. The relationship is stated. The tie between them exists, on the record, nowhere.

To be plain about what that does and does not mean: the assumption that ties them is widely shared, and it is a reasonable one; the joint announcements are much of why. Nothing here questions it. The point is the category. An attribution can be well-founded and still be an estimate, and the disclosure that would make it more than an estimate has not been made, by anyone. Well-founded is one thing; filed is another. The number lives in the first, and we carry it there.

“Well-founded is one thing; filed is another. The number lives in the first, and we carry it there.”

The asymmetry belongs to the rules. Revenue concentration looks backward, and the rules require it: the 10 percent test is mandatory, and Oracle passes it, disclosed. Backlog composition looks forward, and the rules leave it to the aggregate, so any allocation of the $638 billion is, necessarily, an estimate made outside the filings. One has to be disclosed; the other has to be estimated. The most consequential unknown in the filing’s largest number sits on the estimated side of that line, and the filing, lawfully, leaves it there.

What the filing does state, beside the aggregate, is its own description of who is in it: “In certain OCI offerings, we are more concentrated among a number of large customers, which could increase these risks.” (21) The shape of the exposure is filed; the names stay with the aggregate.

Paid ahead

In June we set the two disclosures of the backlog side by side, the release marking $75 billion of it “prepaid and customer supplied,” the audited statements carrying the figure whole, and read the difference as necessity: what a document must carry, against what a description wants. (22) The annual filing now supplies the audited shadow of that characterization, and it is a new line in the company’s books.

During fiscal 2026, Oracle’s operating cash included $4.6 billion from “customer prepayments with significant financing component”: payments so far ahead of delivery that the accounting treats them, in part, as borrowing, on which Oracle recognizes interest expense. The comparable figure in fiscal 2025 was zero. In fiscal 2024, zero. (23) On the balance sheet, deferred revenues rose from $10.7 billion to $15.4 billion, and the non-current portion, cash collected for delivery beyond a year out, quadrupled from $1.3 billion to $5.5 billion. (24) Customers have always paid Oracle in advance; support runs that way. Fiscal 2026 is the first year the money arrived far enough ahead, at scale enough, for the accounting to classify part of it as borrowing, and the line that carries it is new to the statements.

The furnished layer, in the same quarter, acquired a new instrument. The earnings release introduced a measure called “net cash outlay for capital expenditures,” which is capital expenditures net of short-term financing and net of customer prepayments, a lens that presents the capital spend after the customers’ contributions to it. (25) It is disclosed, defined, and reconciled, as the rules for such measures require. It is also new, and it arrived in the quarter the GAAP table printed free cash flow of negative $23.7 billion. The new measure nets; the filed statement records: $55.7 billion out for the buildout, $4.6 billion in from prepayments that carry a financing component, and the gap. Both are Oracle’s numbers.

The price of the next dollar

The gap was raised, and the filings state what the raising cost, at every rung.

