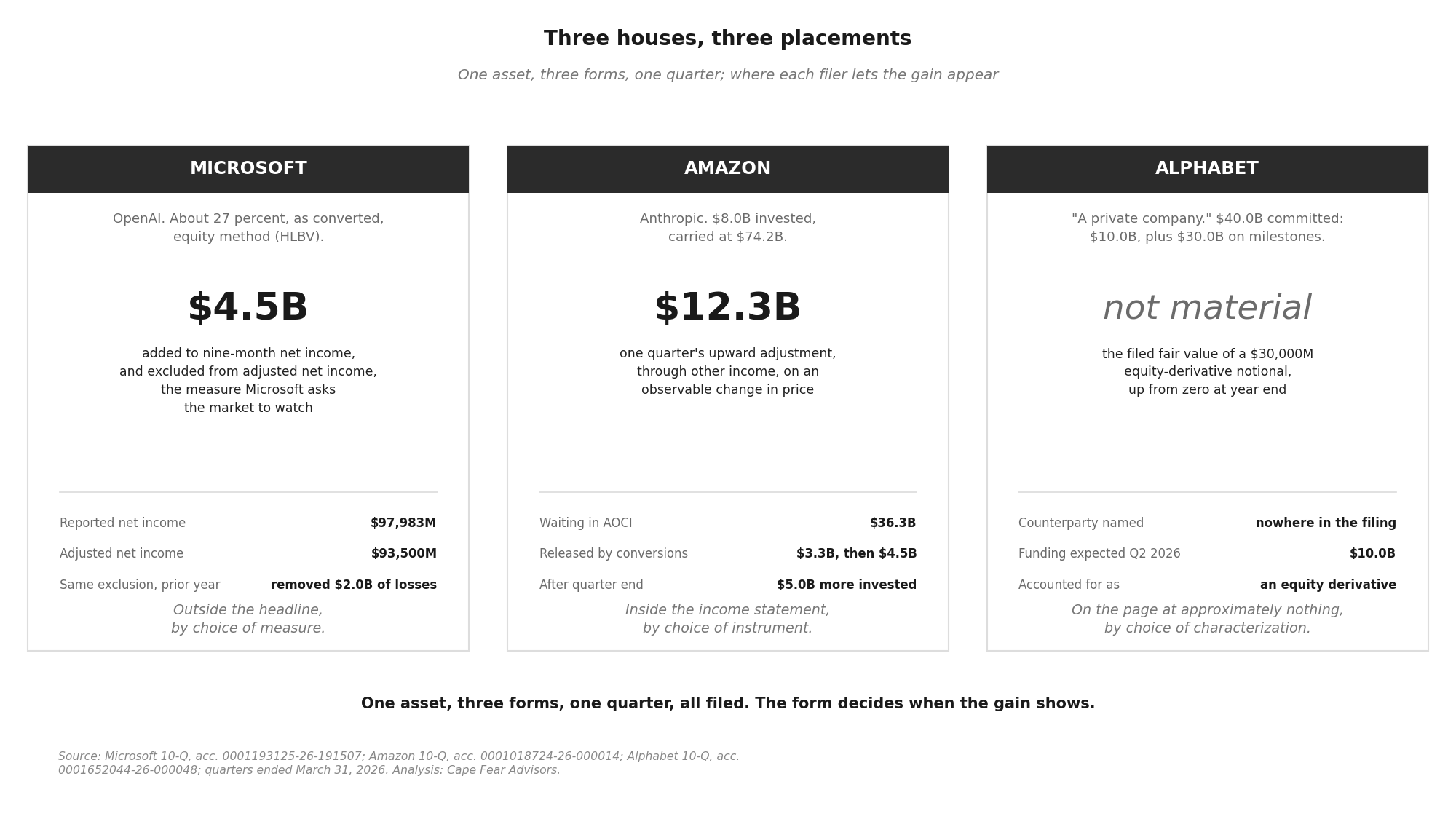

Three companies hold large positions in the two frontier AI laboratories, and in the quarter ended March 31, 2026, all three filed what those positions did. Microsoft’s stake in OpenAI added roughly $4.5 billion to nine-month net income, and the earnings measure Microsoft asks the market to watch removes it. Amazon’s $8.0 billion of Anthropic paper is carried at roughly $74.2 billion; a single observable change in price ran $12.3 billion through one quarter’s income, and $36.3 billion more sits in a comprehensive-income account, waiting for a conversion to release it. Alphabet committed $40.0 billion to a company its filings do not name, accounted for as an equity derivative whose fair value it calls not material. One asset, one quarter, three forms of holding it, and three placements: outside the headline by choice of measure, inside income by choice of instrument, on the page at approximately nothing by choice of characterization. Each is correct. Each was chosen by the house with the cash to make the choice.

