On June 1, Anthropic announced, in two sentences, that it had confidentially submitted a draft S-1; an offering is now reported for as soon as October. Before that document is public, a record assembled from the companies it pays for compute and the companies that pay to own a piece of it already draws much of the picture. This series read the financing before the filing once already. Here the question is wider: three kinds of not-knowing are familiar before a filing arrives, and a fourth, drawn on less often, is where this reading sits.

Three buckets, and a fourth

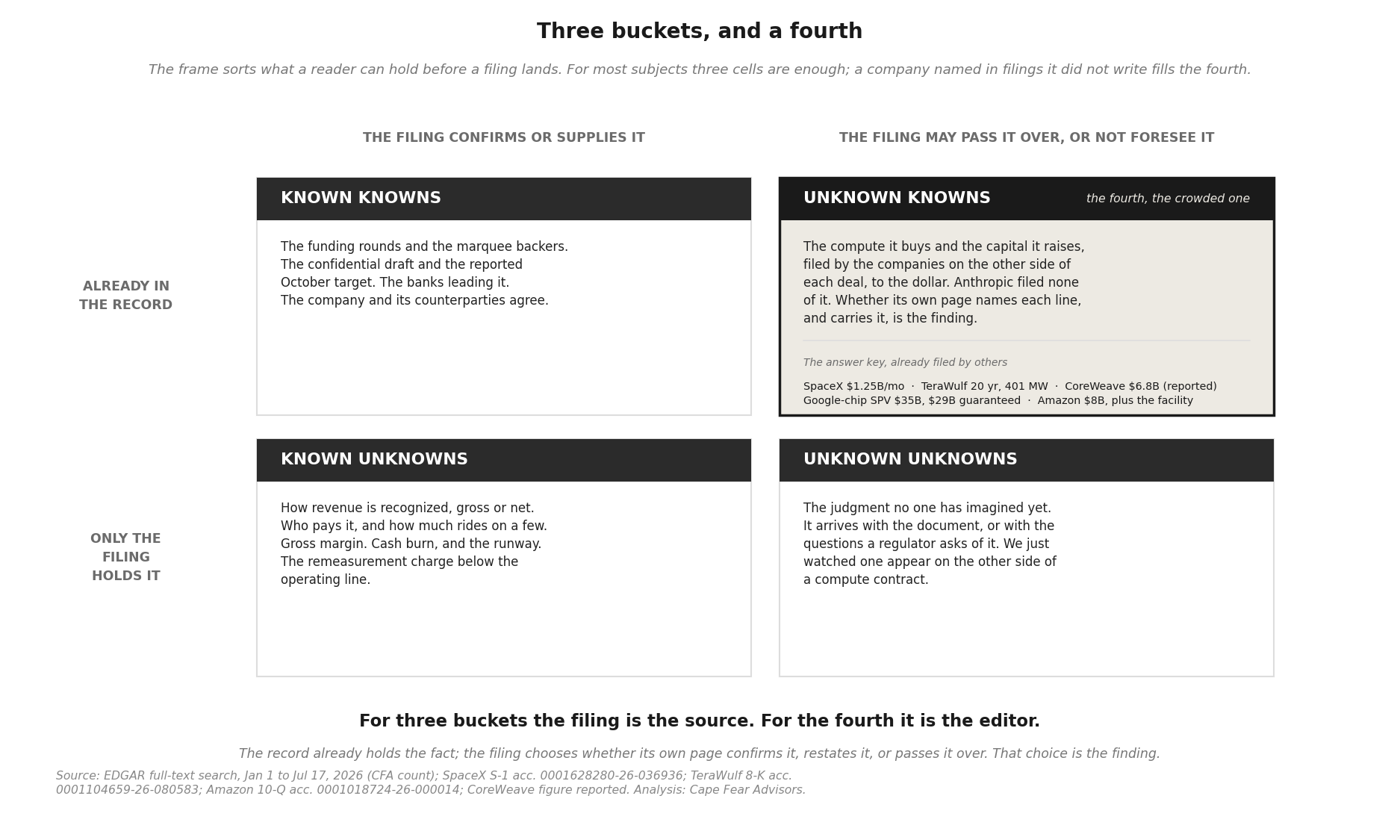

Donald Rumsfeld’s line about known knowns, known unknowns, and unknown unknowns has had a long life outside the podium where he said it. Olga Usvyatsky at Deep Quarry and Francine McKenna at The Dig reached for it this week, reading the distance between SpaceX’s confidential draft and its public prospectus to anticipate a review whose comment letters had not yet posted. It reads well against that question, and it marks a division of labor. Theirs reads a document against its own history, draft to prospectus and comment to amendment; ours reads it against everyone else’s record, whether the page names what the counterparties have already filed. Same filing, two reads that do not overlap, and the first is a craft others own. We borrow the frame with a nod to them and take the second. Their subject was a company midway through filing; ours has filed nothing, and that pulls the weight onto the quadrant a pre-filing read can usually leave empty: the fourth. The frame is old, and so is the name for that quadrant. We make no claim on either. What the fourth gives us is a way to read materiality, and the thresholds beneath disclosure, which is the work this series does.

The first three are the ones everyone quotes. A known known is disclosed and uncontested. A known unknown is a question without an answer yet, the kind a filing exists to supply. An unknown unknown cannot be anticipated at all; it arrives with the document, or with the questions a regulator asks of it.