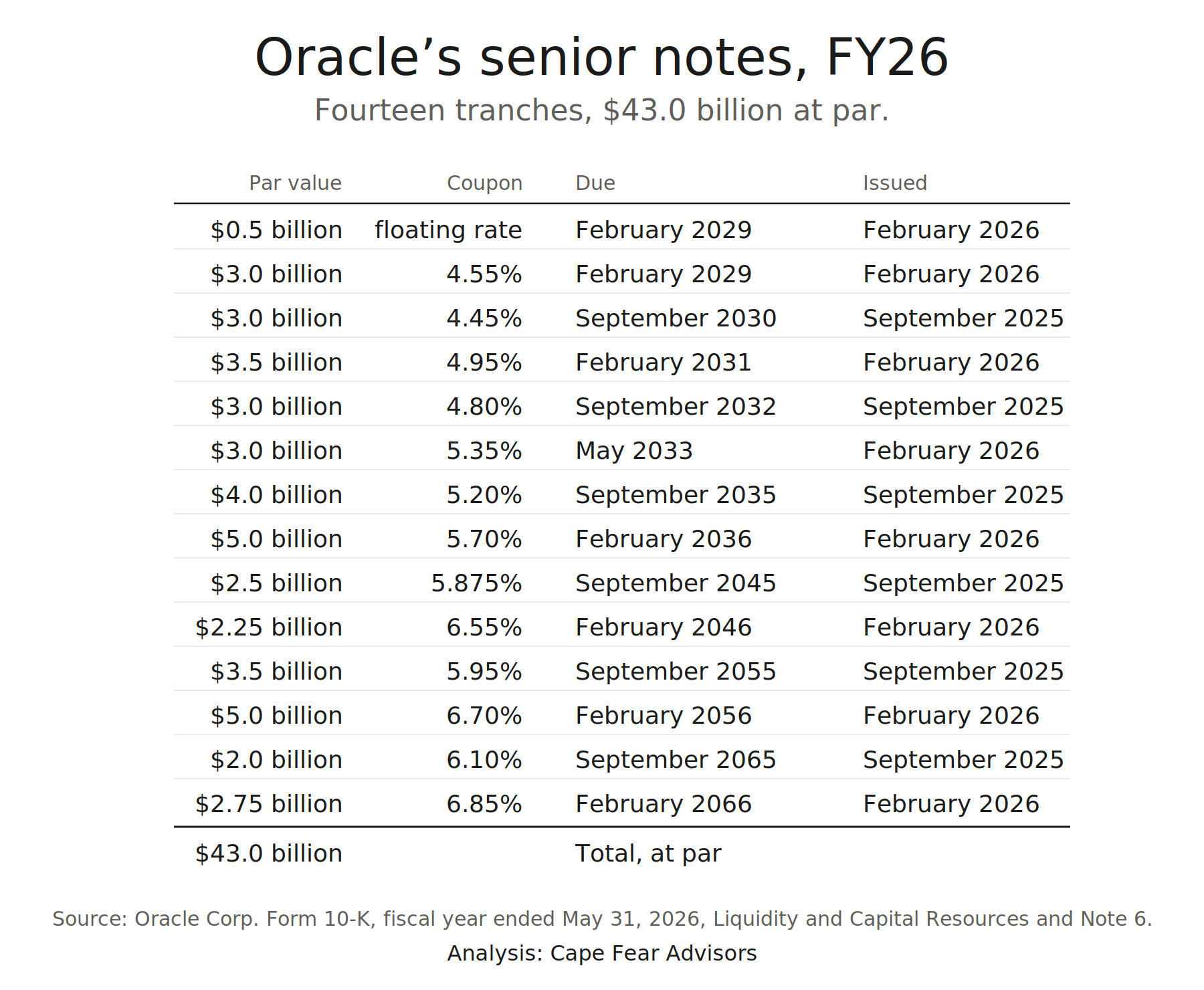

The year’s gross raising was $54.4 billion: $46.1 billion of senior notes, term loans and other borrowings, net of issuance costs, including fourteen senior-note tranches totaling $43.0 billion at par; $5.0 billion of 6.50% Series D Mandatory Convertible Preferred Stock, issued February 5, 2026; and $3.3 billion of short-term financing tied to the capital expenditures themselves. (26) An at-the-market equity program of up to $20 billion was entered on February 2, 2026, and stood unused at year end. (27) The fourth-quarter call added the forward figure: roughly $40 billion of additional financing expected in fiscal 2027, against a net cash outlay for capital expenditures of roughly $70 billion, excluding $20 to $25 billion of expected customer prepayments. (28)

The fourteen senior-note tranches, as the filing lists them: (29)

The maturities run to 2066. Oracle borrowed money for forty years, February 2026 to February 2066, both dates in the debt footnote, in a document whose risk factors state that committed hardware purchases carry “increased excess and obsolescence risk” the company “expect[s]… will continue,” that component lives “may differ from our expectations,” and that data-center lease terms “typically do not align with the duration and pricing of customer contracts.” (30) The instruments and the sentences share a filing.

The table carries its own reading, and the debt footnote dates it: the year’s notes came in two offerings, six tranches issued September 2025, $18.0 billion, and eight issued February 2026, $25.0 billion. (31) Set the long tenors side by side. Twenty years: 5.875 percent in September, 6.55 in February. Thirty: 5.95, then 6.70. Forty: 6.10, then 6.85. The same company, the same seniority, the same tenor, five months apart, at 67 to 75 basis points more. A coupon is a base rate plus a credit spread, and the filing leaves them undecomposed, so we do too; the company pays the coupon whichever component moved. The February notes, $25.0 billion, plus the preferred issued the same month, $5.0 billion, sum to the $30 billion the third-quarter release reported raising “on a record order book that was substantially oversubscribed.” The furnished layer reported the demand. The filed layer reports the price.

Interest expense for the year was $4.6 billion, up a billion. (32) Of the $130.1 billion of principal outstanding, $90.3 billion matures beyond fiscal 2031. (33) The schedule of the money is filed beside the depreciation schedules of the equipment.

