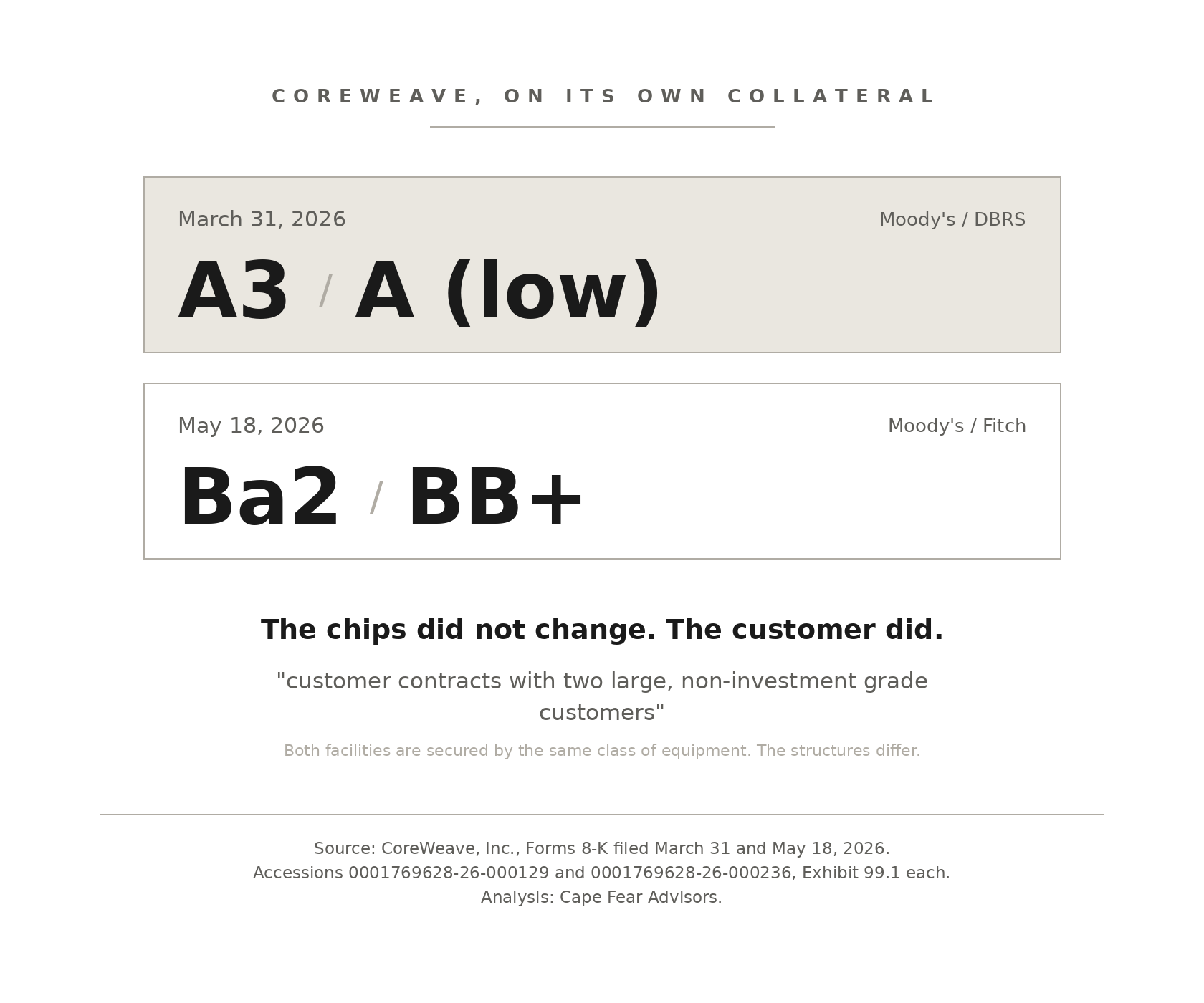

Two loan facilities, seven weeks apart. Same borrower, the same graphics processors in the same buildings. Moody’s rated the first A3, a notch above SpaceX and two above Oracle. It rated the second Ba2, below investment grade. The filing states, in a single clause, what changed: the second facility’s customers are not investment grade. Five notches, and two and a quarter percentage points a year. The one difference the filings put in words is whose promise stood behind the machines.

