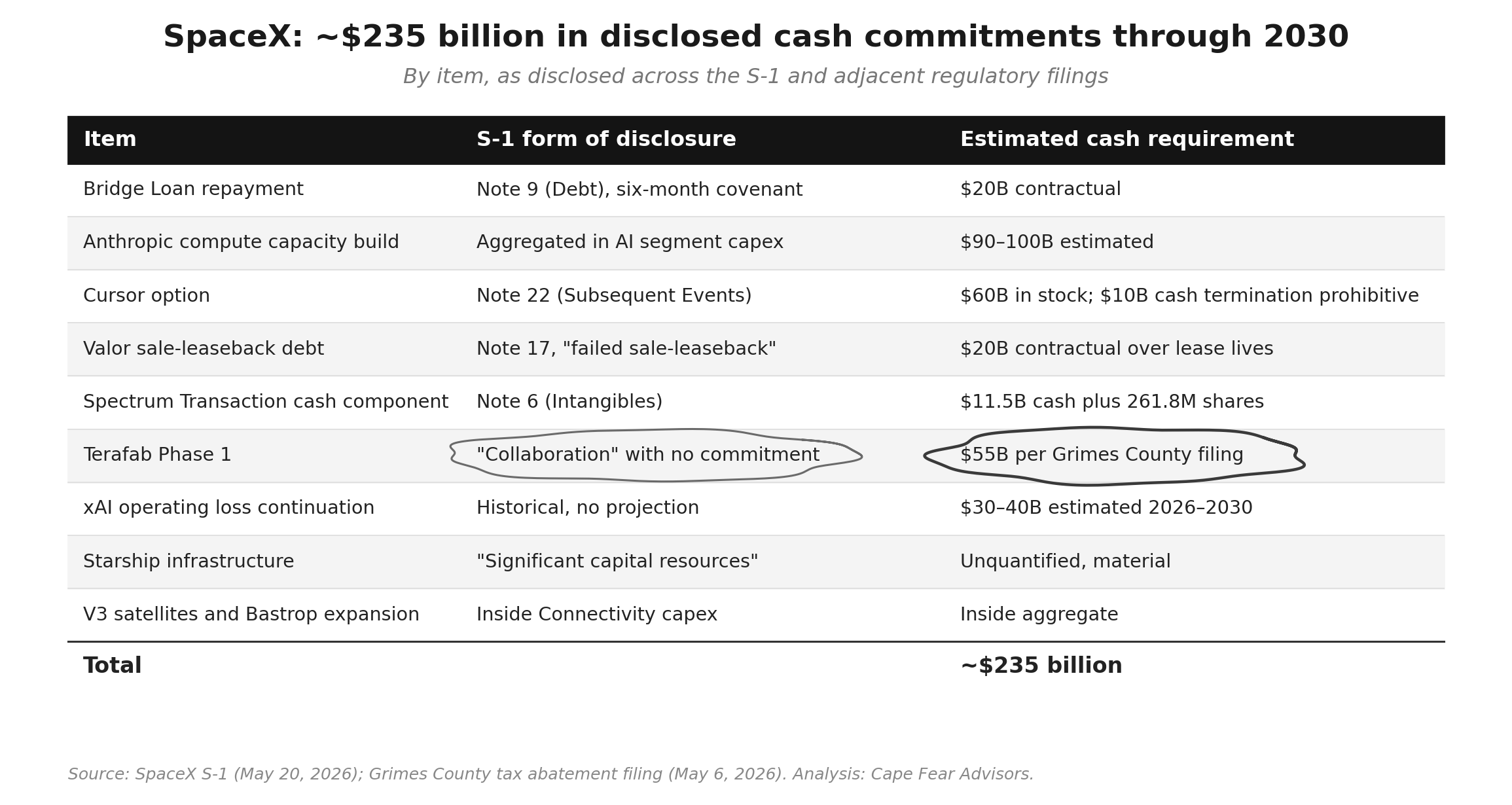

The June notes used the Grimes County filings as the load-bearing estimate of the Terafab requirement: $55 billion for the initial phases, $119 billion for the full build, inside the roughly $235 billion of disclosed commitments through 2030. That estimate stands. What is new is the paper, and the paper carries news. The executed county agreement prices the right to abandon the project at roughly $10 million today, and the price grows only as the build does. The applicant’s own sworn schedule puts $40 million of property on the ground in 2026 and the heavy years in 2028 through 2037, inside the window the rating covenants require the balance sheet to improve. Tesla, the framework counterparty, has never used the project’s name in a federal filing; the consortium as sworn to Texas consists entirely of one man’s companies; and Intel, the one source of the process and the people the fab still lacks, is left free to go by every binding document. Every published valuation carries the revenue the fab enables, and none prices the plant. Cash, per the company’s own bond-offering disclosure, stood at $100.8 billion on June 19; the $25 billion June bond and the bridge repayment bring it near $105 billion, roughly $80 billion of it deployable above the rating floor, the same size as the dated requirements before a dollar of operating burn, and every further funding door but equity reopens only by handing back something already bought. Read in one currency, the commitment sorts into four forms, announced, framework, application, executed, and only the smallest carries a signature. The record now sets the dates: a calendar of small public payments, beginning with $10 million due August 2, will price the other twenty-four twenty-fifths. The company is on the clock to turn the announcement into a commitment, and then to fund it.