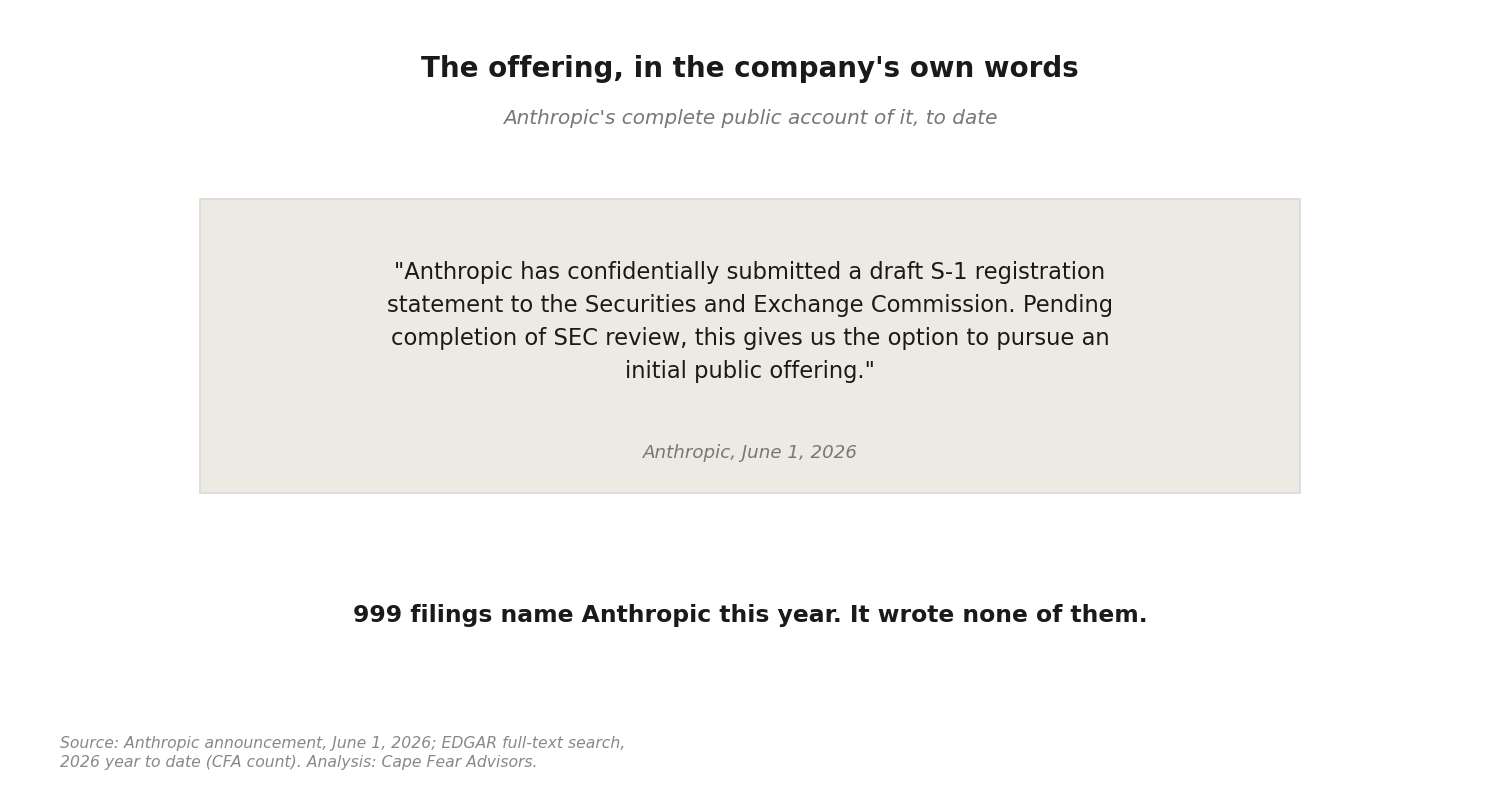

The fourth is the one that carries this piece. Call it an unknown known. The phrase came from elsewhere, borrowed by others before us; it titled Errol Morris’s documentary on Rumsfeld himself, among other uses. We take the words and mean something narrower by them. An unknown known, here, is a fact already in the public record, placed there by someone other than the company, most often in another company’s filing, that the company’s own document may not acknowledge. For most firms approaching an offering, that quadrant is close to empty, because little about a private company appears in anyone else’s filings. For Anthropic it is crowded. By our count, an EDGAR full-text search returns 999 filings that name Anthropic between January 1 and July 17 of this year. (12) Anthropic filed none of them; it is private and has no filings of its own. It speaks in its own voice readily enough elsewhere, in press releases that name its partners and state a revenue run-rate, but it files nothing. Its own account of the step toward this offering is the two-sentence announcement of June 1: that it has confidentially submitted a draft, and that the submission gives it the option to pursue a public offering. (13) Nine hundred and ninety-nine documents name the company. It wrote the two sentences.

Nine hundred and ninety-nine documents name the company. It wrote the two sentences.

Here is why the fourth bucket does the work. For the other three, the filing is the source. It confirms what everyone already agreed, or answers what only it could answer, or springs what no one saw coming. For the fourth, the filing is the editor. The fact already sits on the record, and the company chooses whether its own page confirms it, restates it, or passes over it. When the record already holds the fact, that choice reads as a judgment about what counts as material, made where anyone can watch it happen. Which bucket a fact lands in, in other words, is the filing’s decision, and the fourth exists because the company still has one to make about things everyone else has already disclosed.

The comparable we can see

Reading a document still to come is easier with one already in hand, from the nearest neighbor. OpenAI’s audited 2025 statement reached the public outside the SEC’s files, through Ed Zitron’s reporting, verified by the Financial Times; we treat it as reported, not filed. The headline figures, set out earlier in this series: revenue of $13.07 billion against costs of $34 billion, an operating loss of $20.92 billion, and a net loss of $60.4 billion. (1)