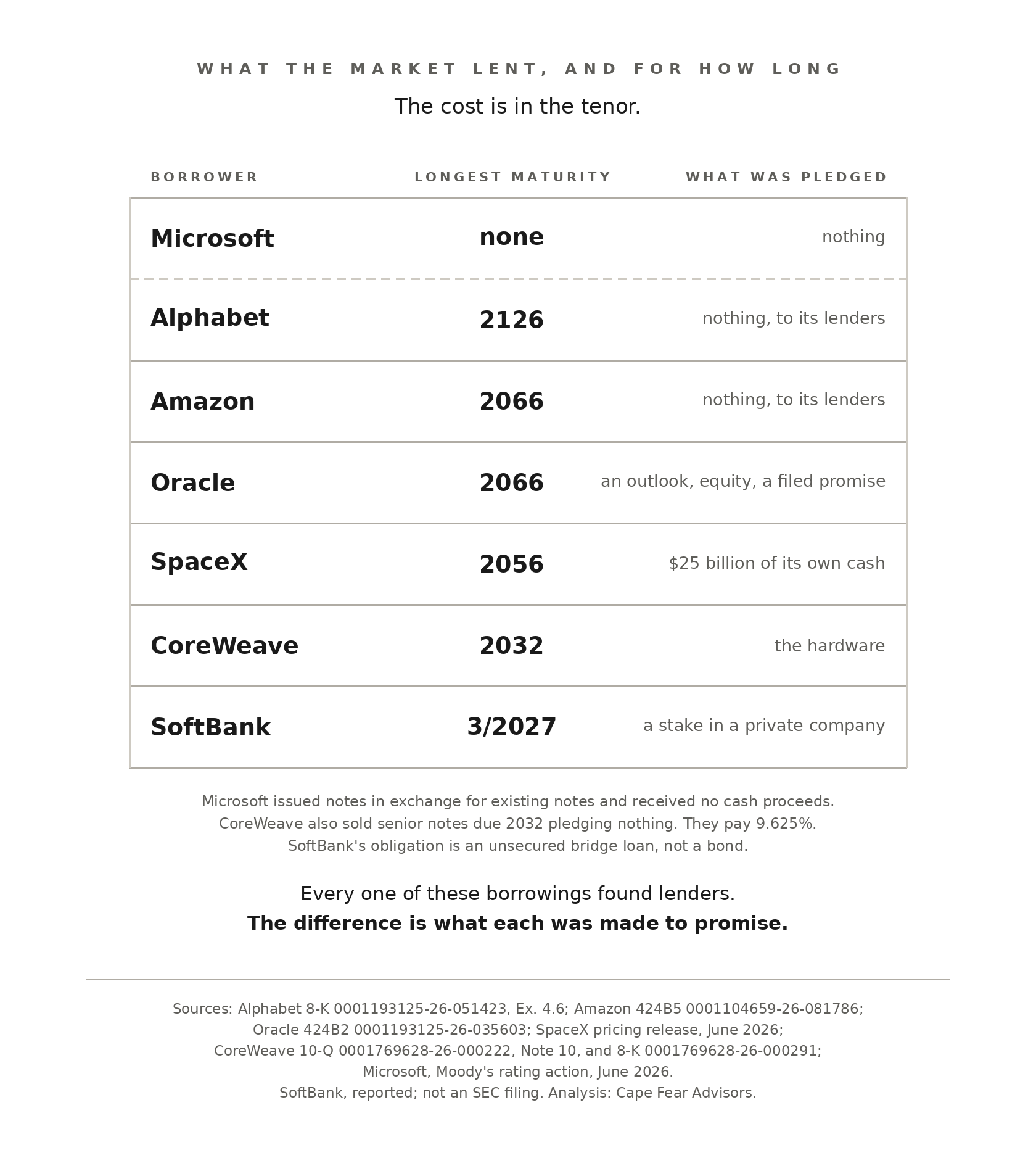

The same asymmetry runs the length of the year’s bond calendar. Alphabet borrowed to 2126 and Amazon to 2066, pledging nothing to their lenders. Oracle reached the same 2066, having filed a promise not to return to the bond market. SpaceX holds at least twenty-five billion dollars of cash still, which Moody’s calls a key credit consideration. Nothing CoreWeave has issued reaches past 2032. SoftBank pledged a stake no market prices daily, and was asked to add a guarantee on top. Every bond sold. And the borrowers who pledged nothing and borrowed longest are the same companies that supply the buildout, hold equity in its buyers, and earn on everything those buyers spend. None of it is irregular, and none of it is hidden. What is not evenly distributed is the rake.