Four forms of commitment, one signature

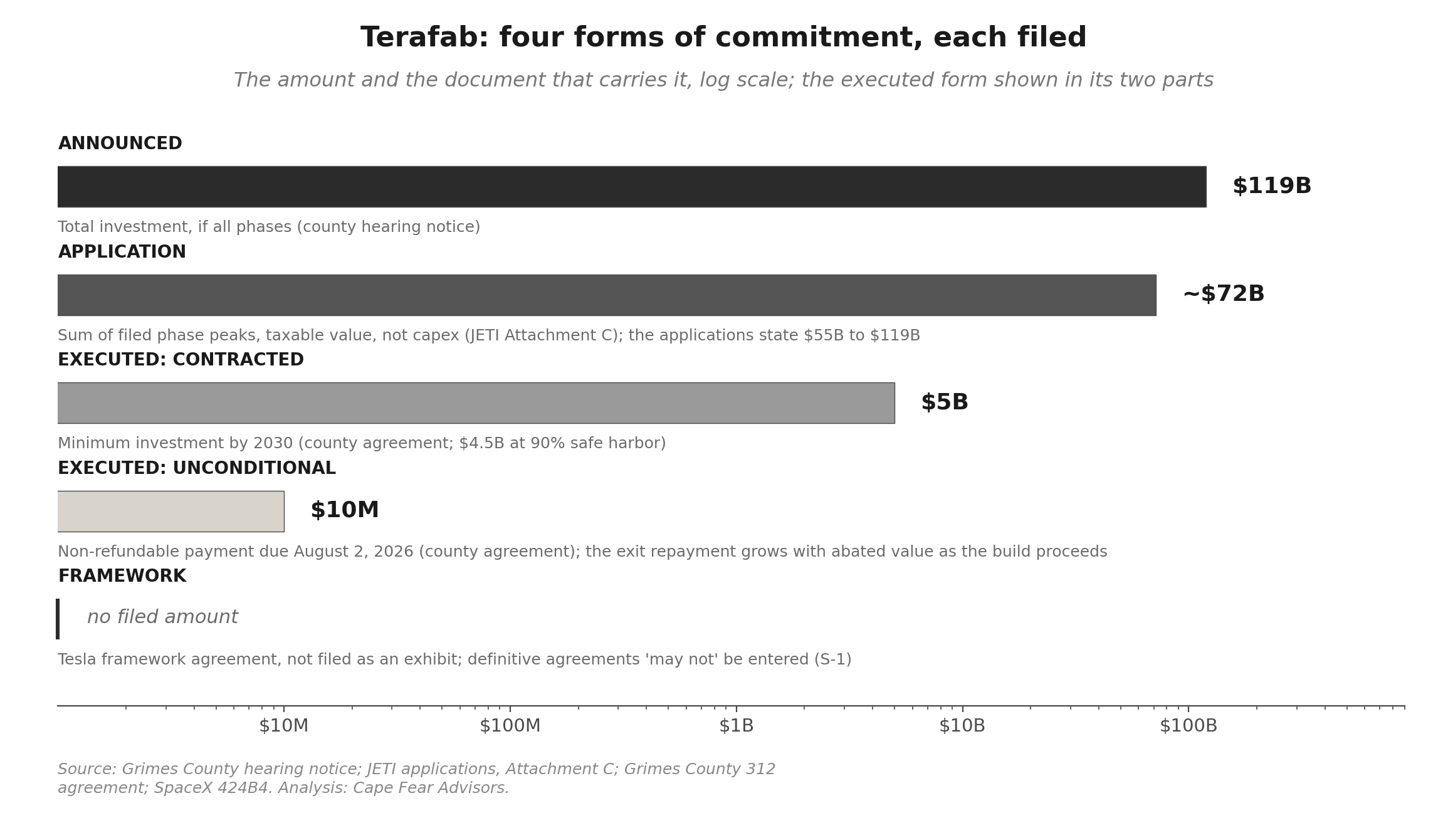

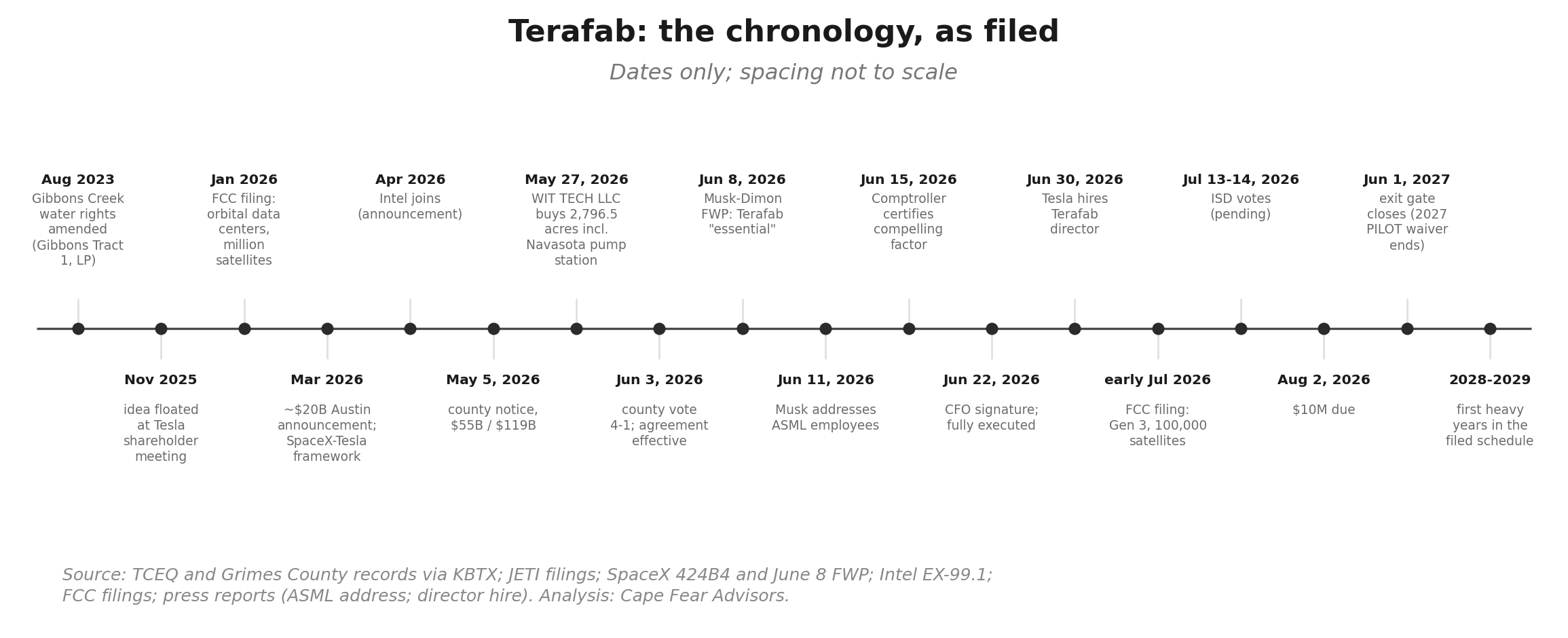

Announced: up to $119 billion. The county’s posted hearing notice carries the number in the county’s voice: $55 billion for the initial phases, $119 billion total if all phases are built. The number has a dated history. The idea surfaced at Tesla’s November 2025 shareholder meeting. The March announcement placed a roughly $20 billion fab near Austin, a vintage preserved in the record because T1 Energy, a solar company, filed a March investor deck citing “a $20 billion chip manufacturing Terafab in Austin” as a demand tailwind. April’s coverage of Intel joining carried $25 billion. The May application to Grimes County reached $55 billion initial and $119 billion total. The announced number roughly sextupled in eight weeks, each step dated in a filing or a release. (1)

Framework: a characterization, without a filed text. The S-1 describes what stands behind the announcement: a “general framework” with Tesla under which specific projects, “including any development timelines, milestones and capital expenditures,” remain “subject to separate negotiations and agreements” and “have not yet been determined.” The risk factors go further: “neither Tesla nor Intel are obligated to remain a part of the project, and we may not enter into any such definitive agreements.” The exhibit index completes the picture. The S-1’s filed material contracts run from the indemnification form through the compensation plans, the Musk restricted stock agreements, the EchoStar spectrum purchase, the bridge loan, and the xAI merger. Item 601 requires material definitive agreements as exhibits, so the framework’s absence from the list is the issuer’s own judgment on what it is: prose. (2)

Application: $55 to $119 billion, sworn by a subsidiary. The applicant in the eight state filings is TeraFab AI, LLC, Texas taxpayer 32105982659, at 1 Rocket Road, Starbase, Texas, parent company SpaceX alone. Its project description calls the work “led by a consortium of affiliated advanced technology companies, including Tesla, Inc., Space Exploration Technologies Corp. (SpaceX), and xAI Corp.” Intel, a public member of the consortium since April, is absent from that