A special-purpose vehicle has borrowed roughly $35 billion to buy Google’s chips and lease them to Anthropic, funding a hardware build-out that Anthropic’s growth requires. Because the vehicle owns the hardware, the borrowing sits on its books rather than Anthropic’s, an outcome of the structure the parties chose. Broadcom guarantees the debt, and its June quarterly report states the guarantee at a maximum of $29 billion, a figure the market reported as undisclosed. Anthropic has filed nothing public; the parties around it have, and their filings read together show the whole vehicle and a pattern of who must name it and who may stay silent. Anthropic’s own filing is expected around Labor Day, and the questions it can and cannot answer are worth having in view before it lands.

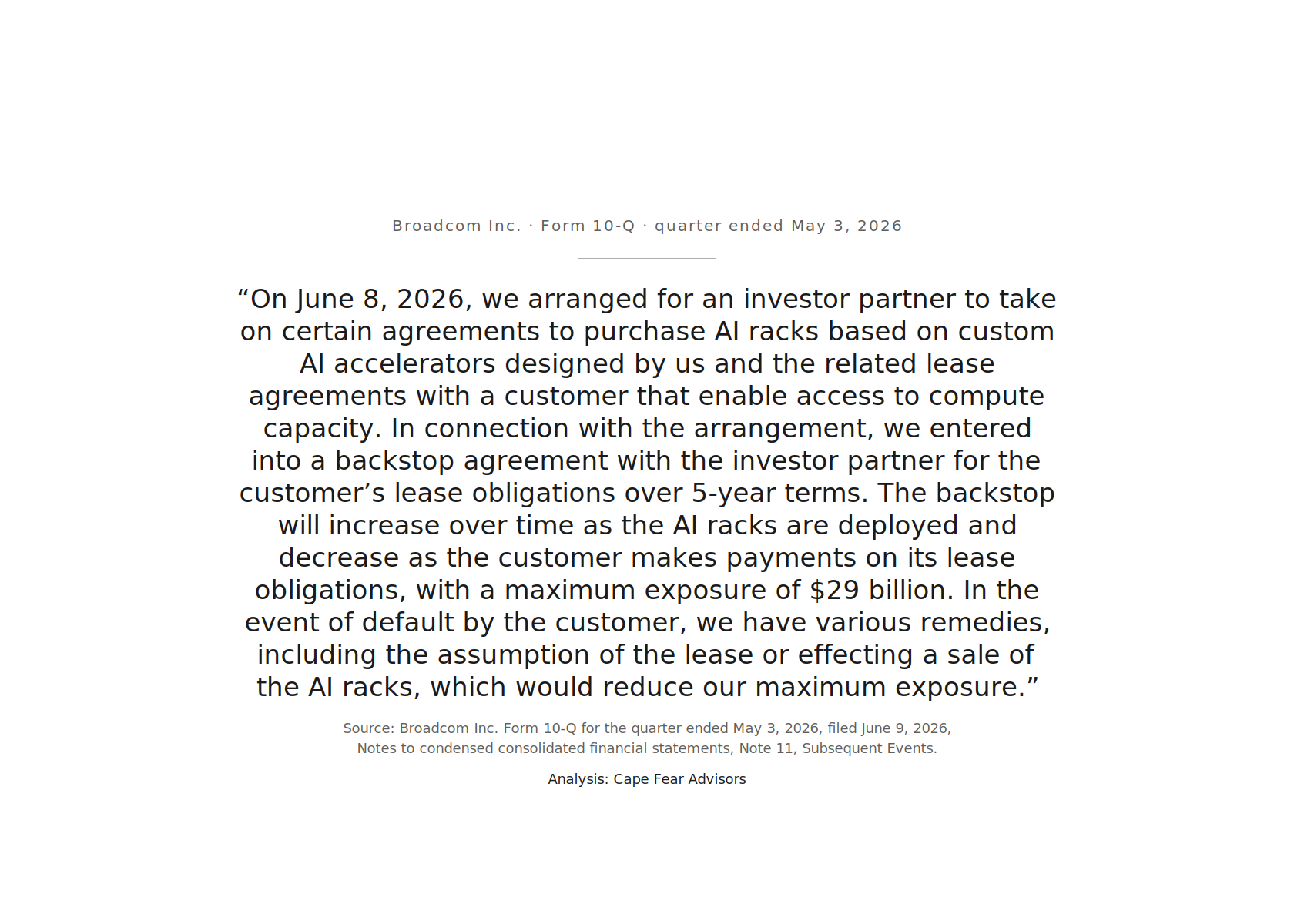

The deal is public and was carefully reported. Analysts and reporters had the vehicle, the roughly $35 billion, Google’s chips, Anthropic as lessee, and Broadcom’s backstop, which they sized at $30 to $31 billion from people familiar with the terms while noting that the exact cap stayed undisclosed. (1) That was a careful approximation, and it was close. We went to the filings to confirm it and came back with something firmer: not an estimate but the figure itself, filed. Broadcom’s June quarterly report states a maximum exposure of $29 billion, in the subsequent-events note above. The confirmation was in the document, for anyone who read it there.

The same holds for the customer’s name, which the coverage gave as Anthropic, and reasonably. The June note itself says only “a customer.” Broadcom’s April 8-K names Anthropic in the collaboration the note finances, the platform’s announcement names Anthropic as its lessee, and the full identification runs through those filings and the public reporting, laid out below, under “The parties who file.”