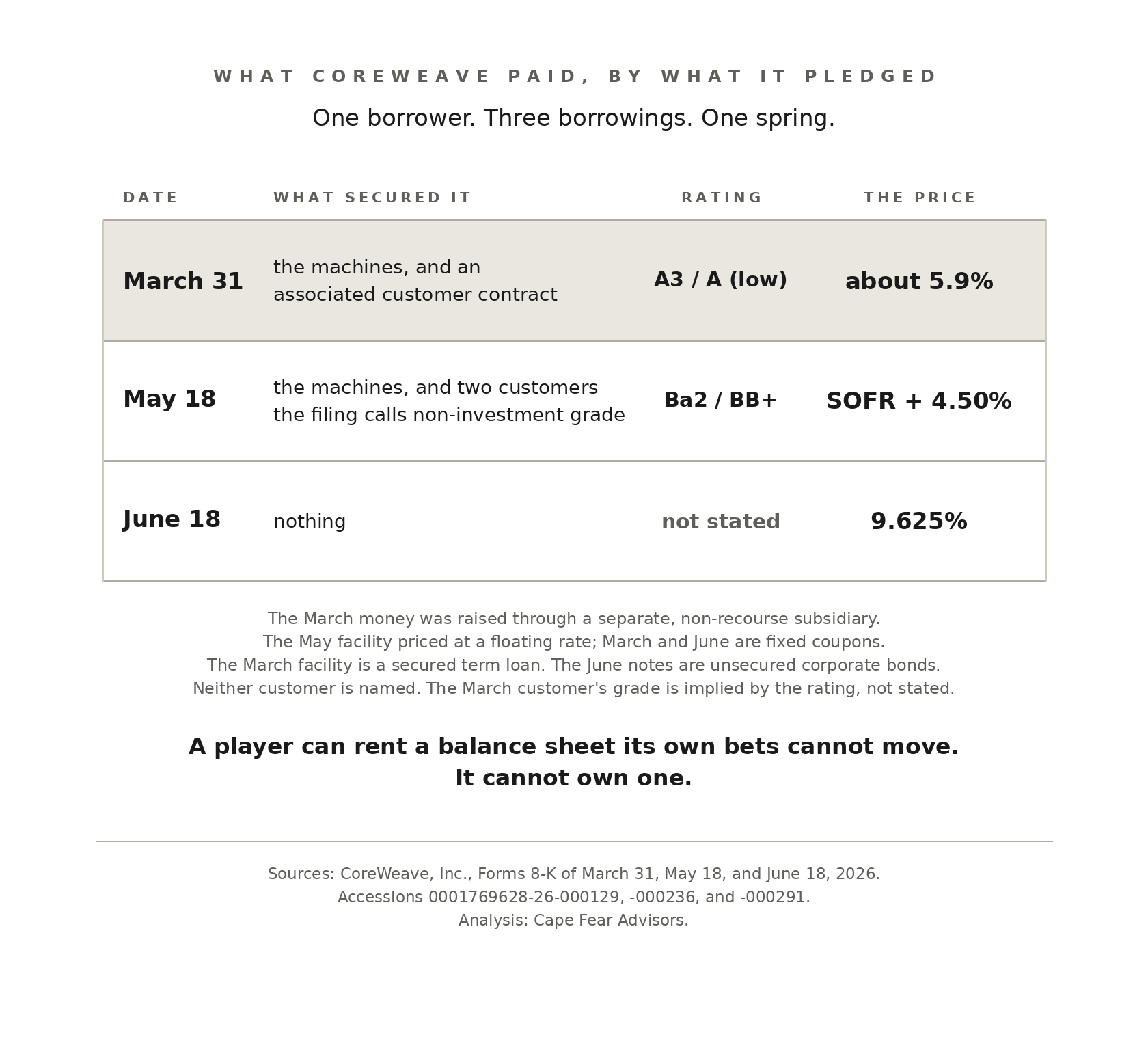

On March 31 CoreWeave filed a current report announcing an $8.5 billion loan facility. Moody’s rated it A3 and DBRS rated it A (low), and the company described the transaction, correctly, as the first investment-grade rated financing secured by high-performance computing infrastructure and an associated customer contract. The floating portion priced at 2.25 percentage points over the benchmark short-term lending rate. The facility matures in March 2032. It is non-recourse, meaning the lenders may look to a single subsidiary, CoreWeave Compute Acquisition Co. VIII, LLC, and not to CoreWeave itself. The customer is not named. (1)