list; “affiliated” is doing precise work. The eight applications, four phases across two school districts, seek roughly $1.66 billion of school maintenance-and-operations tax benefit through 2046. Each commits to ten jobs, the statutory floor under the JETI framework, at a wage floor of $66,668: eighty jobs across all eight filings, beside the county headline of 1,800. Both are filed commitments to government bodies, weeks apart. At every layer of the record, the binding number is a small fraction of the announced one, for jobs as for money. (3)

Executed: the county agreements, and the price of leaving. The 312 tax abatement agreement and its companion 381 economic development agreement took effect June 3; SpaceX’s chief financial officer signed June 22, per the records KBTX obtained and posted. The binding terms, from the agreement text: invest at least $5 billion in facilities and equipment by the end of 2030, with a 90 percent safe harbor that makes $4.5 billion the real floor; create 1,800 full-time-equivalent jobs by the end of 2035, transfers from other Musk-company facilities expressly counting; pay the county $20 million a year in lieu of taxes for 2027 through 2036; and after 2036, under the 381, the county collects full taxes and grants back everything above $20 million a year through 2061. One payment is unconditional: $10 million, due by August 2. (4)

The exit clause, Section 10.13: SpaceX may terminate “at any time and for any reason” on 30 days’ written notice, and termination “shall not constitute a default or breach… nor shall it give rise to any claims for damages, penalties, or recapture,” except that the company repays abated taxes for up to three years, net of PILOTs paid. Early reporting rendered that as a $60 million cap, three years of the $20 million payments. The clause keys the repayment to abated taxes, a function of what sits on the tax roll. Today the roll is empty, so the exit price today is the $10 million payment, and the agreement waives the 2027 PILOT for a termination before June 1, 2027. The same clause grows with the build: three years of abated taxes on a completed campus would run to hundreds of millions. The walk-away costs least during the years the project is a story, and starts costing money on a date the agreement names.