The vehicle owns the hardware and carries the borrowing, so the debt sits with the vehicle and the $29 billion sits on Broadcom’s guarantee, neither on Anthropic’s books. That placement follows from the structure the parties chose to fund the build-out, not from a decision to keep anything off a page. The structure has a reason, and the reason is worth granting before the piece reads how the arrangement discloses itself.

The need is real, and its size explains the structure. Anthropic is meeting demand for its services that requires expensive hardware to deliver, and the capital that hardware takes runs past what an emerging company reaches through equity and ordinary credit. That is why a vehicle like this exists: the size of the need shapes the solution.

Anthropic has said as much in its own voice. Announcing its Series H round in late May, the company recorded that it had signed agreements with Google and Broadcom for five gigawatts of next-generation TPU capacity, and its chief financial officer said the funding would “help us serve the historic demand we are experiencing.” The compute the vehicle finances, Anthropic named; the demand behind it, its finance chief stated. What Anthropic has not done is file. The financing that carries the compute onto its books, or keeps it off, is what a filing would show.

The need also carries a condition, and Broadcom filed it. In its April agreement, Broadcom records that consumption of the capacity is “dependent on Anthropic’s continued commercial success.” Broadcom, with $29 billion at stake, named in its own words what the need rests on. The dependency belongs to the record, and to the hand most exposed to it.

This piece takes both as given: the need, and the size that shapes the structure. It reads only how the arrangement discloses itself across the filings: where the exposure lands, who must name it, and who may stay silent.