What the auditor marked as hard

Ernst & Young’s report names one Critical Audit Matter for fiscal 2026, the designation reserved for the accounts or disclosures that involved especially challenging, subjective, or complex judgment. The matter named is uncertain tax positions: the judgment in intercompany transfer pricing. (34)

Three weeks ago we read another auditor’s report on another company in this business. Deloitte & Touche named two Critical Audit Matters at CoreWeave, and both were the compute contracts themselves: whether the arrangements are services or leases, the judgment on which the presentation of the economics turns, and whether the financing vehicle must be consolidated. (35) CoreWeave’s remaining performance obligations are $98.8 billion; Oracle’s are $638 billion, entered into substantially in one year, in the same category of business. At the smaller company, the auditor recorded that the contracts were among the hardest calls in the audit. At the larger, the hardest call recorded was taxes. Two firms, two judgments about where the difficulty lives, under one standard. The reader weighs them.

The question

The question is the one our CoreWeave piece ended on: whether a unit of compute is sold for more than it costs to deliver. There, the filings hold every input, and even there the question resists a single answer. The calculation turns on how the disclosures are read and the order in which they are assembled, and the two judgments it turns on most, whether the contracts are services or leases, and whether the financing vehicle is consolidated, are the same two the auditor marked as the hardest calls in the audit. (35)(36) A reader can run the calculation. Different readings run to different results. The inputs are filed; the answer is a judgment.

Here the inputs are not even separable. The segment stops at cloud-and-software combined; depreciation stays unallocated in the consolidated totals; the cost of delivering an OCI dollar sits inside the column, undivided, exactly as the standards require of two businesses run as one. The only answer anywhere on the record is furnished: management said on the fourth-quarter call that margins in the new structures are “either at or better than the prior contracts.” (37) The conclusion, without the inputs. Each posture is what the rules make available to each structure. The pure-play filed the inputs and left the judgment open; the diversified company furnished the conclusion and consolidated the inputs.

We would like to answer it. At the pure-play, the honest answer is plural: one result per reading of judgments the auditor itself marked hard. Here, the disclosure that would start the arithmetic is a segment line the rules do not require and the filings do not contain. The absence is structural: the column is built as one because the business is run as one, and the question stays open by construction for everyone outside the CODMs’ own view. The lenders stood outside it too. The only outside prices the filing prints are the capital’s, the coupons in the table above and the 6.50 percent on the preferred, and they price the column whole, never the split. That price may well be right. The filing shows only what it was set against. So the question stands where the rules leave it, in the reader’s hands, and only one thing moves it: the next annual report divides the column further, or carries it whole. The asking begins there.

Notes

(1) Cape Fear Advisors, “Adding It Up: The Quality of Cash,” June 23, 2026, reading Oracle Corp.’s Form 10-K for the fiscal year ended May 31, 2026.

(2) Oracle Corp., Form 10-K for the fiscal year ended May 31, 2026 (filed June 22, 2026), Reports of Independent Registered Public Accounting Firm (Ernst & Young LLP), and Item 9A, Controls and Procedures.

(3) Form 10-K. Total revenues were $67,357 million, up 17%. Net income was $17,087 million, including a $2.7 billion realized gain on the Ampere transaction, read in the June 23 piece.

(4) Form 10-K, MD&A, Liquidity and Capital Resources. Quoted verbatim on the expected trend in capital expenditures.

(5) Form 10-K, MD&A. Oracle’s non-GAAP free cash flow table: net cash provided by operating activities $31,977; capital expenditures $(55,663); free cash flow $(23,686); free cash flow as a percentage of net income, (139)%, versus (3)% in fiscal 2025.

(6) Form 10-K, Consolidated Statements of Cash Flows, fiscal 2026, gross basis. Sources: operating cash $31,977; proceeds from senior notes, term loan credit agreements and other borrowings, net of issuance costs, $46,093; mandatory convertible preferred stock, net, $4,954; short-term financing related to capital expenditures, net, $3,345; issuances of common stock $1,449; sales and maturities of marketable securities and other investments $5,848; effect of exchange rates $96. Total, $93,762. Uses: capital expenditures $55,663; repayments of senior notes, term loans and other borrowings $6,942; repayments of commercial paper, net, $2,285; dividends $5,787; purchases of marketable securities and other investments and acquisitions $2,039; repurchases of common stock and shares withheld for taxes $206; other financing, net, $337; net increase in cash $20,503. Total, $93,762.