What four public companies tell the SEC about a $119 billion project

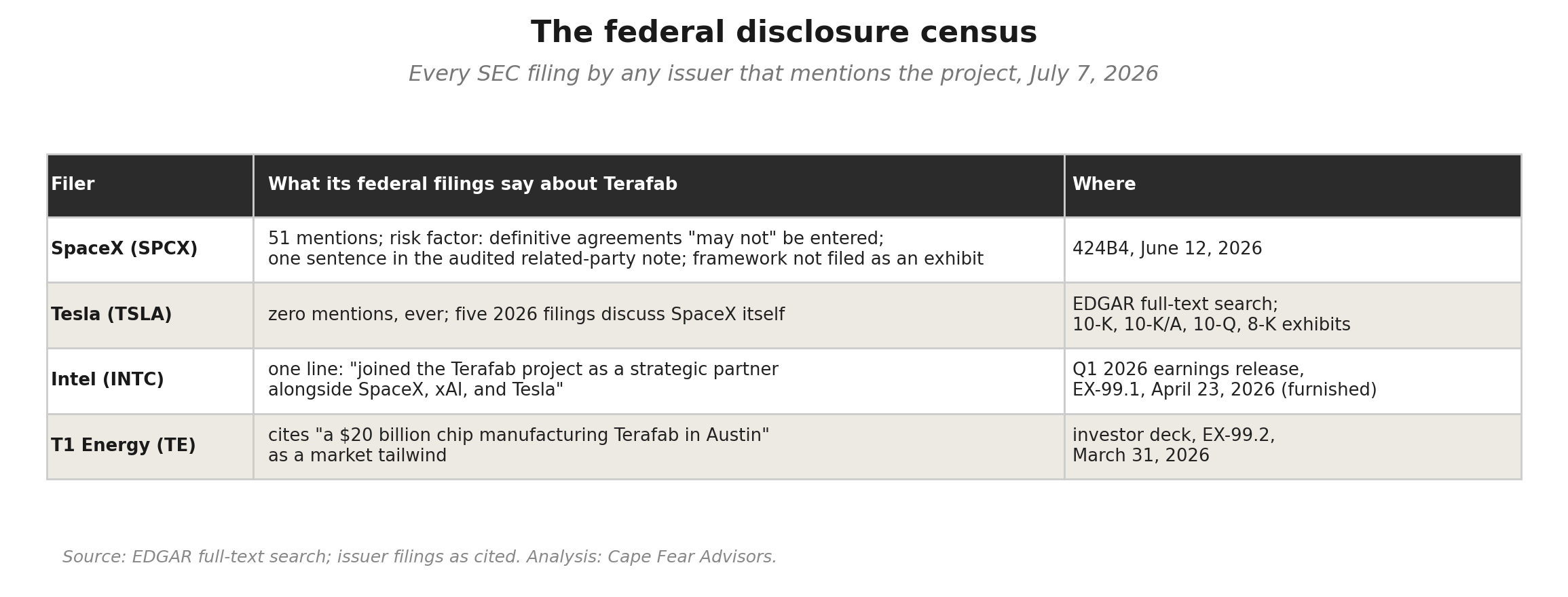

The four federal records, each in its filer’s own materiality judgment. SpaceX’s final prospectus mentions Terafab 51 times, in the narrative and the risk factors, and once in the audited financial statements, a single sentence in the related-party note recording that the company “announced a collaboration with Tesla to build a chip manufacturing facility (referred to as Terafab).” Tesla, the framework counterparty, has yet to use the word Terafab in any SEC filing: the 10-K, the 10-K/A, the first-quarter 10-Q, and two earnings exhibits, all filed since the March announcement, discuss SpaceX itself while leaving the project unnamed. Intel’s entire federal record on the project is one line in a furnished earnings release from April 23: it “joined the Terafab project as a strategic partner alongside SpaceX, xAI, and Tesla,” a membership list that matches the state application’s Musk trio with itself appended. T1 Energy carries the stale March vintage as a market tailwind. (5)

Is Intel in or out? By venue. Intel appears in the April announcement, in the technology story, the controlling shareholder saying the fab will run Intel’s 14A process, in the personnel flow, and in the county’s correspondence file. Every binding document tells the other story: the sworn consortium omits it, the audited related-party sentence names Tesla alone, the risk factor releases it from any obligation to remain, and its own filings give the project one furnished line.

The omission works backward. “Affiliated,” in a sworn application, is a word someone applied, and applying it correctly sorted the consortium: as sworn to the State of Texas, the project is led entirely by companies under one man’s control. Tesla holds the strangest seat in that sorting, the most included member in the narrative, named as family by a subsidiary in a venue where it bears nothing, and the least bound in the documents, since the county agreement’s own affiliate definition, a majority-control test, would leave it outside. On June 30 the project acquired its first named leader, Gary Jiang, a seventeen-year Intel manufacturing veteran who ran tool installation and ramp for Intel’s 18A node, hired as “Director, Terafab.” Tesla hired him. (6) The fab’s first named director draws a paycheck from the consortium member whose federal filings, through July 7, have yet to use the project’s name. Tesla reports its second quarter in late July; the silence has a test date.

The question matters because of what is missing. The record shows most of the stack assembled, and assembled inside the controller’s reach: land in the deeds, water in the rights, power in the county agreement’s own gas plants, the tax structure executed at the county and certified at the state, an entity, internal demand, and chip design teams inside the family. Three pieces remain, and each has one source. The tools: ASML alone makes the extreme-ultraviolet lithography machines a leading-edge fab requires, and the courtship is on the record, the controlling shareholder addressing ASML’s employees on Terafab within days of the Dimon conversation. (7) The process: TSMC and Samsung guard their nodes, Intel licenses, and the reported deal runs on Intel’s 14A. The operating knowledge: a licensed node is ramped by people trained on it, that experience lives on Intel’s payroll, and it has begun to move, one director so far. TSMC offers the alternative to building at all, wafers bought rather than fabs owned, and the company’s own free writing prospectus forecloses it: even the best-case assumptions of existing manufacturers fall short. So an owned Terafab requires Intel’s process and Intel’s people, whatever TSMC sells, and two of the three single sources trace to the one consortium member every binding document leaves free to go. The forward watch writes itself: a process license would be the project’s first definitive agreement anywhere, and it would reach the federal record through Intel’s filings, from the member the sworn record excludes.

The census: a project publicly sized at up to $119 billion whose total binding federal disclosure is one risk factor warning the definitive documents may never exist, one sentence in an audited footnote, one furnished bullet, and silence from the framework counterparty. The local record extends the posture: on June 25 the county asked the Texas Attorney General for permission to withhold its SpaceX, Tesla, and Intel communications from KBTX’s records requests, and confirmed along the way that the abatement rests on no independent economic or feasibility analysis. The state record has the timing model and the entity. The county record has the only signature. The federal record has the disclaimer.