Two features of that statement are the template, and neither is a forecast about Anthropic. The first is the cost stack. About 81 percent of cost of revenue, and close to half of the entire $34 billion, was paid to Microsoft, which is at once OpenAI’s largest compute supplier and one of its investors. On this evidence a frontier lab’s income statement is dominated by payments to a company that also owns part of it. The second is the distance between the operating loss and the net loss, roughly forty billion dollars of charges below the operating line, the signature of remeasuring convertible and preferred instruments as their value moves. The investor’s gain is the issuer’s charge. Amazon reported a $12.3 billion increase in one quarter “primarily from our nonvoting preferred stock in Anthropic”; the mirror of that entry falls on Anthropic’s own statement. (2)

Those two features become two questions to carry into Anthropic’s filing: how much of its cost stack flows to its investors, and how large is the charge that turns an operating loss into a net one.

What the record already holds

The compute Anthropic buys is filed by the companies that sell it, and the sizing runs against intuition. The biggest arrangements are the ones that never appear as a line. Google’s cloud deal, reported at up to a million of its own chips and more than a gigawatt, and Amazon’s Trainium deal, reported near $100 billion, are the two largest, and each surfaces in its supplier’s filings only inside a total: Google’s cloud backlog in the hundreds of billions, Amazon’s “amended commercial arrangement.” (3)

The smaller arrangements are the ones with a name attached, because they sit on the counterparty’s own page. SpaceX’s prospectus records a cloud services agreement at $1.25 billion a month for capacity across two data-center clusters through May 2029, cancellable by either side on ninety days’ notice; the customer is Anthropic. (4) TeraWulf’s July filing records a twenty-year lease of roughly 401 megawatts at a Kentucky campus, delivered across 2027 and 2028. (5) A vehicle that bought Google’s chips and leases them back to Anthropic carries about $35 billion of debt, $29 billion of it guaranteed by Broadcom, spread across four other companies’ filings and set out earlier in this series. (6) And a multi-year deal reported at $6.8 billion with CoreWeave sits in a CoreWeave press release and in none of CoreWeave’s SEC filings. (7)