The parties who file

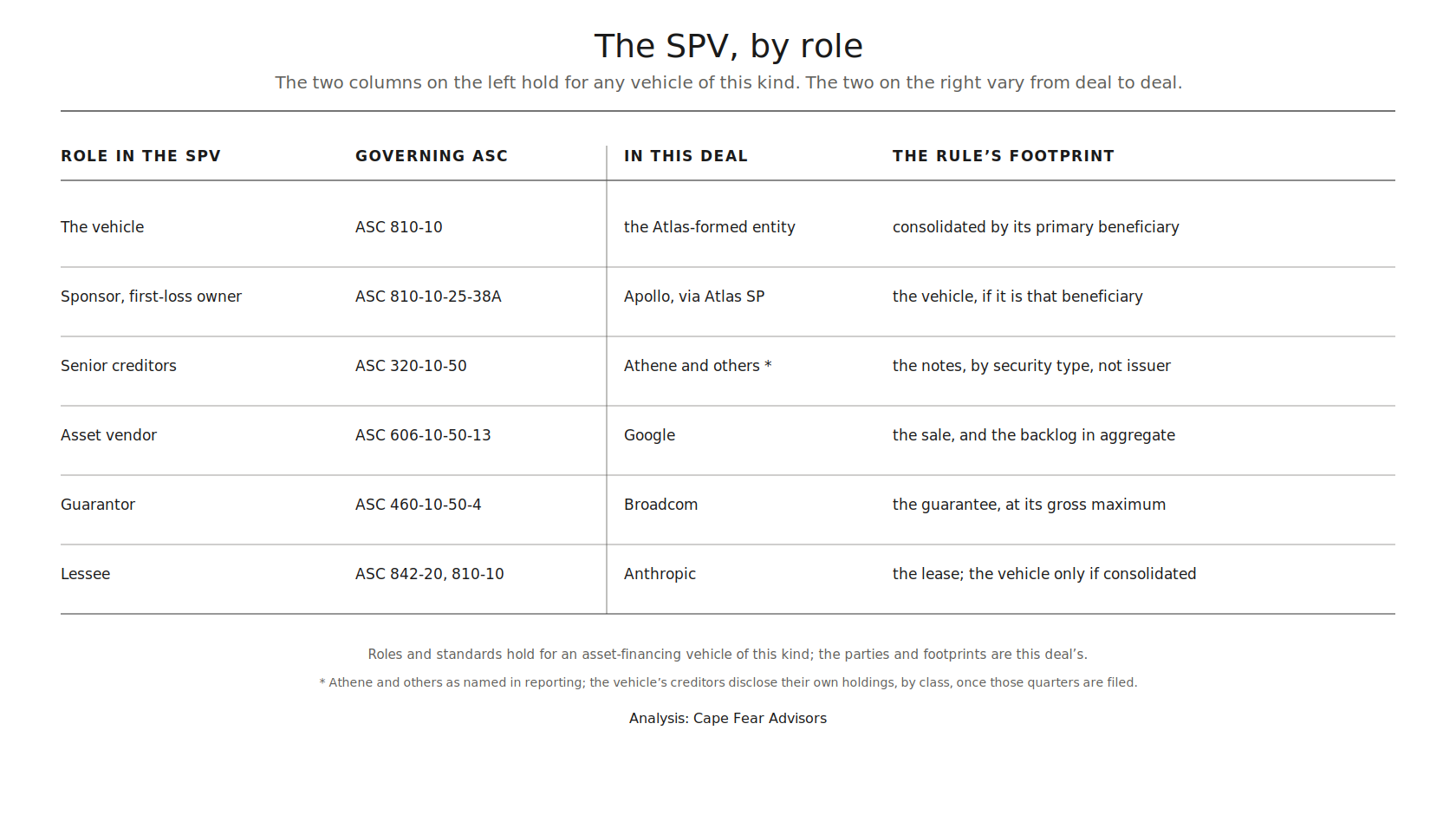

The vehicle is a special-purpose entity, the kind US GAAP treats as a variable interest entity: single-purpose, thinly capitalized, its control and its risk parceled among the parties by contract. Entities like it are among the most closely governed in the accounting standards. One set of rules decides whose balance sheet the vehicle sits on. (2) A separate set decides who discloses which interest, by the nature of the interest held. Both are detailed, both are settled, and here both are followed. Each party discloses what its rules require.

The rules produce disclosure spread across companies, because the arrangement is spread across companies. Broadcom guarantees the debt, Google supplies the chips and holds a stake in Anthropic, Apollo lends and holds, and Anthropic leases. Each files its own interest, in its own report, correctly. The vehicle becomes legible by assembling those filings, because the vehicle is assembled from those parties. Reading it takes several filings at several companies for the plain reason that the arrangement is several companies. The spread of the disclosure is the shape of the deal, faithfully reported.

The question this section asks is narrow, and it rests on top of a standard correctly applied: as the relationship crosses each company’s books, where does the name go, and where does the number?

The cast holds for any vehicle of this kind. An asset-financing vehicle like this has a fixed set of seats, because it solves a fixed problem: raise capital, buy an asset, lease it to the party that needs it, enhance the credit so the debt prices. Each seat carries its own standard, because the standard attaches to the nature of the interest, and the seat is the interest. The role names the standard.

Two of the exhibit’s columns hold for any vehicle of this type, and two vary: the role and its standard are fixed, while who sits in the seat and what they have filed change from deal to deal.