The applicant’s own schedule: the spending lands in 2028 through 2037

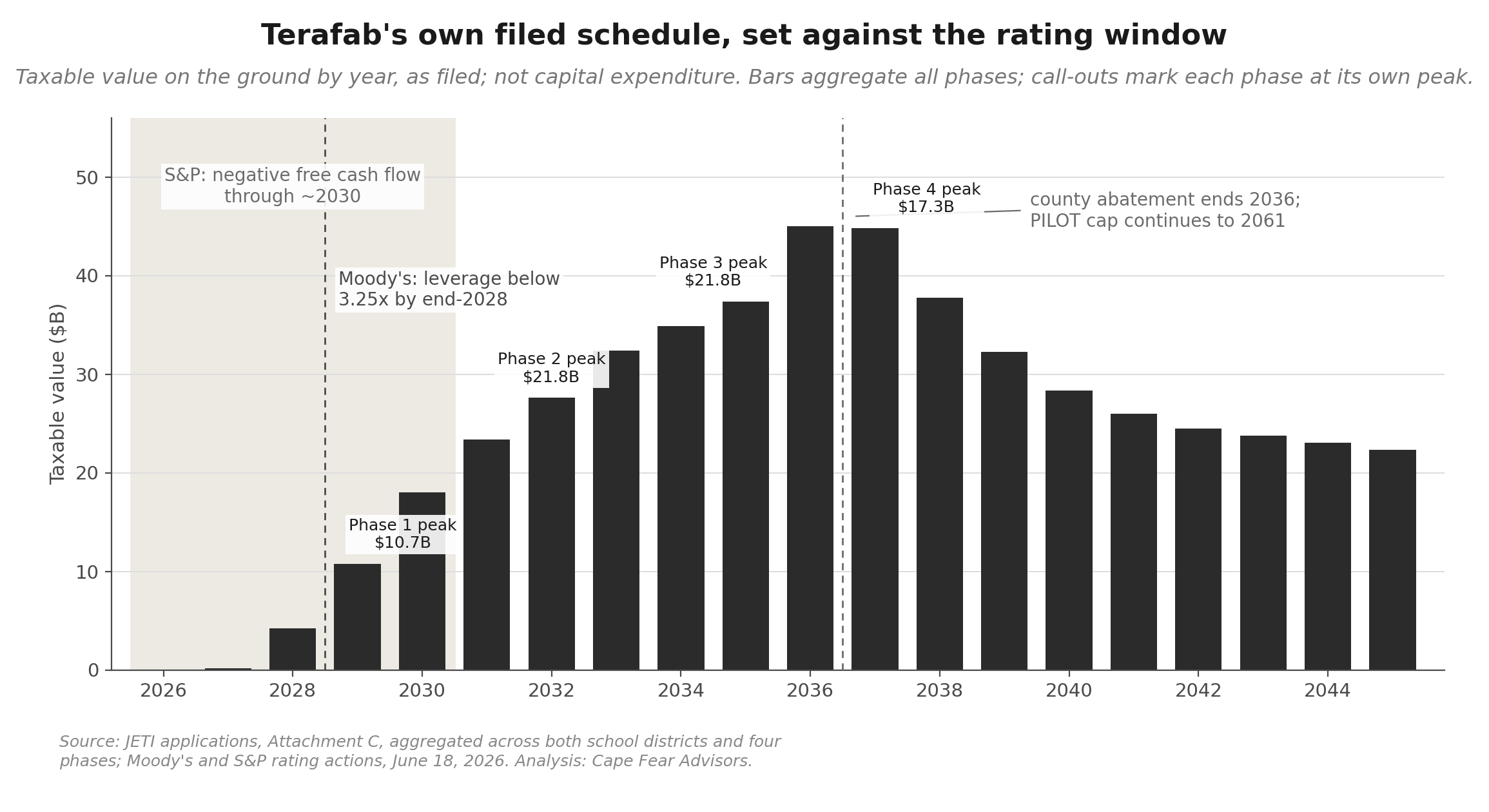

The state applications carry what the federal record lacks: a year-by-year model. Each application’s Attachment C is a 20-year schedule of the taxable value the project expects on the ground, filed with the Comptroller. These are taxable-value schedules, a proxy for deployment timing net of depreciation and assessment mechanics, and the label matters: this is the company’s own filed model of what property it expects on the ground, by year. (8)

By its own filed schedule, essentially nothing arrives in 2026: $40 million of property, then $176 million in 2027, $4.2 billion in 2028, and $10.7 billion in 2029 at Phase 1’s peak. Phase 2 peaks in 2032 at $21.8 billion, Phase 3 in 2035 at the same figure, Phase 4 in 2037 at $17.3 billion. Value on the ground crests near $45 billion in 2036 and declines as equipment depreciates, modeling to roughly $22 billion by 2045, against which the county’s take is $20 million flat.

August reads clean. The first 10-Q is due by mid-August under the 45-day rule, and the second-quarter capital expenditure line is the one number that has to satisfy two owners at once: the growth story needs it rising, the rating math needs it contained. The filed schedule settles what the line covers. Terafab contributes $40 million of 2026 property by its own model, so whatever the line prints, Colossus and the data centers are carrying it, and Terafab’s real cash calls begin in 2028.

The heavy years land inside the rating window. The agencies rated the buildout as something the company can choose to slow: S&P models negative free cash flow through roughly 2030, and Moody’s requires leverage below 3.25x by end-2028. (9) The filed schedule places Terafab’s heaviest deployment, 2028 through the early 2030s, inside that window. The company’s own state filing schedules its largest discretionary program’s peak spending into the years its rating covenants require the balance sheet to improve. Both sides are filed.

The covenant clears with room to spare. The county’s binding floor, $5 billion by 2030 with the safe harbor at $4.5 billion, sits at roughly a quarter of the $18 billion the company’s own model shows on the ground by then. Half-failure would still clear it.

One clause, two markets

The walk-away clause carries two prices at once, both on the record. The rating agencies credit SpaceX with discretionary spending it can defer, and Section 10.13 is that discretion in contract form; the clause supports the floor and the grade. The equity prices the hyperscaler story, which requires the build to be certain; the clause is the term the valuation assumes stays unexercised. Credit prices the option to stop. Equity prices the certainty of going. One document, two readings.