Seven weeks later, on May 18, the same company filed another current report announcing another facility, this one $3.1 billion. Same collateral, graphics processors installed in data centers. Same two banks leading the syndicate. Moody’s rated this one Ba2 and Fitch rated it BB+. Both are speculative grade. It priced at 4.50 percentage points over that same benchmark, after tightening by half a point on demand the company called exceptional. The filing states what changed, in its own words. The proceeds support “customer contracts with two large, non-investment grade customers.” (2)

Five notches, seven weeks, and two and a quarter percentage points a year. The chips did not change. The customer did.

A3 sits one notch above the rating Moody’s assigned SpaceX in June and two above the rating it carries on Oracle. A3 is a rating on the facility. Baa1 and Baa2 are ratings on the companies. Set the borrower aside and the arithmetic is plain. Silicon in a warehouse, pledged beside a tenant’s contract that the rating implies is investment grade, borrows better than Oracle borrows. The same silicon, pledged beside two tenants who lack that rating, borrows below investment grade.

The A3 belongs to a ring-fenced entity whose paper carries somebody else’s promise to pay.

That is a seat. The seat is whose promise stands behind the position, and the market prices it in an indenture, every time, without ever saying so out loud.

The bond calendar

Three times this year a borrower has asked the American bond market for exactly twenty-five billion dollars. Oracle in February, SpaceX in June, Amazon this week. Alphabet asked for fifteen billion in February and took twenty, on more than a hundred billion of orders. (16) CoreWeave’s speculative-grade facility tightened during syndication. Every bond sold. The market wanted to lend at every seat at the table.

What varied was the promise it extracted.

Alphabet pledged nothing to its lenders and borrowed for a century. Its 6.125% notes due 2126, one billion pounds, dated February 13 of this year, come due on February 13 of the year twenty-one twenty-six. No covenant, no cash floor, no stated project. The century tranche drew close to ten times its size in orders. (16) Alphabet may buy the bond back at any time before August 2125, by compensating the holders. (4)

Amazon pledged nothing to its lenders and borrowed to 2066. Eight tranches, twenty-five billion dollars exactly, coupons from 4.600 percent to 6.250 percent. The prospectus says the money is for “general corporate purposes, which may include, but are not limited to, repayment of debt, acquisitions, investments, working capital, investments in our subsidiaries, capital expenditures, and repurchases of outstanding shares of our common stock.” (5) Forty-year money whose stated purpose includes buying back the borrower’s own stock. Amazon was not obliged to justify the loan, and did not.

Oracle pledged its conduct. Moody’s rates it Baa2 with a negative outlook and S&P rates it BBB with a negative outlook, both citing the capital program and the concentration of its cloud revenue in a small number of counterparties. In a free writing prospectus filed February 1, Oracle told the market it expected to raise forty-five to fifty billion dollars during the calendar year. Roughly half would come from selling stock, or instruments that convert into stock. The other half would come from one bond deal, and only one. “Oracle does not expect to issue additional bonds during calendar year 2026 beyond this transaction,” the document says, and “this funding plan reflects Oracle’s commitment to maintaining an investment-grade rating.” (6) A promise about future conduct, filed with the Commission, to protect a letter. The market then lent it twenty-five billion dollars across eight tranches reaching 2066, the same year Amazon reached this week.

SpaceX pledged cash. Moody’s assigned Baa1 with a stable outlook on June 18, and its rating action states that “a key credit consideration is SpaceX’s intention to maintain at least $25 billion of cash and marketable securities, supplemented by full revolver availability,” alongside a consolidated leverage covenant tested quarterly with no step-downs. Days later the company priced twenty-five billion dollars across five tranches, the longest running to 2056, with proceeds named to the repayment of its bridge loan in full. (7) Twenty-five billion dollars held motionless in order to borrow twenty-five billion dollars, and the borrowed money was told where to go.

CoreWeave pledged the hardware. Its debt stack carries a weighted average effective rate of 9.1 percent, and 9.9 percent excluding the convertibles. Fifty-nine percent of principal, nearly fifteen billion dollars, carries an effective rate of ten percent or higher. The most expensive facility runs at fifteen percent. The company discloses that its debt “bears interest at variable rates, the majority of which is unhedged.” (8) Nothing in its capital structure matures after 2032.