Several parties hold more than one seat. Google sells the chips and holds a stake in Anthropic. Broadcom designs the chips and guarantees the debt. Apollo sponsors the vehicle, holds its first loss, and buys its senior notes. The disclosure spreads across filings, and within a filing across notes, because a single company sits in several seats, each seat under its own standard.

The deal is public. Anthropic announced the five gigawatts of Google and Broadcom TPU capacity in its own words, and Apollo, Blackstone, and Broadcom announced the financing platform with Anthropic as its first lessee. The names are on the record.

The filings use other words for them. Broadcom’s June note calls Anthropic “a customer” and Apollo “an investor partner.” Item 5 of the same report names Apollo, the partner April’s 8-K had left “in discussions,” and still calls Anthropic “a customer.” Broadcom’s April 8-K names Anthropic plainly, “Broadcom, Google, and Anthropic PBC,” with 3.5 gigawatts of TPU compute through Broadcom, and turns to “certain operational and financial partners” at the financing. Broadcom names Anthropic at the compute and writes “a customer” at the financing, in both filings.

The identification is that simple: the customer Broadcom’s note describes, by its Broadcom-designed racks and five-year leases, is the Anthropic the announcements named. The finding is the gap. Where the announcement says Anthropic, the filing says “a customer,” and it says so at the financing, where the rules would let it write the name. Perhaps an agreement seals it; perhaps it is the ordinary practice of a filing that writes “a customer” even when the market knows who, the way CoreWeave’s filings write “Customer A” for its largest customer. The gap is on the record; the reason for it is not.

The other seats set what reaches the page in different ways. Some rules compel a number; others let a position fold into a total. Google folds: a rule lets it aggregate the sale and the stake, so the backlog carries Anthropic’s commitment under ASC 606 (3) and the mark carries the stake under ASC 321, (4) each inside a total, the positions small against Google’s results. Apollo’s insurer and asset manager report their holdings by class under ASC 320 (5) once the quarter that captures them is filed, Anthropic inside a security type. Anthropic holds the lease and, for now, files nothing public, its registration confidential and no trigger yet reached.

So Anthropic’s name reaches the page where a rule compels it, and folds into a total where a rule permits. At the financing it becomes “a customer,” where the rule would allow the name and something outside the rule holds it back.

One seat shows the materiality force by itself. The owner of the lessee holds non-marketable equity in Anthropic, marked under ASC 321. Google fills it at roughly fourteen percent and aggregates, the mark folded into other income, because at Google’s scale the position is immaterial and the rule lets the total stand unattributed. A registered fund, Destiny Tech100, fills the same seat at $100 million and names it in full, Anthropic PBC, in a prospectus supplement, because at the fund’s scale the same position is material and the rule requires the name. (6) Same seat, same standard, opposite ends of the scale, opposite disclosures. Here only materiality is at work, which makes it the clean case: the threshold moves with the filer, and the smaller holder states the name the larger folds away. What the record discloses tracks materiality to the filer, and runs opposite to size in the world.

The cash, in two parts

The money moves in two directions on two clocks.

One part is certain and moves now. The debt and the equity fund the vehicle, and the vehicle buys the chips. Reporting puts the debt near $35 billion across three tranches and the first-loss equity near $800 million, at coupons reporting also supplies. Those figures are reported rather than filed; they come from the parties describing the deal, not from a document any party has signed and submitted. What they describe is a single, upfront use of capital: the vehicle takes the borrowed money and the equity and pays Google for the hardware. That leg closes at the start and stands on its own.

The other part is contingent and arrives over time. Anthropic leases the chips and pays across five years, and those payments service the debt. The stream is future, and it carries the condition Broadcom filed: it depends on Anthropic’s continued commercial success. Behind the stream stands Broadcom’s backstop, which the same filing sizes at $29 billion and describes as growing while the racks deploy and shrinking as Anthropic pays. The contingent leg is where the structure lives, because it is the leg that can vary.