The models price the revenue and assume the plant

The revenue is in every model. Goldman, the lead underwriter, carries roughly $474 billion of total revenue by 2030, about $322 billion of it AI; Morgan Stanley, a co-lead, roughly $330 billion and $190 billion. The most generous credible independent, Aswath Damodaran, took the company’s story at close to full strength, doubling his AI revenue target to $160 billion by the mid-2030s and holding the probability of failure at zero, a setting his own pre-IPO practice reserved for companies that fund themselves, and reached $1.25 to $1.35 trillion, with the offer priced at 138 percent of his value. (10) The published bear, Morningstar, sits at $780 billion. Every build is a claim about AI revenue arriving on a schedule.

All of it is compute revenue. The filings route the fab’s output inward: chips “optimized for AI robots and vehicles” and chips “optimized for the space environment to be used in our orbital compute infrastructure,” inputs to the compute the AI segment sells and to products a different public company sells. What connects the fab to the revenue is the issuer’s own risk factor, one continuous passage: the company’s orbital AI ambitions “depend on our ability to access a sufficient number of AI chips, significantly more than are currently available to us”; “we expect to construct Terafab to address such supply constraints”; and should Terafab fall short, “we may not have other sources of sufficient AI chips.” Revenue, to chips, to the fab, to no alternative, in the company’s own sequence. The controlling shareholder’s filed conversation with Jamie Dimon generalizes it: the nearest American memory fab reaches volume in 2028, “even the best-case assumptions of existing manufacturers fall short of anticipated demand,” and “that’s why we need to do Terafab. It seems essential. Otherwise… there will not be enough chips.” One threshold: today’s contracted revenue rides third-party silicon; the compute SpaceX leases to Google under the June cloud agreement runs on 110,000 NVIDIA GPUs. (11) The fab becomes load-bearing at the ramp, the growth from today’s headline contracts to the models’ hundreds of billions, which requires compute at a scale the filings say only the unbuilt plant can supply. And the ramp keeps being sworn to new regulators: in January the company filed FCC plans for a million-satellite orbital data center constellation, and this week it asked the FCC to authorize 100,000 third-generation satellites as infrastructure for AI. (12) The demand side now sits in county, state, securities, and spectrum filings. The supply side remains a framework, and each new application enlarges the shortage the framework exists to cure.

Each revenue path therefore implies a capacity date, and the sworn schedule answers it. Revenue collected in 2030 requires compute in service around 2029 and chips before that; at the end of 2029 the filed schedule has one phase standing, $10.7 billion of property, with the volume phases arriving 2032 through 2037. The bull case needs the fab’s output roughly three years ahead of the applicant’s own schedule. The generous independent’s mid-2030s vintage fits the calendar, and the money sits outside his model by design: he reinvests about $133 billion across ten years, roughly $13 billion a year, funding the revenue he forecasts rather than the buildout the company announced, while the county filing prices this one project at $55 to $119 billion and the company’s actual capital spending ran $10.1 billion in the first quarter.

Damodaran’s spreadsheet carries four revenue lines, launch, Starlink, AI, and an expansion bucket he describes as “expansion options embedded in each business,” with Terafab appearing nowhere in the spreadsheet or the post. Assign the fab to that bucket as generously as possible and the assumptions require it to be the most capital-efficient fab ever operated, by a factor of about five. The bucket builds $100 billion of 2036 revenue with roughly $20 billion of capital and implies an after-tax return on incremental capital near 120 percent. TSMC, the most efficient fab operator in history, at the peak of its strongest cycle, turns roughly a dollar of invested capital into a dollar of annual revenue, spent 33 percent of its 2025 revenue on capital to hold that position, and prints returns in the high forties at the cycle top and the twenties through it. (13) The bucket’s modeled margin sits below TSMC’s actual one; the entire excess is the capital assumption. The bank models stay private, their reported summaries carry compute revenue and, in Goldman’s case, name “future equity raises” without quantifying them. The cash for the plant enters the record as an assumption in the one public model, a phrase in the lead underwriter’s, and silence in the rest. No published build prices the plant its own revenue requires. And the exclusions are sound practice, which is the point: an unsigned project is not a valuation input. The $119 billion lives in one place only, the price.

The cash: $80 billion deployable, against a dated $80 billion

Cash is the reconciling variable, because the equity rests on the revenue while the debt restrictions cap the spend: Moody’s leverage test at end-2028, S&P’s tolerance conditioned on continued raising, Fitch’s expectation that the company defers discretionary capital if access tightens. Debt at fab scale would spend the grade the company bought in June.

Capital coming in has not been the constraint. In its first three weeks public the company raised $86 billion of equity, sold $25 billion of bonds on $89 billion of orders, and agreed to buy Cursor for $60 billion in stock: capital in three currencies, roughly $171 billion of it. The June 22 bond disclosure put cash at $100.8 billion as of June 19; the bond settled June 26 and the bridge was repaid from it, leaving roughly $105 billion. The $25 billion minimum-cash commitment, the price of the rating, holds the floor, and roughly $80 billion sits above it. Against it, the dated requirements: the fab’s initial phases, the county’s own $55 billion definition, spent by roughly 2029 if the 2030 revenue is to exist; AI-segment capital spending already running $7.7 billion a quarter; the Spectrum close taking $11.5 billion of cash in November 2027; Valor leases near $3.4 billion a year; a free-cash-flow run rate near negative $36 billion a year. (14) Any conservative assembly of the project pieces alone puts at least $80 billion out the door before the revenue’s date. The deployable pool and the dated project requirement are the same size, before a quarter of operating burn touches either.