CoreWeave borrowed three times this spring. In March it pledged the machines and an investment-grade customer’s contract, and the fixed portion of that money cost about 5.9 percent. In May it pledged the machines and two customers who are not investment grade, and paid 4.50 percentage points over the benchmark. In June it pledged nothing at all, borrowing on its own name, and paid 9.625 percent. Its other unsecured notes pay 9.000, 9.250, and 9.750 percent. (8)

What stands behind those chips is a small number of promises. Committed contracts, which are take-or-pay and typically carry a prepayment, produced 98 percent of CoreWeave’s revenue in the first quarter. Roughly 65 percent of that revenue came from two customers, and no other customer reached ten percent. A year earlier a single customer produced 72 percent. One of the two is OpenAI, under a master services agreement signed in May 2025. Whether either of those customers is a party to either facility is not disclosed. (9)

Banks lent SoftBank forty billion dollars unsecured, against no collateral at all, and that bridge comes due in March 2027. S&P rates the company BB+, below investment grade, and cut the outlook to negative in March. When SoftBank sought ten billion dollars more against its OpenAI shares, the market declined. Reporting has it cutting the target by forty percent when lenders hesitated at collateral that no public market prices daily, watching the talks stall in June, and reviving them only by offering a corporate guarantee, so that lenders could look past the pledged stake to SoftBank itself. (14)

A century, forty years, thirty years, six years, and a margin call. The order books were full at every one of them.

The other side of the table

The inversion sits on the page. The buildout’s shortest paper funds the equipment with the shortest life. Alphabet borrows to 2126. CoreWeave borrows to 2032 against equipment its own annual report depreciates over six years, an estimate the company makes and reviews, and every dollar of that stack must be refinanced, on terms nobody can know, before the machines it bought have finished paying for themselves. The company that sells CoreWeave those machines states in its own annual report that it brings new advanced architectures “on a one-year product cadence.” (13) The refinancing clock spins fastest exactly where the assets melt.

A house is legible from the other side of the table.

Microsoft approached the table and walked away without money. Its most recent notes carry Moody’s highest rating, and the agency’s own action explains that the company “will not receive any cash proceeds from the issuance of the new notes in the exchange offers,” because the old notes were surrendered, retired, and cancelled. (3) The paperwork moved. The money did not.

It watches from a seat it does not have to fund. It holds approximately 27 percent of OpenAI on an as-converted basis, accounted for under the equity method. Its own filing describes Microsoft as “a major investor in OpenAI” which “will continue to receive revenue-sharing payments,” and which holds “rights to OpenAI’s intellectual property, including models and infrastructure.” Under the restructuring announced in April, Microsoft’s revenue-share payments to OpenAI end, while OpenAI’s payments to Microsoft continue through 2030 against a cap. And when Microsoft reports adjusted net income, its own preferred measure, that measure excludes net gains and losses from its investments in OpenAI. Across the nine months ended March 31, the difference between the two figures is roughly four and a half billion dollars, and the difference is the position in the buyer. (10)

Amazon is the same shape, doubled.

It borrowed to 2066 for purposes that include, in the prospectus language, investments. Between 2023 and 2025 it invested eight billion dollars in Anthropic convertible notes. In the first quarter Amazon put fifteen billion dollars into OpenAI Series C preferred stock and signed a letter agreement committing thirty-five billion dollars beyond that, which it may exercise at its sole discretion and must exercise upon the earlier of specified milestones or an OpenAI public listing. In that same quarter AWS and OpenAI expanded an existing thirty-eight billion dollar commercial arrangement by one hundred billion dollars over eight years, an arrangement that “includes contractual obligations related to the performance of AWS chips.” The Anthropic arrangement is also primarily for the provision of AWS cloud services, and it also includes the use of AWS chips. (11)

Equity in both laboratories. Compute sold to both. The seller’s own chips written into both contracts. Forty-year money available for all of it.

NVIDIA sells CoreWeave the graphics processors that secure CoreWeave’s loans. CoreWeave spent $7.7 billion on property and equipment in the first quarter. In January, NVIDIA bought approximately 23 million shares of CoreWeave’s Class A common stock at $87.20 per share, two billion dollars, in a private placement. (12) The seller of the collateral holds equity in the borrower. NVIDIA’s own annual report observes that “access to capital can be particularly constrained for less-capitalized companies, which may face difficulties securing financing for large-scale infrastructure projects.” (13)

The commitments run among the same names. Microsoft funds OpenAI and sells OpenAI compute. Amazon funds both laboratories and sells both laboratories compute, with its own chips written into the contracts. NVIDIA sells the machines and holds equity in the company that buys the machines. Google sells the chips, and states that in connection with certain of those agreements it provides credit backstops to support third-party data centers. It carries an equity derivative in a private company it does not name. (15) What the houses commit to one another, they commit against balance sheets the market lends to for a century.