The capital Anthropic raises is filed by the companies that supply it. Amazon’s most recent quarterly report records $8.0 billion of convertible notes invested from 2023 to 2025, now converting to nonvoting preferred; a credit facility that opens as Amazon meets compute-delivery milestones and expires thirty months after an Anthropic public listing; and an option to invest up to $5.0 billion more. (2) Registered funds mark their Anthropic holdings every quarter: one closed-end fund carries its exposure at $134 million, about eighteen percent of its assets, held through a special-purpose vehicle, and a row of others, including funds built expressly to hold pre-listing shares, do the same. (8)

Not every appearance is a purchase or a stake. News Corporation’s quarterly report notes that a class action against Anthropic, in which its subsidiary HarperCollins is a class member, received preliminary approval for settlement, with proceeds receivable uncertain. (9) Even a liability Anthropic will pay shows up first on the books of those it will pay.

For each of these lines the S-1 poses the same question, and the question is never the number. We already have the number. What the filing will settle is whether Anthropic’s own document names the counterparty and carries the obligation, and where it does not, which threshold left it off the page. A lease of twenty years sits on a balance sheet as a liability or appears in a note as a commitment. A supplier that is also among the largest investors is a related party or the relationship is described another way. A customer that a public company does not name in its own filings either appears in Anthropic’s, or it does not. Every line we can already draw becomes a test of the line the company draws.

What the filing will tell us

Against that fourth bucket sits the second, the ordinary one: the questions a document answers because only the company holds them. The cost side of Anthropic is the best-lit part of it, because suppliers file. The revenue side is dimmer, not dark: Anthropic has said in its own voice, in the release for the Google and Broadcom partnership, that run-rate revenue has passed $30 billion, up from about $9 billion at the end of 2025, reported and not filed. (6) A run-rate in a release is a headline, though, not an audited line, and the S-1 supplies for the first time the figure and the choice that shapes it, whether revenue is recognized gross or net, and whether compute resold or hosted for others runs across the top line.

Darker than the total is its make-up. OpenAI’s reported statement at least showed a shape there, with about nine percent of revenue coming from two of its own investors. (1) Anthropic’s customers sit on no one’s page, and the accounting would let its filing carry a single customer at a tenth of sales without printing the name. Whether the S-1 names a concentrated customer, or reports it only as a percentage, is the judgment the customer line will pose.

The other open questions follow from the first. A gross margin, to read against the OpenAI ratio of a $20.92 billion operating loss on $13.07 billion of revenue. A cash burn, and the runway it leaves against a valuation reported near a trillion dollars. (10) And the size of the remeasurement charge below the operating line, the mirror of the marks the investors have already booked. These are answers only the filing holds. They are what a filing is for.

Where the judgments sit, and who makes them

Materiality is a judgment first and a disclosure second, the company’s own call about what a reasonable investor would find important. A private company has never had that call gathered in one place, or contested. Anthropic’s has instead been made piecemeal, by the companies around it, and they diverge. Amazon names Anthropic and quantifies its stake to the dollar. CoreWeave records a multi-billion-dollar agreement in a press release, and it does not appear in its filings. Broadcom guarantees $29 billion and identifies the beneficiary as “a customer.” Google places a commitment inside a backlog measured in the hundreds of billions and names no one. The same company is material to the dollar in one filing and unnamed in the next.

Most of these blanks can be read, and often from the filer’s own words. A filer will name a party in one document and anonymize it in another: Broadcom announced Anthropic by name, with Apollo and Blackstone, in the release for the chip financing, and wrote “a customer” into the 8-K. (6) The release is the filing’s answer key, and the gap between the two is a disclosure choice laid bare. The blank that resists this is a name a counterparty’s confidentiality keeps out of the filer’s own voice everywhere, release and filing alike, and that is the case to watch for rather than assume.

The auditor makes a judgment too, and the S-1 will rest on a full audit, conducted to public-company standards. That audit carries the first layer of the auditor’s judgment on its face: the footnotes, where each accounting policy is set out, and the fair-value hierarchy that sorts the instruments held and issued. For a frontier lab the hardest calls cluster where the quality-of-cash questions do, in the fair value of Level 3 instruments, the recognition of revenue, and the accounting for long-dated leases and for the vehicle that holds the chips. The sharpest layer, the critical audit matters that name what the auditor found hardest to test, arrives later. It attaches to the first annual report a public company files, not to the registration statement, so the S-1 can carry a complete audit and still not name a single critical audit matter. (14) The auditor’s judgment, like the company’s, reaches the record in stages: the footnotes now, the hardest areas named on the annual cycle that follows.