The other sources stay open, and each carries a price the company has already been paid once. The debt door has opened once already: the June bond, rated into the grade, retired the bridge and added about $5 billion of new cash; debt at fab scale beyond it spends the grade, with Fitch’s rating conditioned on deferring discretionary capital and the covenant counting cash against the leverage test. The $25 billion floor is spendable by un-committing it, and the agencies credited the commitment. The customers could prepay or commit, by reopening contracts whose value to the story is that they read as firm at the headline; the two anchors pay monthly, in arrears, on 90-day terms, and financed none of the construction. The partners could fund, by signing the definitive agreement that starts the disclosure machinery at both companies; the framework leaves capital expenditures “not yet been determined” precisely as long as it stays a framework. The county and state incentives run the other way in the near term, $10 million out on August 2. Every door reopens by handing back what it already bought: the grade, the floor, the headline, the silence. Equity is the door that costs only new money, and the S-1 reserved it in a single sentence: “We may issue a significant amount of equity in connection with future transactions.” The sentence sits inside the acquisitions risk factor, the paragraph that names xAI, the spectrum, Terafab, and Cursor, so the disclosed funding plan is equity-for-transactions, and Cursor proved the mechanism six days after listing: $60 billion, in stock. It comes in two shapes, a secondary offering or a stock-funded acquisition, and an acquisition could close the missing pieces and the cash gap in a single document. Either shape spends the same currency, which requires the price, which requires the announced number alive, which the calendar tests. Its filed complication comes with it: new shares would price from a level the most generous independent marks 28 percent lower, into the same window the lockup releases insider supply.

Also in the record: water and power

The campus supplies its own inputs, and the record shows who owns them. The power, from the county agreement’s own text: the project is “expected to include semiconductor manufacturing facilities; natural gas fired power plants, and artificial intelligence facilities to be used in conjunction with the manufacturing process,” powered on site and off the grid. The power buildout is inside the same capital requirement as the fab.

The water has a filed magnitude and an open owner. TCEQ records show water-rights certificates tied to Gibbons Creek Reservoir were amended in August 2023, nearly three years before the project was named, authorizing permanent consumption up to 3.2 billion gallons a year, several times what a large semiconductor plant draws, in keeping with a campus that is a fab, an AI facility, and its own power plants. On May 27, one week before the county vote, WIT TECH LLC, a Wyoming entity, bought six parcels totaling 2,796.5 acres, including the Navasota River pump station and the one-acre parcel that is the river itself, with reporting placing contracts for more than 6,000 acres behind them. (15) The entity’s paper trail points two directions: its Wyoming filings carry the signature of Jared Birchall, who manages the Musk family office, and its deed records carry James Burnham, xAI’s general counsel, and xAI has been inside SpaceX since February. The public record leaves the water’s balance-sheet home open: the controller’s private holding, or already the public company’s. The county agreement draws the facility’s water from Gibbons Creek Reservoir and names no owner of the intake. A future disclosure settles it either way: a related-party note if the water is private, a subsidiary schedule if it is home. KBTX traced the parcels and the entity, part of a records effort running past twenty public-information requests; these documents are public because of that work.

The application’s compelling-factor section argues the limitation is decisive because otherwise “competing jurisdictions (e.g., Arizona) would present a more favorable after-tax return.” The consortium’s public plan contemplates an Arizona fab beside Intel’s campus regardless, and the Comptroller certified the factor on June 15.

The clock: the dates that test the project, and the financing behind it

If the company steps back from Terafab, when must it say so? The disclosure rules attach to decisions and to filed agreements, and the record holds neither. The framework was never filed; the county agreement, though signed, sits outside the S-1’s exhibit list, so by the issuer’s own materiality judgment even a termination notice arguably travels without a report. The risk factors, written before the offering, already cover the exit: the project “may not be successful,” the definitive agreements “may not” be entered. The structure that never required a commitment never requires an un-commitment. A decision would surface in a later report, if a decision is ever made; drift is quieter than that.

What replaces disclosure is a calendar of small public payments and other companies’ reporting dates, each a revealed preference. July 13 and 14, approximately: the school boards vote, the Governor’s approval still pending, and since property placed in service before the agreements execute loses eligibility, a serious builder signs quickly. Mid-to-late July: the counterparties report before the company does. ASML discloses bookings, and extreme-ultraviolet tools are ordered years ahead of wafers, so a schedule that finishes construction in 2028 has to leave orders in that backlog within quarters; TSMC takes questions days later; Intel, which put the project in its first-quarter release, chooses among updating the line, repeating it, and dropping it, all three legible; Tesla’s silence gets its test. August 2: the $10 million pays, maintaining a $119 billion story at a dollar per twelve thousand, or a Material Obligation defaults in a public record. Mid-August: the first 10-Q, with the fab absent from the capex line by its own model, so the line reads on Colossus alone; the lockup’s first trigger runs two trading days behind the release. Year-end: the sworn applications put construction commencement in 2026, and the Comptroller’s letters rescind if the information changes. February 1, 2027: half the 2027 PILOT, $10 million. May 1, 2027: the first annual compliance certificate to the county. June 1, 2027: the exit gate closes; the agreement waives the 2027 PILOT for terminations before this date, so every later day is the first that leaving costs real money. June 15, 2027: the state recommendations lapse if the school agreements sit unexecuted.

Across the same months run the other two clocks. The lockup releases begin at the earnings trigger and run through 180 days in December and 366 days next June. The equity raise, the cheapest door the record leaves, has to come before the spending it funds, and the bull case needs the spending by 2028; the raise window is this window. Three calendars, one year: the announced number has to stay alive to price the raise, the county’s payment dates test whether it is, and the insiders’ first sales run alongside both. The market’s visibility into a $119 billion project runs through whether a $10 million check clears in Anderson, Texas.

Later still: the definitive consortium agreements, if they are ever signed, and the related-party notes of future filings, where the water, the subsidiary, and the allocation among four balance sheets each acquire a document. Until then the $119 billion is a number with one signature under one twenty-fifth of it.