(7) Form 10-K, restructuring note. The 2026 Restructuring Plan, approved and initiated in fiscal 2026, with total estimated costs of up to $2.1 billion; $1.8 billion recorded in fiscal 2026. Rationale quoted verbatim in fragment.

(8) Form 10-K, notes payable and other borrowings: $129.5 billion total at May 31, 2026, versus $92.6 billion a year earlier; principal outstanding of $130.1 billion.

(9) Form 10-K, revenue disclosures: software support revenues of $19,804 million (fiscal 2026), $19,523 million (fiscal 2025), $19,609 million (fiscal 2024).

(10) Form 10-K. Cloud services revenue (SaaS and IaaS) of $33,989 million; cloud infrastructure (IaaS) growth of 77%.

(11) Form 10-K, MD&A, quoted verbatim and in full: “Our largest source of operating cash flows is cash collections from our customers following the purchase and renewal of their cloud and software support agreements.” The sentence names cloud agreements and software support agreements together; the filing does not apportion operating cash between them.

(12) Oracle Corp., Form 10-K for the fiscal year ended May 31, 2011, Item 1: “Cloud computing environments provide on demand access to a shared pool of computing resources in a self-service, dynamically scalable manner,” and “Cloud computing has evolved from technologies and services that Oracle has provided for many years.” In that filing the word describes an environment; it appears in no revenue segment name.

(13) Oracle Corp., Form 10-K for the fiscal year ended May 31, 2013: the software business’s first operating segment is “new software licenses and cloud software subscriptions.” The fiscal 2012 Form 10-K’s corresponding segment was “new software licenses,” with cloud appearing in a segment name for the first time in the fiscal 2013 report.

(14) Form 10-K (fiscal 2026), quoted verbatim: segment disclosures “align to how our chief operating decision makers (CODMs), which are our Chief Executive Officers and Chief Technology Officer, view our operating results and allocate resources.” The three businesses, cloud and software, hardware, and services, per Item 1 and Note 13. Segment reporting under ASC 280 follows the management approach: the reportable segments are the components the CODMs review.

(15) Form 10-K, MD&A segment results, Cloud and Software Business. Revenues of $58,530 million (fiscal 2026), $49,230 million (2025), $44,464 million (2024). Cloud and software expenses of $16,850 million, $10,827 million, and $8,783 million; sales and marketing expenses of $7,212 million (fiscal 2026) versus $7,473 million (2025), a 3% decline. Total margin of $34,468 million on $58,530 million (59%), versus $30,930 million on $49,230 million (63%) and $28,514 million on $44,464 million (64%).

(16) The June 23 piece, on the pattern: names where the accounting compels them (Ampere, TikTok USDS Joint Venture LLC), the aggregate where it permits the group.

(17) Oracle Corp., Form 8-K, June 30, 2025 (Regulation FD). Quoted verbatim in fragment.

(18) Form 10-K, Note 1 (attribution of the RPO increase, quoted verbatim in fragment) and the concentration disclosure: “No single customer accounted for 10% or more of our total revenues in fiscal 2026, 2025 or 2024.”

(19) OpenAI and Oracle joint announcements regarding Stargate data-center capacity, including the July 2025 expansion. Statements by the parties, not filings. The announcements state the partnership; they state no dollar amount and draw no connection to the contract disclosed in the June 30, 2025 Form 8-K.

(20) The ~$300 billion figure originates in press reporting (The Wall Street Journal, September 2025) and subsequent coverage. We searched Oracle’s SEC filings and both companies’ own communications for the figure, or for any allocation of remaining performance obligations to a named customer, and found none. On Oracle’s September 2025 earnings call, following the reports, the question was put to executives and no counterparty details were provided.

(21) Form 10-K, Item 1A, Risk Factors, quoted verbatim.

(22) The June 23 piece, note (7) there: the $75 billion appears in the earnings release furnished June 10, 2026 (Form 8-K, Exhibit 99.1, Item 2.02), and does not appear as a line in the audited statements.

(23) Form 10-K, Consolidated Statements of Cash Flows: “Increase in deferred revenues from customer prepayments with significant financing component,” $4,592 million in fiscal 2026, with no comparable amount in fiscal 2025 or 2024.

(24) Form 10-K, balance sheet and Note 7: deferred revenues of $15,395 million ($9,916 current, $5,479 non-current) at May 31, 2026, versus $10,733 million ($9,387 current, $1,346 non-current) a year earlier.