With the reported figures set aside, two numbers about this arrangement are filed rather than reported, and both describe the future. Broadcom’s $29 billion is the contingent ceiling on the backstop, gross, as its standard requires. Google’s $462.3 billion is the aggregate of Google Cloud revenue under contract and not yet earned, Anthropic’s share among it, as its standard requires. Google’s finance chief attributed the backlog’s near-doubling in part to TPU hardware sales, and told analysts that the TPU hardware agreements “are reflected in our cloud backlog,” the same $462.3 billion; the seller places this class of arrangement inside the number, an aggregate that names no one. The money that has already changed hands reaches the record only as reported. The two filed numbers both point forward: one a ceiling on a guarantee, one a backlog of revenue, each a measure of what has yet to happen.

The exposures

The $29 billion is a ceiling, and it is gross, because ASC 460 requires a guarantor to state the maximum it could pay before any recovery. (7) Broadcom filed the trigger and the remedies alongside it: the backstop is called if Anthropic defaults, and Broadcom’s remedies then, assuming the lease or selling the racks, would reduce the maximum exposure. Three parts of the exposure are filed, then, the ceiling, the trigger, and the remedies Broadcom says would reduce it, and one part is not: what those remedies would actually recover.

That recovery rests on a resale value no filing in the structure supplies, and it is the same value the CoreWeave reading turned on. What a specialized chip fetches after a lease has run and the market has moved is the quality of the asset behind the cash. Here the asset stands behind a guarantee rather than a balance sheet, and the question holds its shape: the exposure is only as covered as the collateral is worth, and the collateral is a used accelerator whose secondhand price stands outside every filing.

This is terrain Rod Dubitsky has been reading, (8) and further than we can reach from EDGAR. His forensic work on Athene’s statutory filings takes Athene’s book apart below the level the GAAP reports show: where we stop at ASC 320’s disclosure by security type, he reads the holdings themselves. On the residual-value question, and on how the rating agencies weigh a guarantee against the guarantor that gives it, his work goes where ours does not, and we point readers to it.

The net, the amount Broadcom would truly carry, is the filed ceiling less a recovery the record describes and does not size. And the condition beneath the whole arrangement, Broadcom filed as well: consumption of the compute, its April agreement records, is “dependent on Anthropic’s continued commercial success.”

The standard, and the page

Every party followed every rule. The vehicle stands disclosed, the guarantee filed at its gross maximum, the backlog aggregated as the standard directs, the stake marked where the standard places it. Each seat met its obligation, and the framework the FASB built for exactly these structures did what it was written to do. Their compliance is the finding, and it carries weight.

The sum of that compliance is a $35 billion financing that reaches the public record in pieces, held by the parties around the vehicle, on pages that belong to them. The number at the center, the $29 billion, reaches the record because Broadcom was required to state it, in Broadcom’s filing, under the label “a customer.” Reconstructing the vehicle took a reading across several filings at several companies, because the arrangement spreads across several companies and the disclosure spreads with it. That reading was the only route to the number, and it returned more than the number. It tightened a widely-held assumption into a filed fact, and it traced a pattern that outlasts this deal: a name placed where a rule compels it, folded into a total where a rule permits, and set aside for “a customer” at the financing, until the party every exposure in the structure runs back to is the one the filings name least.

The question the piece leaves begins where compliance ends. It asks whether a standard can be fully satisfied and still keep the financing behind a commitment of this size off Anthropic’s own page, legible only through the others.

The counterparties file again through the summer, and each report can add a line: Athene’s holdings by class, Apollo’s consolidation, Google’s next mark and its backlog. Anthropic’s own filing is expected around Labor Day, later than once thought and open to change, and it is the one that can answer the balance-sheet question. It can show whether Anthropic consolidates the vehicle or holds it apart, whether the lease appears as a right-of-use asset while the debt stays with the vehicle, (9) and whether the $29 billion Broadcom disclosed appears at last under Anthropic’s own name. It cannot fix what the hardware will fetch secondhand, or whether the demand the structure rests on holds, or where the net exposure behind the gross ceiling finally sits; those wait on the market, not the page. And it can decline the question altogether, aggregating the vehicle the way the counterparties aggregate the stake and the backlog, and leave the pieces where they lie.

The standard has been satisfied. The page is still to come.

Notes

(1) The trade coverage that carried the deal sized Broadcom’s backstop from unnamed sources and flagged the cap itself as unknown. AI Weekly, “Apollo Backs $36B Record Debt Deal for Anthropic TPUs,” May 30, 2026, stated that “Broadcom’s residual-value guarantee cap is undisclosed”; OpenTools reported the same, that the guarantee cap “is also not public.”