One asset, three forms

The asset is a position in a private frontier AI laboratory. Two laboratories matter here, OpenAI and Anthropic, and three public companies carried positions in them through the first calendar quarter of 2026: Microsoft in OpenAI; Amazon in Anthropic and, as of this quarter, OpenAI; Alphabet in a company its filings call “a private company” and “a certain strategic investment.” The three filers are the largest sellers of the compute the laboratories buy, a relationship each discloses in its own way and none of them prices here.

The three forms differ in more than accounting. A stake carries rights a note does not; a note carries seniority the preferred does not; a commitment is not yet a position at all. The reading here is narrower: whatever else a form determines, it also decides where, in each set of financial statements, the position and its gain are permitted to appear. That consequence is the subject.

Everything below is quoted from the filers’ own quarterly reports for the period ended March 31, 2026, and every figure is filed unless marked otherwise. (1)

Microsoft: removed by choice of measure

Microsoft holds approximately 27 percent of OpenAI on an as-converted basis, accounted for under the equity method. The mechanics are unusual enough that the filing explains them: income or loss is computed under the hypothetical liquidation at book value method, “because our liquidation rights and priorities differ from our underlying ownership interest.” Microsoft recognizes income based on the change in what it would receive if OpenAI’s net assets were distributed at book value. The commitment stands at $13 billion, of which $11.8 billion has been funded. (2)

In October 2025, OpenAI recapitalized into a public benefit corporation. Microsoft’s proportionate ownership went down, and a dilution gain went through other income: $5.9 billion of net gains from the OpenAI position in the nine months ended March 31, 2026, lifting net income by $4.5 billion after tax and diluted earnings per share by $0.60. Reported nine-month net income: $97,983 million.

Then the placement. Microsoft’s own non-GAAP measure, adjusted net income, is defined by a single exclusion: it “exclude[s] net gains and losses from investments in OpenAI.” Adjusted nine-month net income: $93,500 million. The position added four and a half billion dollars to the number GAAP produces, and the number Microsoft promotes removes it.

The measure is symmetric. A year earlier the same line ran the other way: the nine months ended March 31, 2025 carried roughly $2.0 billion of OpenAI losses, and adjusted net income was higher than reported. The measure removed losses then and removes gains now. Microsoft has built a wall, in both directions, between the laboratory and the earnings figure it asks the market to watch: whatever OpenAI does to the income statement, the headline is defined so that it does not move. (3)

Amazon: delivered by choice of instrument

Amazon invested $8.0 billion in Anthropic convertible notes between the third quarter of 2023 and the fourth quarter of 2025. The notes are classified as available-for-sale, reported at fair value as Level 3 assets, and their unrealized gains rest in accumulated other comprehensive income, a balance-sheet account that touches the income statement only when something happens.

Things have been happening. In the first quarters of 2025 and 2026, portions of the notes converted to nonvoting preferred stock, and the conversions reclassified $3.3 billion and $4.5 billion of parked gains into “Other income (expense), net.” In the first quarter of 2026, Amazon also recorded “an upward adjustment of approximately $12.3 billion to our nonvoting preferred stock in ‘Other income (expense), net’ to reflect observable changes in price.” The quarter’s net other-income gain, $15.6 billion, is by the company’s own description primarily Anthropic. (4)

The carrying values, against the basis: the notes stood at approximately $42.2 billion at March 31, 2026, the nonvoting preferred at approximately $32.0 billion. Call it $74.2 billion of carrying value against $8.0 billion invested. The unrealized gain still parked in accumulated other comprehensive income, after the reclassifications: $36.3 billion. That is the reservoir. Each future conversion or liquidity event moves some of it from the parking account into income.

The position is still growing. Subsequent to quarter end, Amazon invested a further $5.0 billion in Anthropic nonvoting preferred, amended its commercial arrangement covering AWS cloud services and the performance of AWS chips, and made available to Anthropic a financing facility of up to $20.0 billion, expiring thirty months after a liquidity event such as an initial public offering, with an option to invest up to $5.0 billion more in future equity financings. (5)

And this quarter the second laboratory arrived on the same balance sheet. Amazon invested $15.0 billion in OpenAI Series C preferred and signed a commitment letter for a further $35.0 billion, an obligation that becomes mandatory upon the earlier of specified milestones or a public listing, and terminates if unspent by the end of 2028. Amazon’s carrying value in equity investments in private companies went from $16.2 billion to $48.1 billion in ninety days. (6)

Amazon’s laboratory gains run through the income statement, twelve billion dollars in a quarter when a price is observed, three to four billion at a time when notes convert, with a thirty-six billion dollar reservoir queued behind them. Available-for-sale accounting and the measurement alternative for private stakes are standard. The instrument chose the placement, and the placement puts the laboratory inside the earnings the market reads.