And the regulator makes the third judgment. The record already shows how the gathering gets tested. Weeks ago the staff read SpaceX’s draft, found a compute agreement the company had not filed as a material contract, and asked, on paper, what consideration it had given to filing it. The agreement was the one with Anthropic. (11) The same kind of review runs from Anthropic’s side when its own document posts.

Behind all three sits the drafting. A prospectus is written before it is read, and how it is written, what a page names and what it folds into a total, is a judgment the company makes with the banks that underwrite the offering and the counsel that drafts alongside them. That is the same choice we have been reading from the other direction on OpenAI. An income statement presents before it proves; how it groups a cost, what it names and what it folds into a subtotal, draws the line before any reader arrives. The drawing happens on both sides of the table.

A receivable, a fleet of machines, and a set of equity marks have each been graded on the quality-of-cash shelf by what must still happen for the dollar to become real. A frontier lab’s first audited statement is the next thing to grade, and much of the cost side is legible before it arrives.

The fourth does not thin. It sharpens. Every line the filing draws the way the others already drew it confirms what the record holds; every line it draws differently, or leaves blank, marks a place where a company valued near a trillion dollars, and named in nine hundred and ninety-nine filings it did not write, made a judgment about what to say.

So the document lands in a room already half furnished. Three of the four kinds of not-knowing thin as it posts: the known unknowns turn into numbers, and somewhere an unknown unknown appears that no outside reader could have named. The fourth does not thin. It sharpens. Every line the filing draws the way the others already drew it confirms what the record holds; every line it draws differently, or leaves blank, marks a place where a company valued near a trillion dollars, and named in nine hundred and ninety-nine filings it did not write, made a judgment about what to say. How much of that page do we already hold, and what will it choose not to say?

DISCLOSURE, standing: Anthropic is the developer of Claude, which is used in preparing this research, and is the subject of this piece. Amazon and Alphabet, named above, hold large positions in Anthropic; CoreWeave announced a multi-year agreement with Anthropic in April 2026; NVIDIA supplies the infrastructure providers that serve Anthropic. Figures are quoted from the filers without characterization, and the same standard of reading is applied to every filer named. This piece renders no view on Anthropic’s merits, prospects, or valuation; its subject is where the judgment of what must be disclosed sits, and how it is navigated.

Figures are verified against the primary filings and cited by accession; reported figures are labeled as such; our own counts are labeled as ours and sampled. The verification brief for this piece is written to be run by any reader against the cited accessions. Analysis: Cape Fear Advisors.

Cape Fear Advisors holds no position in any security named in this analysis and has received no compensation from any company discussed.

This analysis also appears on Substack.

Notes

(1) OpenAI’s audited 2025 figures are reported, not filed: Ed Zitron’s reporting on the audited statements, independently verified by the Financial Times (June 2026), and set out in “OpenAI, adding it up” (this series). Revenue $13.07 billion; total costs $34 billion; operating loss $20.92 billion; net loss $60.4 billion; approximately 81 percent of cost of revenue, and about half of total costs, paid to Microsoft. Approximately 9 percent of revenue came from two of its investors, Microsoft ($303 million) and SoftBank ($867 million).

(2) Amazon.com, Inc. Form 10-Q for the quarter ended March 31, 2026, accession 0001018724-26-000014: $8.0 billion of Anthropic convertible notes invested from Q3 2023 to Q4 2025, converting to nonvoting preferred; a Q1 2026 upward adjustment on private-company equity of $12.3 billion, “primarily from our nonvoting preferred stock in Anthropic”; a credit facility available to Anthropic as compute-delivery milestones are met, expiring 30 months after an Anthropic public listing, with draws in the form of convertible notes or, after a liquidity event, common stock; and an option to invest up to $5.0 billion in Anthropic’s future equity financings. The “amended commercial arrangement” referenced in the same note is the Trainium compute relationship.