(2) ASC 810-10 governs consolidation of a variable interest entity. The party that both directs the activities most significant to the entity’s economic performance and bears the obligation to absorb its losses or the right to its benefits (ASC 810-10-25-38A) is the primary beneficiary, and consolidates it. Every other holder of a variable interest discloses that interest under ASC 810-10-50 without consolidating. The test decides which balance sheet the vehicle sits on; when Anthropic files, its treatment of the vehicle under this test is the line to read.

(3) ASC 606-10-50-13 requires disclosure of the aggregate transaction price allocated to performance obligations not yet satisfied, with an explanation of when it will be recognized. The standard asks for the aggregate, not the customers. Anthropic’s commitment sits inside Google’s Google Cloud remaining performance obligations as one contract among many, disclosed in total and without names.

(4) For an equity holding without a readily determinable fair value, ASC 321-10-35-2 permits the measurement alternative: cost less impairment, remeasured to fair value when an observable price change occurs in an orderly transaction for the same issuer. A new Anthropic funding round is such a transaction. The holder marks its stake to the round and records the change in earnings, in other income, where the standard places it and where the issuer goes unnamed.

(5) A creditor holding the vehicle’s senior notes discloses them under ASC 320-10-50 by major security type, defined by the security’s nature and risk (ASC 320-10-50-1B), rather than by issuer. The holdings reach the record inside a class, not under the borrower’s name.

(6) Materiality is judged relative to the reporting entity and its investors, not in absolute dollars. The SEC staff’s SAB No. 99 (codified at ASC 250-10-S99) frames significance against a particular registrant’s statements and the total mix of information a reasonable investor in that entity would weigh, and the FASB locates the same judgment with those who understand the entity’s own circumstances. A $100 million position significant to a small fund, named in its schedule of investments, can sit inside an aggregate line for a company whose results run in the tens of billions.

(7) ASC 460-10-50-4 requires a guarantor to disclose the maximum potential amount of future payments it could be required to make, undiscounted, and before reduction for any recoveries under recourse or collateral provisions. Broadcom’s $29 billion is that figure, gross. The remedies listed in the same note, assuming the lease or selling the racks, are the recoveries the standard holds separate from the ceiling.

(8) Rod Dubitsky writes forensic analysis of Athene’s statutory filings and the structures around them at roddubitsky.substack.com, including “Inside Athene’s Nesting Dolls” and the “Dangers Lurking” series. The residual-value and rating-agency observations this section points to are his.

(9) For the lessee, ASC 842-20-25-1 places a right-of-use asset and a lease liability on the balance sheet at the present value of the lease payments. The vehicle’s own debt follows onto the lessee’s books only if the consolidation test in ASC 810 makes the lessee the primary beneficiary.

On Tools and Conflict

This analysis was drafted and pressure-tested with AI tools, including a model built by Anthropic, the company this piece examines. No tool removes that conflict; another model would only trade it for its own. The bias a tool cannot eliminate has three answers, and the piece uses all three. It avoids the judgment call where the record allows, resting its claims on filings and accounting standards a reader can check without trusting the tools or the author. It tests against the bias rather than around it. And in the end it rests on the author, who holds the judgment that remains and the responsibility for it.

Structural disclosure analysis of a special-purpose vehicle financing Anthropic’s Google-TPU build-out. Sources: Broadcom Inc. Form 10-Q for the quarter ended May 3, 2026, filed June 9, 2026 (Note 11, Subsequent Events); Broadcom Inc. Form 8-K, April 16, 2026; Alphabet Inc. Form 10-Q for the quarter ended March 31, 2026; Apollo Global Management, Inc. press releases. Figures verified against the primary filings. Analysis: Cape Fear Advisors.

Greg Collins serves as CEO of C3 Metrics, a marketing measurement and analytics firm, and maintains an advisory practice at Cape Fear Advisors focused on structural analysis and strategy.

The author holds no direct position in any security discussed. Whatever indirect exposure comes through index and managed funds is neither known to him nor, he suspects, escapable.

This article is also available on Substack.

Start a Conversation →