None of that is irregular. Vendors have financed their customers since the first equipment lease. Special purpose vehicles, take-or-pay contracts, credit backstops, prepayments: this is the ordinary furniture of capital-intensive industry, and in these filings each one appears correctly characterized and correctly disclosed.

Several of these filings also rest on judgment. A useful life is an estimate. A materiality threshold is a determination. The characterization of an instrument is a choice among permitted treatments, and so is the measure a company asks the market to judge it by. In every case the judgment belongs to the filer, and in every case the filer made it and disclosed it. The circle is not the finding, and neither is the judgment.

What is not evenly distributed is the rake. Taking a margin on the flow, holding a position in whoever pays the margin, and pricing that position against a balance sheet the position cannot move. The third condition is what permits the first two. A player can borrow money. It owns a balance sheet, and its own bets move it. What it can do is rent a balance sheet that its bets cannot move, for one facility, at a stated price. That price is on the page. About five point nine percent when CoreWeave borrowed behind an investment-grade customer’s promise, and 9.625 percent when it borrowed behind its own. Three and three-quarters percentage points separate the two. Some of that gap is the collateral, some is the structure, and some is whose promise stood behind it, and the filings do not separate them. Whatever share of it is rent, the rent is payable one facility at a time. What a player cannot do is own one.

The bond market does not argue with any of it. It prices it. A century of duration for one credit and nothing past 2032 for another is a view, stated in the only language an indenture has. So is twenty-five billion dollars of cash held still. So is two hundred twenty-five basis points for the difference between one customer’s promise and another’s. The market does not raise its voice. It writes the number into the term, and the term into the paper, and then the paper trades.

Which returns the question to the seat, and to what the seat is made of.

Alphabet accounts for its data-center backstops as credit derivatives, and its most recent quarterly states both numbers: the most it could ever be called on to pay, $28.4 billion, and what it carries the promise as worth, a liability of $339 million, which the company describes as not material. (15) That is what a ledger of lent credit looks like on a house’s balance sheet. An investment-grade rating on a warehouse of graphics processors is what the invoice looks like when an agency prints one.

Somewhere behind that facility is a customer whose promise turned pledged silicon into investment-grade paper. CoreWeave did not name it. TeraWulf, disclosing a twenty-year Anthropic lease at Hawesville, Kentucky, worth roughly nineteen billion dollars of contracted revenue, said only that the payments are “expected to be supported by an investment-grade credit,” and did not name that either. (15) No rule required either of them to name a counterparty, and nothing here identifies either one. The tenants are named. The credits go unnamed.

Every bond at this table sold. The one borrowing that did not clear was SoftBank’s, against a stake in a private company, and it moved only when SoftBank offered its own guarantee on top of the collateral. What separated these borrowers was not whether the money was there, and not the size of the ask, and not the quality of the collateral, which in CoreWeave’s case was identical across five notches.

What separated them was the cash standing behind the paper. Whose it was. How it was earned. Whether the promise to pay it could survive the position going wrong. A promise from a balance sheet the bet cannot move is worth a century. A promise from two customers who are not investment grade is worth five and a half years.

The price of the seat is the quality of the cash behind it.

Between March and May the promise behind CoreWeave’s paper changed. The filings name neither customer. They state the credit quality of one pair, and the rating of the other, and they leave everything else alone. What they do state is the price of the difference: five notches, and two hundred twenty-five basis points.

Who owns the house, which tables are open, who is sitting at which tables, and who wants a seat?

The cost is in the tenor.

Cape Fear Advisors holds no position in and makes no recommendation regarding any security mentioned in this analysis.

This analysis was originally published on Substack, where free subscribers receive every piece.

Get in TouchNotes

(1) CoreWeave, Inc., Form 8-K filed March 31, 2026, accession 0001769628-26-000129, Items 1.01 and 2.03, Exhibit 99.1. States the A3 and A (low) ratings, the non-recourse structure, the floating tranche at SOFR plus 2.25% and a fixed tranche at approximately 5.9%, the March 2032 maturity, and the securing entity. Item 1.01 filings are required, not elective. FILED.