(3) The Google and Amazon compute arrangements are reported: Google’s cloud and TPU expansion, reported at up to one million TPUs and more than one gigawatt worth tens of billions of dollars (CNBC, October 2025; Data Center Dynamics), and Amazon’s Trainium arrangement, reported near $100 billion. Both appear in the suppliers’ filings only inside aggregates: Google’s cloud remaining-performance-obligation backlog, and Amazon’s “amended commercial arrangement” and capital expenditure, neither naming a quantified Anthropic figure.

(4) Space Exploration Technologies Corp. Form S-1, accession 0001628280-26-036936: the Cloud Services Agreement, $1.25 billion per month for capacity across COLOSSUS and COLOSSUS II through May 2029, terminable by either party on 90 days’ notice.

(5) TeraWulf Inc. Form 8-K, July 6, 2026, accession 0001104659-26-080583: the Justified Data Campus Lease, a 20-year lease by subsidiary Raylan Data LLC of approximately 401 MW to Anthropic PBC at Hawesville, Kentucky, delivered late 2027 to early 2028.

(6) The approximately $35 billion chip-financing vehicle, with $29 billion guaranteed by Broadcom, is disclosed across Google, Broadcom, Apollo, and Athene filings and set out in “Anthropic, the financing before the filing” (July 6, 2026, this series). Broadcom’s Form 8-K identifies the beneficiary as “a customer,” while the financing announcement issued through Broadcom’s investor site, with Apollo and Blackstone, names Anthropic and states an initial $35 billion tranche; Anthropic’s own announcement of the expanded Google and Broadcom compute partnership names both counterparties. In each, the name sits in the company’s press release and not in the filed guarantee. The same Anthropic announcement reports run-rate revenue surpassing $30 billion, up from approximately $9 billion at the end of 2025 (reported).

(7) The CoreWeave multi-year compute agreement is reported at approximately $6.8 billion (CoreWeave press release, April 10, 2026; Forbes). A full-text search of CoreWeave’s 2026 SEC filings returns no mention of Anthropic.

(8) Destiny Tech100, Inc. Form NPORT-P, accession 0000894189-26-016628: “Magnitude ANC III, LLC (economic exposure to Anthropic PBC, Series B Preferred Shares),” carried at $134,092,223, 17.92 percent of the fund. Registered funds including Fidelity, T. Rowe Price, Coatue, Fundrise, and RiverNorth’s prime-unicorn funds also hold and mark Anthropic exposure through comparable vehicles.

(9) News Corporation Form 10-Q, accession 0001564708-26-000103: the note that a class action against Anthropic PBC, in which HarperCollins is a class member, received preliminary court approval for settlement in September 2025, with timing and amount of any proceeds receivable uncertain.

(10) Anthropic’s reported valuation of approximately $965 billion after its May 2026 round, and an offering reported for as soon as October 2026 led by Morgan Stanley, Goldman Sachs, and JPMorgan, are press reports (Bloomberg and others, July 16, 2026), labeled reported.

(11) SpaceX comment-letter correspondence, released on EDGAR July 13, 2026: the SEC staff’s letter of May 29, 2026 (UPLOAD, accession 0000000000-26-005505) notes the added disclosure that Anthropic will pay $1.25 billion per month across the two clusters and asks what consideration the company gave to filing the agreement, citing Item 601(b)(10).

(12) The count of 999 filings naming Anthropic is ours, from an EDGAR full-text search for “Anthropic” over January 1 to July 17, 2026, summed across monthly buckets and sampled across the range. The hits are overwhelmingly registered-fund holdings (Forms NPORT-EX and NPORT-P), fund prospectuses and shareholder reports (Forms 485 and N-CSR), private-placement Form Ds, and counterparty periodic reports, consistent with the company rather than the adjective. Anthropic, a private company, has no filings of its own.

(13) Anthropic’s confidential-submission announcement, posted to its website and its X account on June 1, 2026: “Anthropic has confidentially submitted a draft S-1 registration statement to the Securities and Exchange Commission. Pending completion of SEC review, this gives us the option to pursue an initial public offering.”

(14) The critical-audit-matter requirement is set by PCAOB Auditing Standard AS 3101, which the SEC approved in Release No. 34-81916 (October 23, 2017). A newly public company that is not an emerging growth company first communicates critical audit matters in the auditor’s report on its first annual report as a public company (Form 10-K); the auditor’s report on the financial statements included in an IPO registration statement does not carry them, though that audit is complete and conducted to PCAOB standards. Emerging-growth-company issuers are exempt from critical audit matters under the standard while they qualify. Footnote disclosures and the fair-value hierarchy are part of the audited statements included in the S-1.