Whence the cash. Still open, now dated. And, in whose name.

Notes

(1) Grimes County public hearing notice, county-posted: “Estimated capital investment for the initial phases is $55 billion, with an estimated total capital investment (if additional phases are constructed) of $119 billion.” The March vintage: T1 Energy investor presentation, EX-99.2, March 31, 2026 (“a $20 billion chip manufacturing Terafab in Austin”). The April vintage, $25 billion, per contemporaneous coverage of Intel’s joining.

(2) SpaceX Form 424B4, June 12, 2026: the framework language and the risk factor quoted appear in the business section and risk factors. The exhibit index to the S-1 lists the material contracts named; the Tesla framework agreement is not among them. Item 601 of Regulation S-K governs required exhibits.

(3) JETI applications J0035 through J0038 (Anderson-Shiro CISD) and J0039 through J0042 (Iola ISD), TeraFab AI, LLC, applicant, with Texas Comptroller recommendation letters signed June 15, 2026. Applicant identity, parent, jobs commitments, and wage floors per the applications; the $1.66 billion is the sum of the eight “estimated M&O gross tax benefit” figures in the Comptroller’s Attachment A summaries. Each recommendation is rescinded if the application is modified or the information presented changes, and lapses unless the school agreements are executed within one year.

(4) Grimes County 312 Tax Abatement Agreement and Section 381.004 Economic Development Program and Agreement, each effective June 3, 2026, as released by the county and posted by KBTX; the June 22 signature of SpaceX’s chief financial officer per KBTX’s report of the fully executed version. Terms cited: Sections 3.4 and 3.6 (payments), 4.1 through 4.3 (investment, jobs, safe harbor), 10.13 (termination), and the 381’s Section 3(a) (grants of taxes above $20 million, 2037 through 2061).

(5) EDGAR full-text search, July 7, 2026, all issuers, “Terafab.” SpaceX: Form 424B4. Tesla: 10-K, 10-K/A, first-quarter 10-Q, and two 8-K exhibits filed since March 2026, each discussing SpaceX without naming the project. Intel: Q1 2026 earnings release, Exhibit 99.1, furnished April 23, 2026. The county’s Attorney General request and the absence of an independent feasibility analysis per KBTX, July 2, 2026.

(6) The director hire: Electrek and Tom’s Hardware, June 30, 2026, from the executive’s own announcement of the role.

(7) The ASML address: Bloomberg, June 6, 2026, and CNBC, June 11, 2026. The 14A process: the controlling shareholder’s public statements and contemporaneous reporting.

(8) Attachment C of each JETI application, aggregated across both school districts and all four phases. The schedules state taxable value by year; they are a timing proxy, net of depreciation and assessment mechanics, and are not capital expenditure. Iola Phase 2 figures mirror the Phase 3 schedule shifted by three years, consistent with the OCR of the filed tables.

(9) Moody’s, Fitch, and S&P rating actions, June 18, 2026, as described in the June 19 note in this series.

(10) Aswath Damodaran, post-prospectus SpaceX valuation, June 2026, posted with the full spreadsheet. The failure-probability comparison draws on his prior pre-IPO valuations (Uber, Lyft, WeWork, Airbnb, Zomato, at 5 to 20 percent) and his Tesla series, where zero arrived only with self-funding; the June 7 note in this series sets out the record.

(11) SpaceX free writing prospectus, June 5, 2026: the Google Cloud Service Agreement, approximately 110,000 NVIDIA GPUs, $920 million per month from October 2026, terminable by either party on 90 days’ notice after December 31, 2026. Terms read against the headline in the June 6 note in this series.

(12) FCC filings: the orbital data center constellation application, January 2026, accepted for filing by the Space Bureau in February; the third-generation constellation application, approximately 100,000 satellites, submitted the week of July 6, 2026, per the filing and contemporaneous coverage.

(13) TSMC 2025 results ($122.9 billion revenue; $40.9 billion capital expenditure) and 2026 capital guidance ($56 billion), company reports and press coverage; returns as computed by standard screens, cycle-peak versus through-cycle.

(14) Cash and capital, as filed: the Form 8-K launching the notes offering, June 22, 2026, disclosed approximately $100.8 billion of cash and cash equivalents as of June 19, 2026; the pricing 8-K of June 23 set the five tranches ($7.0 billion at 5.350% due 2031, $6.0 billion at 5.650% due 2033, $6.0 billion at 5.875% due 2036, $2.5 billion at 6.600% due 2046, $3.5 billion at 6.650% due 2056); the offering settled June 26, with proceeds repaying the bridge loan in full, paying fees, and the remainder to “general corporate purposes.” The Cursor consideration is stock (Form 8-K, June 16), capital in without cash. Requirement components as filed: first-quarter 2026 consolidated capital expenditure of $10.1 billion, $7.7 billion of it in the AI segment (424B4); the EchoStar spectrum cash component, $11.5 billion (Note 6); the Valor lease obligations (Note 17); 2025 free cash flow of negative $13.9 billion and the first-quarter run rate, per the cash-flow statements. The arithmetic follows the June 5 and June 19 notes in this series.

(15) TCEQ water-rights certificates and amendments, and Grimes County deed records, via KBTX’s reporting, with additional deed detail (the xAI general counsel’s appearance in the records; contracts for more than 6,000 acres) via national pickup of the same records.

Part of a continuing read of the SpaceX offering documents, taken one at a time and in a single currency. Clause citations are pinned to the agreement texts; figures are verified against the primary filings. Analysis: Cape Fear Advisors.

Greg Collins serves as CEO of C3 Metrics, a marketing measurement and analytics firm, and maintains an advisory practice at Cape Fear Advisors focused on structural analysis and strategy.

The author holds no direct position in any security discussed. Whatever indirect exposure comes through index and managed funds is neither known to him nor, he suspects, escapable.

This article is also available on Substack.

Start a Conversation →