Alphabet: not material

Alphabet’s first-quarter derivatives table carries a line that did not exist at year end. Equity derivatives, gross notional: zero at December 31, 2025; $30,000 million at March 31, 2026. The note explains: “The notional amounts for equity derivatives represent an agreement for future capital funding in the form of notes receivable or equity to be funded in multiple tranches contingent upon the achievement of specified operational and financial milestones through 2030. The fair value of these equity derivatives was not material as of March 31, 2026.” (7)

The commitments note gives the full shape: “a $40.0 billion investment in a private company consisting of a $10.0 billion capital commitment and $30.0 billion of future capital funding contingent upon the achievement of specified operational and financial milestones through 2030, which is accounted for as an equity derivative. We expect to fund $10.0 billion in the second quarter of 2026 in the form of a non-marketable security.” Alphabet’s total future funding commitments moved from $1.1 billion to $40.7 billion in the same ninety days. (8)

What the filing does not carry is a name. The counterparty is “a private company,” “a future private investment,” “a certain strategic investment.” A full-text search of the quarterly report returns zero instances of Anthropic and zero of OpenAI. The identification of the counterparty as Anthropic is reported and inferred, not filed: press reporting placed Alphabet’s planned Anthropic investment at $40 billion in the same weeks, court documents put Alphabet’s existing ownership near 14 percent, and the filed structure matches the reported one. The inference is strong, and Alphabet’s own paper is the reason it must remain one. (9)

Microsoft’s laboratory position produces income the company then excludes, visibly, with a reconciliation table. Amazon’s produces income the company reports, at billions per quarter. Alphabet’s produces, so far, a notional amount in a table and a fair value described as not material. A $40.0 billion commitment to the most consequential private company in its orbit enters the record as a derivative worth approximately nothing, held against a counterparty with no name. At inception a derivative’s fair value can sit near zero, and the funding has not yet flowed. The visibility is the consequence.

“A $40.0 billion commitment to the most consequential private company in its orbit enters the record as a derivative worth approximately nothing, held against a counterparty with no name.”

Readers of the backstop work will recognize the move, because it sits one row away in the same table. Alphabet’s data-center lease backstops are accounted for as credit derivatives: $28.4 billion of gross notional at March 31, 2026, carried at $339 million of fair value. Its energy-infrastructure backstops, in the same filing, sit under the financial-guarantees caption, with the “maximum potential amount of future payments” stated: $9.0 billion. Same filer, same quarter, and the characterization decides what a reader can see. (10)

The counterexample is filed by another house entirely. On June 8, Broadcom arranged for an investor partner to take on agreements to purchase AI racks Broadcom designed, and the leases of those racks to a customer, and then backstopped the customer’s lease obligations itself: “a backstop agreement with the investor partner for the customer’s lease obligations over 5-year terms,” rising as racks deploy, falling as the customer pays, “with a maximum exposure of $29 billion.” The remedies are stated: assume the lease, or sell the racks. Neither the customer nor the investor partner is named. The names stayed out of Broadcom’s report too. The number could not. A capped backstop is a different instrument from a credit derivative, and part of the gap between the two disclosures is the difference between the two things. Grant that fully and set the pages side by side anyway. Broadcom stands behind a stated maximum of $29 billion of AI-lease obligations. Alphabet’s data-center lease backstops carry $28.4 billion of notional, a figure its own note defines as the maximum potential amount of future payments. Nearly the same exposure, two forms: one page carries the maximum, the other carries $339 million of fair value. (11)

The fork, transposed

Set the three placements side by side, as of the same ninety days:

Microsoft: the gain is in net income, and the promoted measure removes it. A reader of the adjusted number sees no laboratory at all, by symmetric design.

Amazon: the gain is in net income, $12.3 billion of it in one quarter on an observable price, with $36.3 billion staged in an equity account for future quarters. A reader of the headline sees the laboratory every time something happens, and something has happened three quarters running.

Alphabet: the gain, if there is one, is nowhere. A $40.0 billion commitment is a notional in a footnote at a fair value not material, and the counterparty is unnamed. A reader of the headline sees nothing, and a reader of the footnotes sees a shape without a face.