(2) CoreWeave, Inc., Form 8-K filed May 18, 2026, accession 0001769628-26-000236, Items 1.01 and 2.03, Exhibit 99.1. States the Ba2 and BB+ ratings, final pricing at SOFR plus 4.50% after a fifty basis point tightening, an approximately 5.5 year maturity, issuance through CoreWeave Financing DDTL V, LLC, and the credit quality of the two customers. That the March facility’s unnamed customer is investment grade is an INFERENCE drawn from the rating and from the contrast with this filing. It is not stated. Neither customer is named in either filing. The two facilities also differ in structure: the March facility is non-recourse through a separate entity and was privately arranged; the May facility was publicly syndicated through a different entity. Both are secured by high-performance computing infrastructure.

(3) Moody’s Ratings, rating action assigning Aaa to Microsoft’s new notes, June 2026; quoted language verbatim. Microsoft and Johnson & Johnson are the only two U.S. public companies rated AAA by S&P and Aaa by Moody’s. REPORTED.

(4) Alphabet Inc., Form 8-K filed February 13, 2026, accession 0001193125-26-051423, Exhibit 4.6, the global note for £1,000,000,000 of 6.125% Notes due 2126, principal due February 13, 2126, redeemable at the company’s option on a make-whole basis prior to August 13, 2125. Alphabet is rated AA+, not AAA. FILED.

(5) Amazon.com, Inc., Form 424B5 filed July 8, 2026, accession 0001104659-26-081786, Registration No. 333-293246. This is the priced prospectus supplement; the preliminary supplement of July 7, accession 0001104659-26-080950, states the tranches without amounts or coupons. Eight tranches totaling $25.0 billion, maturities 2029 through 2066, coupons 4.600% to 6.250%. The use of proceeds language is verbatim. FILED.

(6) Oracle Corporation, free writing prospectus filed February 1, 2026, pursuant to Rule 163, accession 0001193125-26-032650, Registration No. 333-277990. All quoted language is verbatim. Tranche detail from Oracle’s Form 424B2, accession 0001193125-26-035603, Registration No. 333-277990: $25,000,000,000 across eight tranches, the longest maturing in 2066. The Moody’s and S&P ratings and outlooks are REPORTED. FILED.

(7) Moody’s Ratings, rating action assigning Baa1 to Space Exploration Technologies Corp., June 18, 2026; quoted language verbatim. Fitch assigned BBB+ and S&P assigned BBB, both stable. Tranche detail from the company’s pricing announcement of its inaugural $25 billion issuance, settled June 26, 2026. Baa1 is three notches above Baa3, the lowest investment grade rating at Moody’s. REPORTED and FURNISHED.

(8) CoreWeave, Inc., Form 10-Q for the quarter ended March 31, 2026, accession 0001769628-26-000222, Note 10, Debt, for the weighted average rate, the distribution of rates, and the maturities. Rates in that note are effective rates, which include issuance costs and discount, and are not coupons. The three spring borrowings, each from a filed current report: Form 8-K of March 31, 2026, accession 0001769628-26-000129, Exhibit 99.1, a facility secured by high-performance computing infrastructure and an associated customer contract, non-recourse to CoreWeave, floating tranche at 2.25 points over the benchmark short-term rate and a fixed tranche at approximately 5.9%, maturing March 2032; Form 8-K of May 18, 2026, accession 0001769628-26-000236, Exhibit 99.1, secured, priced at 4.50 points over that benchmark, supporting contracts with “two large, non-investment grade customers”; Form 8-K of June 18, 2026, accession 0001769628-26-000291, Item 1.01, $1,250 million of 9.625% dollar-denominated senior notes and EUR 2,000 million of 8.500% euro-denominated senior notes, senior unsecured, guaranteed by subsidiaries, maturing July 15, 2032. Existing unsecured coupons of 9.000%, 9.250% and 9.750% appear in CoreWeave’s April 2026 current reports. The March money was raised through a separate, non-recourse subsidiary and the June money on the parent’s own credit. The collateral, the customer’s contract, and the structure all sit inside the difference between the two rates. The May facility priced at a floating rate; the March and June figures are fixed coupons. FILED.