(25) Oracle Corp., Form 8-K (Exhibit 99.1), furnished June 10, 2026, and the fiscal Q4 2026 earnings call: “net cash outlay for capital expenditures,” defined as capital expenditures less short-term financing related to capital expenditures and less customer prepayments. Furnished, on the same Item 2.02 posture.

(26) Form 10-K, Consolidated Statements of Cash Flows and MD&A. The statement line of $46,093 million includes term loan credit agreements and other borrowings and is net of issuance costs; the $43.0 billion is the stated par value of the fiscal 2026 senior notes. Mandatory Convertible Preferred Stock: 6.50% Series D, issued February 5, 2026, cash proceeds of $5.0 billion net of issuance costs. Short-term financing related to capital expenditures, net: $3,345 million.

(27) Form 10-K, MD&A: equity distribution agreement entered February 2, 2026, for an at-the-market program of up to $20 billion; no shares sold under it as of May 31, 2026.

(28) Oracle fiscal Q4 2026 earnings call (furnished): approximately $40 billion of expected debt and equity financing in fiscal 2027, including the announced $20 billion at-the-market program; net cash outlay for capital expenditures of approximately $70 billion, excluding $20–25 billion of expected customer prepayments and timing.

(29) Form 10-K, MD&A, Liquidity and Capital Resources: “During fiscal 2026, we issued a total of $43.0 billion par value of senior notes comprising the following,” the fourteen tranches as tabled, in the filing’s own order.

(30) Form 10-K, Item 1A, Risk Factors, quoted verbatim in fragments: hardware excess-and-obsolescence risk expected to continue; useful lives and performance characteristics that may differ from expectations; lease terms that typically do not align with the duration and pricing of customer contracts.

(31) Form 10-K, Note 6, which tabulates a date of issuance and an effective interest rate for each tranche: six tranches issued September 2025 totaling $18.0 billion; eight issued February 2026 totaling $25.0 billion. Effective rates at the long tenors: 5.91% (September 2045) against 6.59% (February 2046); 6.05% against 6.74%; 6.17% against 6.89%. Oracle fiscal Q3 2026 earnings release, March 10, 2026 (Form 8-K, Exhibit 99.1, furnished): “Within days of the announcement, Oracle raised $30 billion through a combination of investment grade bonds and mandatory convertible preferred stock, with a record order book that was substantially oversubscribed.”

(32) Form 10-K: interest expense of $4,599 million in fiscal 2026, versus $3,578 million in fiscal 2025.

(33) Form 10-K, maturities of notes payable: fiscal 2027 $7,210 million; 2028 $10,145; 2029 $5,500; 2030 $7,250; 2031 $9,750; thereafter $90,250.

(34) Form 10-K, Report of Independent Registered Public Accounting Firm: a single Critical Audit Matter, uncertain tax positions, centered on intercompany transfer pricing.

(35) Deloitte & Touche LLP, Report of Independent Registered Public Accounting Firm in CoreWeave, Inc.’s Form 10-K (fiscal 2025): two Critical Audit Matters, the assessment of customer contracts as service arrangements versus leases, and the consolidation analysis of the financing joint venture. CoreWeave’s remaining performance obligations of $98.8 billion per its Form 10-Q for the quarter ended March 31, 2026.

(36) Cape Fear Advisors, “CoreWeave, Adding It Up,” June 13, 2026.

(37) Oracle fiscal Q4 2026 earnings call (furnished): management’s statement that margins on the new large contracts are “either at or better than the prior contracts.” A call remark; the Form 10-K reports margin at the cloud-and-software segment level and above.

The quality of cash, applied to Oracle’s full fiscal 2026 annual report. Sources: Oracle Corp. Form 10-K for the fiscal year ended May 31, 2026; Oracle Corp. earnings releases (Form 8-K, Exhibit 99.1) for fiscal Q3 and Q4 2026; Oracle Corp. Form 8-K, June 30, 2025 (Regulation FD); Deloitte & Touche LLP audit report in CoreWeave, Inc.’s Form 10-K; CoreWeave, Inc. Form 10-Q for the quarter ended March 31, 2026. Figures verified against the primary filings. Analysis: Cape Fear Advisors.

Greg Collins serves as CEO of C3 Metrics, a marketing measurement and analytics firm, and maintains an advisory practice at Cape Fear Advisors focused on structural analysis and strategy.

This article is also available on Substack.

Start a Conversation →