The instrument decides for Amazon. The measure decides for Microsoft. The characterization decides for Alphabet. What a shareholder in each company knows about the same asset, in the same quarter, from the same class of document, differs by an order of magnitude, and in Alphabet’s case by the presence or absence of the asset itself.

The gains are marks on private shares, and the marks move on observable prices, which for a private company means financings. Amazon’s $12.3 billion adjustment reflects observable changes in price, and after quarter end Amazon invested $5.0 billion more. Alphabet expects to fund $10.0 billion in the second quarter. The same houses that carry the marks are buyers in the rounds where private prices are set. Every one of those facts is filed by the house that carries it.

The question

The laboratories are private. Their prices are set in rounds, and the rounds are funded in large part by the three houses above. Three pieces of paper carry the positions, and none of them was dealt. Each house chose its card when it sat down to play, and each card shows only when the rules written on it require. An equity-method stake shows every quarter, and Microsoft publishes a second number that does not. A note shows when it converts or when a price is observed, so Amazon’s quarter carried sixteen billion. A derivative shows when its fair value turns material, a threshold the funding schedule has not yet crossed.

“Each house chose its card when it sat down to play, and each card shows only when the rules written on it require.”

The quality of cash entered this series as a question about a backlog: how much of a number still to come is already backed by cash, and how much is expectation. The three houses answer it from the other side of the table, because their future cash requires no such test. Alphabet’s $30.0 billion is contingent and unfunded, and it has already bought a characterization. Amazon’s $35.0 billion is a commitment letter, and it is already mandatory upon a milestone. At this end of the ladder the quality of cash is a currency in itself: the forms above were not bought with cash that moved. They were bought with cash that could.

When the same asset, in the same quarter, can add four and a half billion to one company’s earnings and be removed, add sixteen billion to another’s and be kept, and rest at approximately zero on a third’s, what does a reader hold who holds the headline number? And when the next round prices, whose number will it appear in, whose number will it be defined out of, and whose page will it never reach? Each house answered before the gain existed, when it chose its card. The answers are in the paper, and so are the next ones.

Cape Fear Advisors holds no position in any company named above and has no commercial relationship with any filer cited. This is structural observation, not investment advice.

DISCLOSURE, standing: Anthropic is the developer of Claude, which is used in preparing this research. Amazon and Alphabet hold large positions in Anthropic. Figures above are quoted from the filers without characterization, and the same standard of reading is applied to every filer named.

Figures are verified against the primary filings; quarterly reports are cited by accession number. Analysis: Cape Fear Advisors.

This piece was originally published on Substack on July 11, 2026.

Notes

(1) Microsoft Corporation Form 10-Q for the quarter ended March 31, 2026, accession 0001193125-26-191507 (fiscal third quarter). Amazon.com, Inc. Form 10-Q for the quarter ended March 31, 2026, accession 0001018724-26-000014. Alphabet Inc. Form 10-Q for the quarter ended March 31, 2026, accession 0001652044-26-000048. All figures in this note derive from these three filings except where marked reported or inferred.

(2) Microsoft 10-Q, Note 1, Investments: “We have an investment of approximately 27 percent of OpenAI on an as-converted basis accounted for under the equity method of accounting… We calculate our equity method income or loss using the hypothetical liquidation at book value (‘HLBV’) method because our liquidation rights and priorities differ from our underlying ownership interest… We have made total funding commitments of $13 billion, of which $11.8 billion has been funded as of March 31, 2026.” The October 2025 recapitalization and dilution gain per the same note and Note 3.

(3) Microsoft 10-Q, MD&A and Non-GAAP Financial Measures: “These non-GAAP financial measures exclude net gains and losses from investments in OpenAI.” Reconciliation table, nine months ended March 31: net income $97,983 million (2026) and $74,599 million (2025); net (gains) losses from investments in OpenAI, net of tax, $(4,483) million (2026) and $2,045 million (2025); adjusted net income $93,500 million (2026) and $76,644 million (2025). MD&A: nine-month other income included $5.9 billion of net gains from investments in OpenAI, primarily the dilution gain from the OpenAI recapitalization, increasing net income by $4.5 billion and diluted EPS by $0.60.