(9) The same CoreWeave 10-Q. Committed contracts are described as take-or-pay and as typically including a customer prepayment; they produced 98% of revenue in each of the three months ended March 31, 2026 and 2025. The top two customers produced approximately 65% of revenue in the quarter, with no other customer at 10% or more; the top customer alone produced approximately 72% a year earlier. The master services agreement with OpenAI OpCo, LLC dates to May 2025, with an order form in September 2025. CoreWeave’s revenue concentration and the customers of its financing facilities are separate disclosures. No filing states whether the two sets overlap, and nothing here suggests that they do. FILED.

(10) Microsoft Corporation, Form 10-Q for the quarter ended March 31, 2026, accession 0001193125-26-191507. The 27 percent as-converted equity method investment, the hypothetical liquidation at book value method, and the $13 billion of total funding commitments of which $11.8 billion was funded, are stated in the filing, as is the quoted partnership language. The filing states that the partnership was extended in October 2025 and April 2026. Adjusted net income is a non-GAAP measure that, in the company’s words, excludes net gains and losses from investments in OpenAI; nine month reported net income was $97,983 million against $93,500 million adjusted. The difference reflects net gains, not losses. FILED. The direction of the revenue share after the April restructuring, and the 2030 term and cap, are REPORTED, and were read at length in “Microsoft just said a lot about SpaceX” (Cape Fear Advisors, April 27, 2026).

(11) Amazon.com, Inc., Form 10-Q for the quarter ended March 31, 2026, accession 0001018724-26-000014. States $8.0 billion of Anthropic convertible notes invested from Q3 2023 to Q4 2025, with conversion of portions to nonvoting preferred stock in Q1 2025 and Q1 2026. The filing also states a $15.0 billion Q1 2026 investment in OpenAI Series C Preferred Stock and a letter agreement for $35.0 billion of additional Commitment Shares, purchasable at Amazon’s sole discretion and mandatory upon the earlier of specified milestones or a public listing; the AWS expansion of an existing $38.0 billion commitment by $100.0 billion over eight years, with the quoted chip language; and, as a subsequent event, a further $5.0 billion invested in Anthropic nonvoting preferred stock. FILED. Anthropic is the developer of Claude, the model used in preparing this analysis. The figures above are quoted from Amazon’s filing without characterization.

(12) CoreWeave, Inc., Form 10-Q for the quarter ended March 31, 2026, accession 0001769628-26-000222: “In January 2026, we entered into a securities purchase agreement with NVIDIA Corporation for a private placement of approximately 23 million shares of our Class A common stock at a purchase price of $87.20 per share, for aggregate gross proceeds of $2.0 billion.” Purchases of property and equipment, including capitalized internal-use software, were $7,695 million in the quarter. FILED. What portion of CoreWeave’s equipment purchases is paid to NVIDIA is not disclosed.

(13) NVIDIA Corporation, Form 10-K for the fiscal year ended January 25, 2026, accession 0001045810-26-000021. Verbatim: “We continue to execute Data Center compute product introductions, bringing new advanced architectures on a one-year product cadence, including our Rubin platform.” The observation regarding access to capital appears in the same passage, verbatim. FILED.

(14) S&P Global Ratings outlook revision, March 2026. The margin loan sequence, the forty percent reduction in the target, the stall, and the corporate guarantee are REPORTED, sourced to Bloomberg and others. SoftBank has publicly stated that the $40 billion unsecured bridge, maturing March 2027, will be repaid through existing assets and other financing measures. SoftBank is not an SEC registrant for these obligations; nothing in this note is drawn from a filing with the Commission. REPORTED.

(15) Alphabet Inc., Form 10-Q for the quarter ended March 31, 2026, accession 0001652044-26-000048. The $28.4 billion gross notional and the $339 million fair value liability, described as not material, are read at length in “Apple just said a lot about Google” (Cape Fear Advisors, July 8, 2026). Alphabet is not named in, and is not stated to be a party to, the CoreWeave facility discussed above. FILED. Separately, and cited for a different proposition: TeraWulf, Inc., Form 8-K filed July 6, 2026, accession 0001104659-26-080583, Exhibit 99.1, for the Hawesville lease and the quoted phrase. That filing does not name the investment-grade credit it refers to. Neither does this piece. No connection between that credit and any filer named above appears in the record. FILED.

(16) The order books for Alphabet’s February offerings, the upsizing of the dollar tranche from fifteen to twenty billion dollars, and the roughly tenfold oversubscription of the sterling century tranche, are REPORTED, sourced to Bloomberg and others.