(4) Amazon 10-Q, Note on investments: “From Q3 2023 to Q4 2025, we invested $8.0 billion in convertible notes from Anthropic, which are classified as available-for-sale and reported at fair value… and as Level 3 assets… a gain of approximately $3.3 billion and $4.5 billion was recorded in ‘Other income (expense), net’ [on the Q1 2025 and Q1 2026 conversions]. In Q1 2026, we also recorded an upward adjustment of approximately $12.3 billion to our nonvoting preferred stock in ‘Other income (expense), net’ to reflect observable changes in price.” MD&A: “The net gain of $15.6 billion in Q1 2026 is primarily from an upward adjustment for observable changes in price relating to our nonvoting preferred stock in Anthropic and the reclassification adjustment for the gains on available-for-sale debt securities.” Derivation of the $74.2 billion: the notes ($42.2 billion) are an available-for-sale debt line; the nonvoting preferred ($32.0 billion) sits within “equity investments in private companies not accounted for under the equity-method” ($48.1 billion at March 31, 2026, which the filing states relates primarily to the Anthropic preferred and the OpenAI preferred, $15.0 billion). Converted paper is recorded in the equity line at conversion-date fair value and simultaneously leaves the notes line, so no portion of the position appears in both lines; $42.2 billion plus $32.0 billion states the whole Anthropic position once.

(5) Amazon 10-Q, subsequent events: the $5.0 billion further investment; the amended commercial arrangement, “primarily for the provision of AWS cloud services,” including “contractual obligations related to the performance of AWS chips”; the financing facility “not to exceed $20.0 billion that will expire 30 months after a liquidity event, as defined, such as an Anthropic initial public offering or direct listing”; and the option to invest up to $5.0 billion in future equity financings.

(6) Amazon 10-Q: “In Q1 2026, we invested $15.0 billion in Series C Preferred Stock of OpenAI, and we also entered into an equity commitment letter agreement… to purchase additional shares of Series C Preferred Stock… with an aggregate purchase price of $35.0 billion… we are obligated to purchase all remaining Commitment Shares upon the earlier to occur of (i) OpenAI meeting specified milestones, and (ii) OpenAI directly or indirectly consummating an initial public offering or direct listing… The parties’ obligations under the Letter Agreement will terminate if we have not invested the Commitment Amount by December 31, 2028.” Private-company equity carrying values of $16.2 billion and $48.1 billion at December 31, 2025 and March 31, 2026, per the same note. The letter agreement is filed as Exhibit 10.1.

(7) Alphabet 10-Q, Note 3, gross notional amounts of outstanding derivative instruments: equity derivatives $0 at December 31, 2025 and $30,000 million at March 31, 2026; the quoted description and fair-value statement follow the table.

(8) Alphabet 10-Q, MD&A contractual obligations and Note 5: the $40.0 billion structure and second-quarter funding expectation as quoted; variable interest entity future funding commitments of $1.1 billion and $40.7 billion at December 31, 2025 and March 31, 2026. One layout observation: the MD&A liquidity bullet describing the $40.0 billion commitment omits the “through 2030” milestone window that appears in Notes 3 and 5 and the contractual-obligations paragraph.

(9) REPORTED AND INFERRED, not filed: the identification of the counterparty as Anthropic. The Information reported Alphabet planned an investment of up to $40 billion; court documents reported via Data Center Dynamics place Alphabet’s existing Anthropic ownership near 14 percent; Bloomberg reported Google backstopping lease payments at five Anthropic-linked data-center sites. Alphabet’s existing stake predates the quarter and appears in its filings only within unnamed non-marketable equity securities.

(10) Alphabet 10-Q, Notes 3, 5, and 10: data-center lease backstops “accounted for as credit derivatives,” gross notional $16,940 million at December 31, 2025 and $28,436 million at March 31, 2026, fair value a $339 million liability; approximately $15.3 billion of additional credit-derivative notional entered into in April 2026; energy-infrastructure backstops under the financial-guarantees caption, “maximum potential amount of future payments under these guarantees was $9.0 billion.” The characterization contrast on the liability side is set out in “Apple just said a lot about Google” (July 8, 2026) in this series.

(11) Broadcom Inc. Form 10-Q for the fiscal quarter ended May 3, 2026, accession 0001730168-26-000054, Note 11, Subsequent Events, verbatim: “On June 8, 2026, we arranged for an investor partner to take on certain agreements to purchase AI racks based on custom AI accelerators designed by us and the related lease agreements with a customer that enable access to compute capacity. In connection with the arrangement, we entered into a backstop agreement with the investor partner for the customer’s lease obligations over 5-year terms. The backstop will increase over time as the AI racks are deployed and decrease as the customer makes payments on its lease obligations, with a maximum exposure of $29 billion. In the event of default by the customer, we have various remedies, including the assumption of the lease or effecting a sale of the AI racks, which would reduce our maximum exposure.” Neither the customer nor the investor partner is named in the note.